Today, the Bureau of Labor Statistics reported that the United States Of America created 431,000 jobs in March. We also had 95,000 positive revisions, and although this was a slight miss of estimates, it continues the solid trend of good job reports in 2022. On another note, I raised my third recession red flag, since the inverted yield curve happened this week. I’ll talk about jobs first and then get to the recession red flag model as three of the six flags are up now.

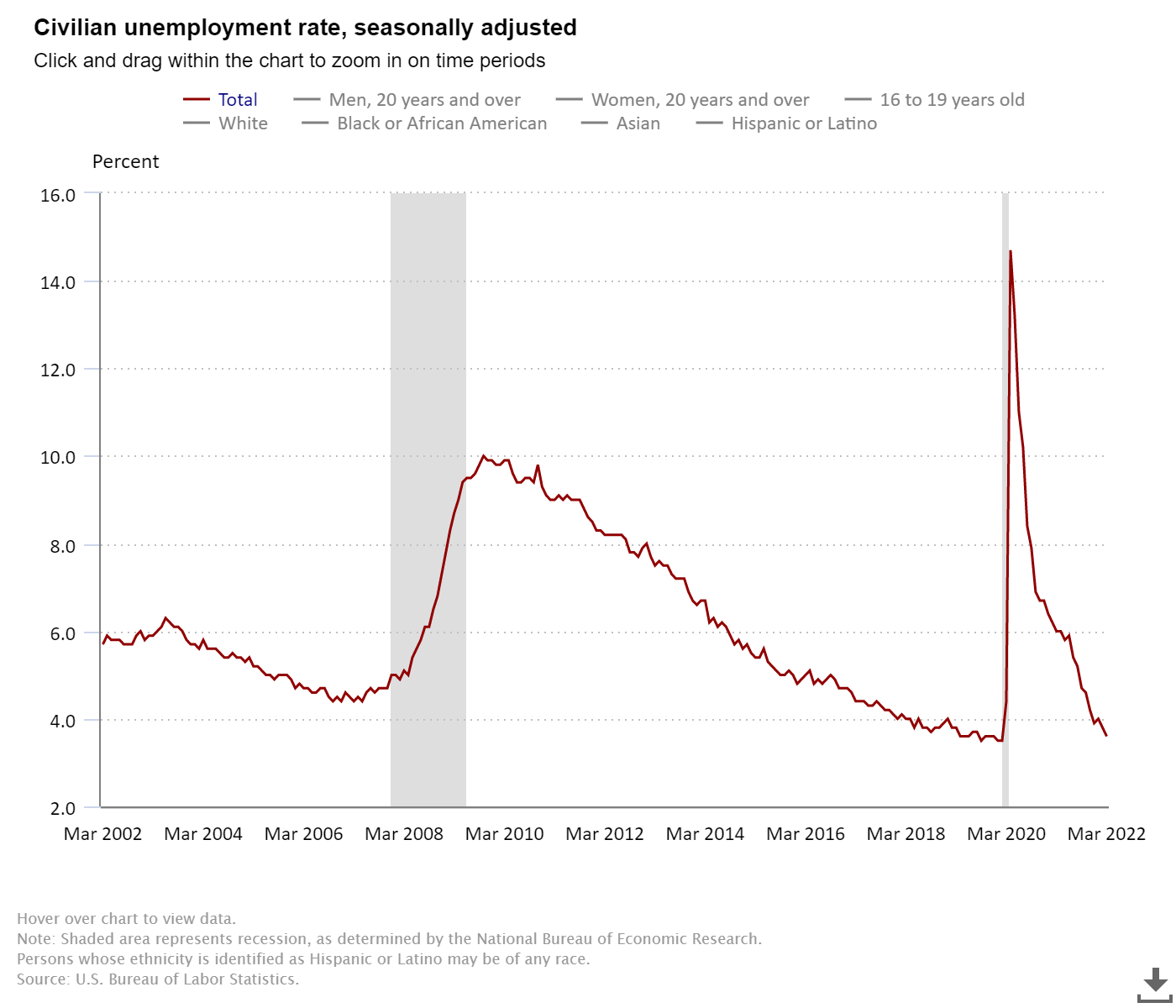

The U.S unemployment rate stands at 3.6%, and we are getting closer and closer to my September 2022 forecast of getting all the jobs back that we lost due to COVID-19. If you break it down to women over 20, the unemployment rate is 3.3%. For men over the age of 20, it’s down to 3.4%. As you can see below from the unemployment rate chart, the job recovery was much faster than after the great recession of 2008.

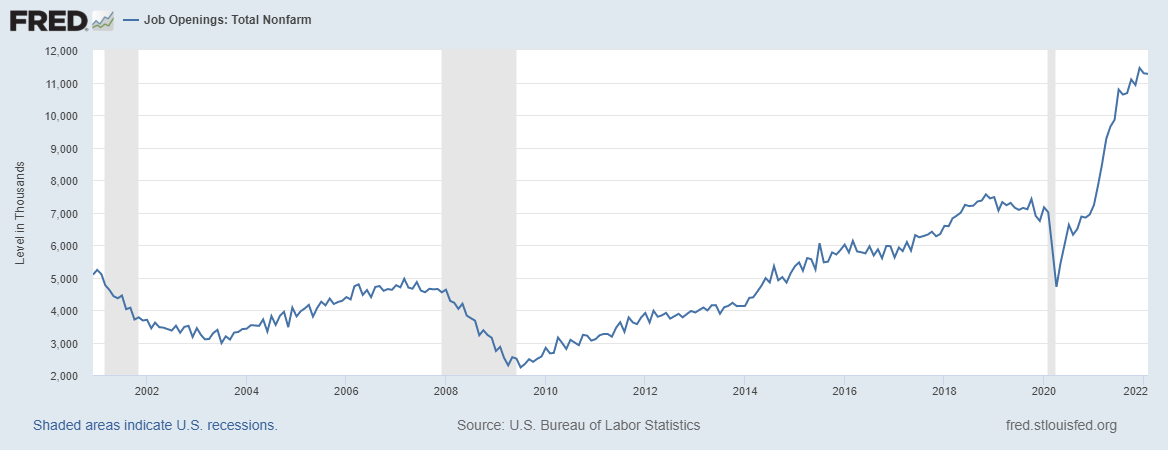

Early in this historical economic recovery, which started on April 7, 2020, one of my big themes was that job openings would get over 10 million.I sent out many tweets saying #JOLTS 10,000,000, and even when we had some big job misses in 2021, I didn’t change my tune. “Job openings should get to 10,000,000 in this expansion. Don’t forget the Boomers are aging out of the labor force, they need to be replaced.”

The internal jobs data always pointed to a strong recovery, and job openings have been trending higher since 2008. The years 2020-2024 were going to be different not only for the housing market but also for the labor market. The recent job openings data is over 11 million with an unemployment rate of 3.6%! Just whistle, folks — that is a hot labor market.

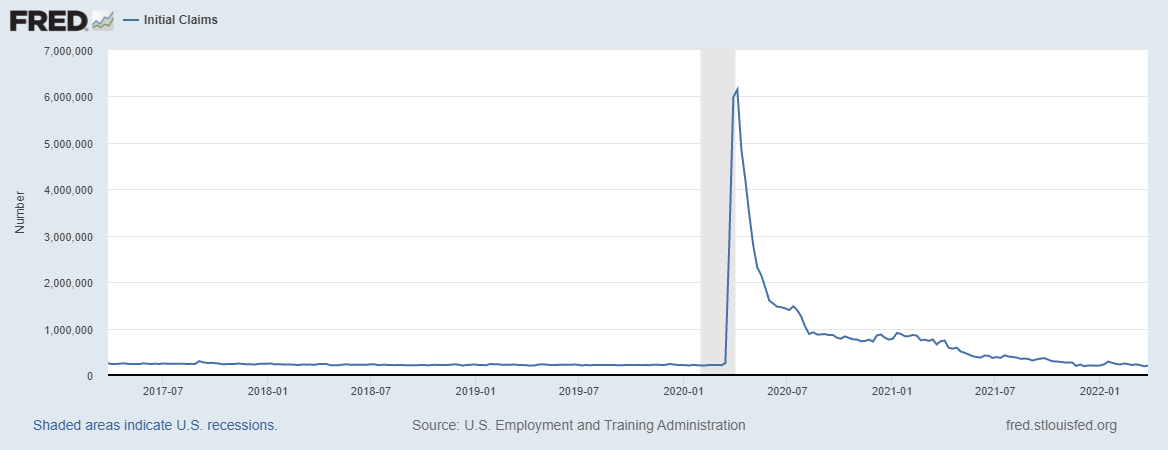

Jobless claims data looks solid as companies are fighting to get the labor they need. They also have to make sure they retain their labor as well.

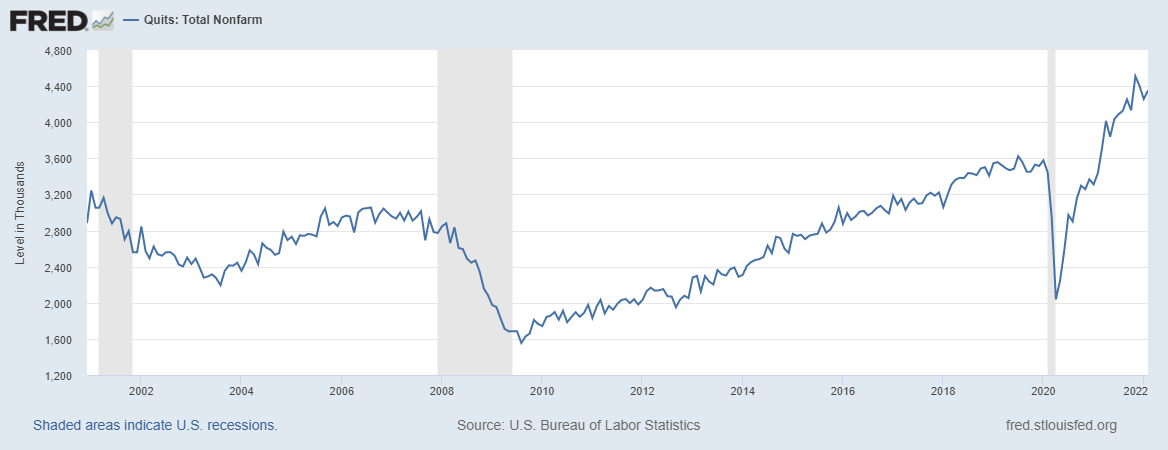

People are quitting for better pay. A tighter labor market is a good thing, not bad. The premise that robots and immigrants would take all the employment has been destroyed. Many small business owners were lied to believe this by politicians from both parties, and they’re having trouble finding labor and keeping them.

One positive that the U.S. has that other countries don’t: we have a massive young workforce. The millennials and Gen Z are enormous, and I talk about these wonderful people as replacement workers and consumers.

Other countries worldwide aren’t as fortunate as we are, so count your blessing; you live in the United States Of America. Imagine if we didn’t have a massive young workforce, our economic growth would be much slower.

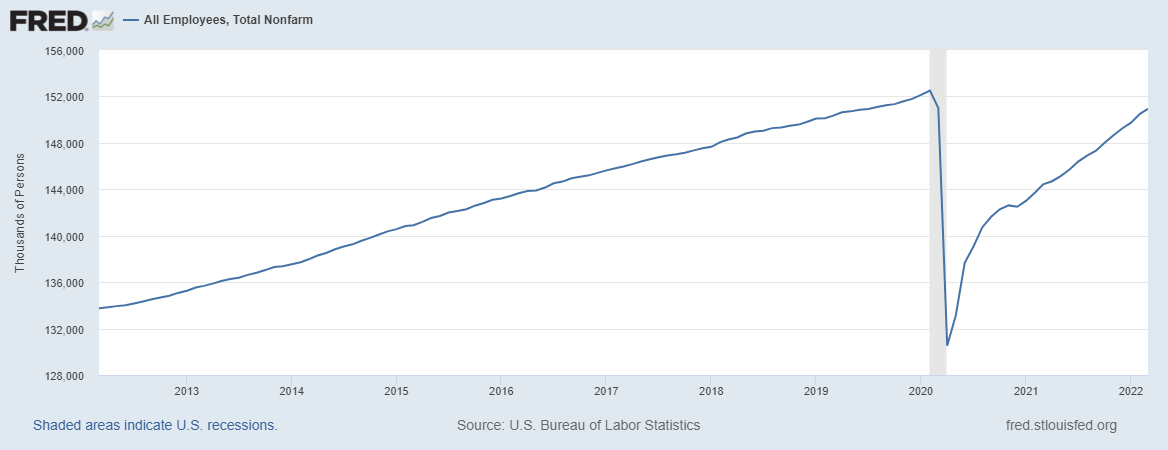

After I retired the America is Back recovery model on Dec. 9, 2020 one thing that I knew would take just a bit longer than other economic data lines to recover was the job gains. As you can imagine, a Global pandemic can impact a few economic sectors more than others.

Also, the demographic turnover in labor is much different now. However, even with that said, the civilian labor force is large enough to get all the jobs back. I just believed it would take until September of 2022 to happen, with some chance of it happening sooner. Of course, Delta and Omicron weren’t part of that equation. but nonetheless, I never changed that date.

—Feb 2020: 152,553,000 jobs

—Today: 150,925,000 jobs

That leaves us with 1.628 million jobs left to make up for six months, which means we need to average adding 271,333 jobs per month. The unemployment rate currently stands at 3.6%.

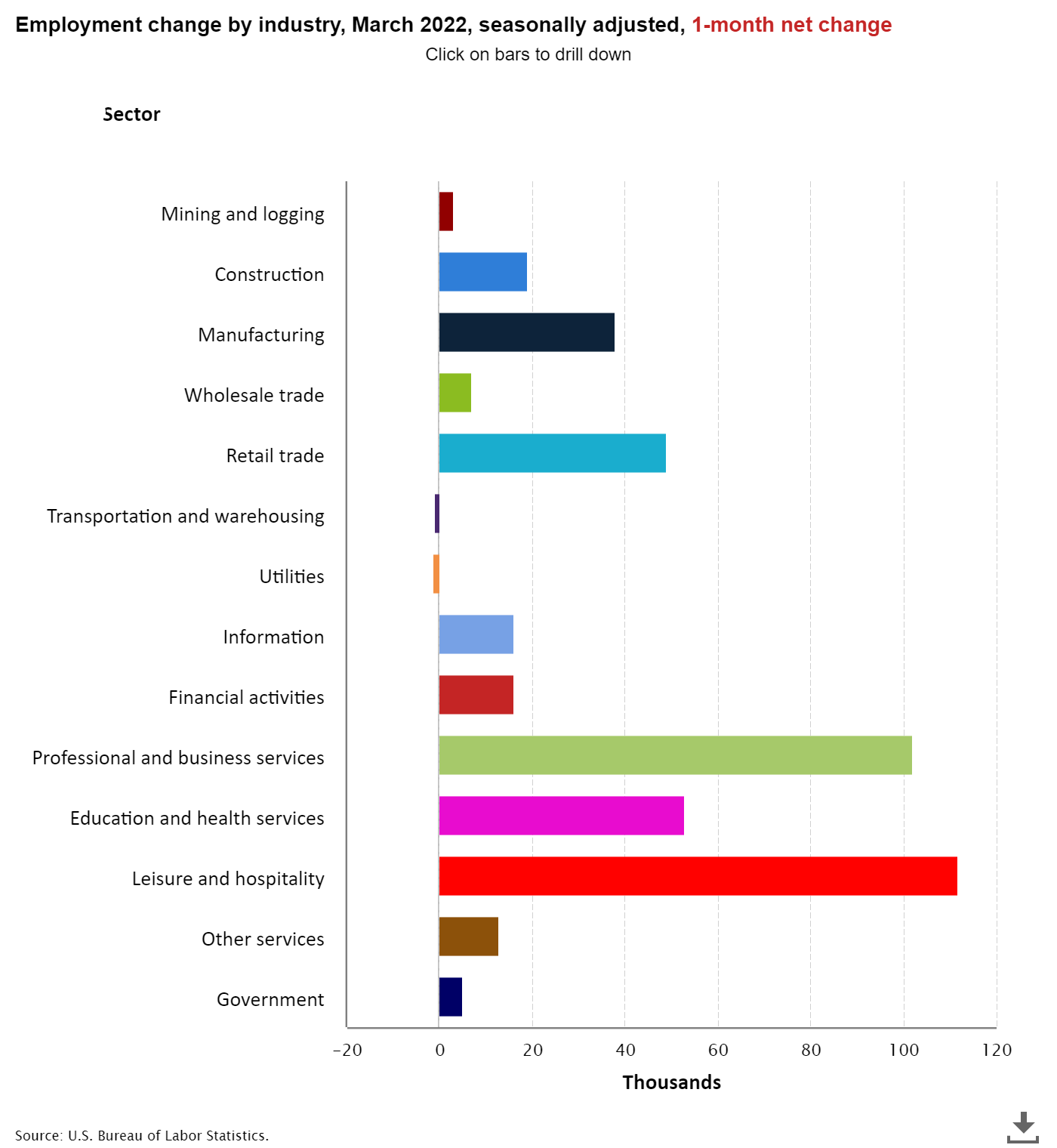

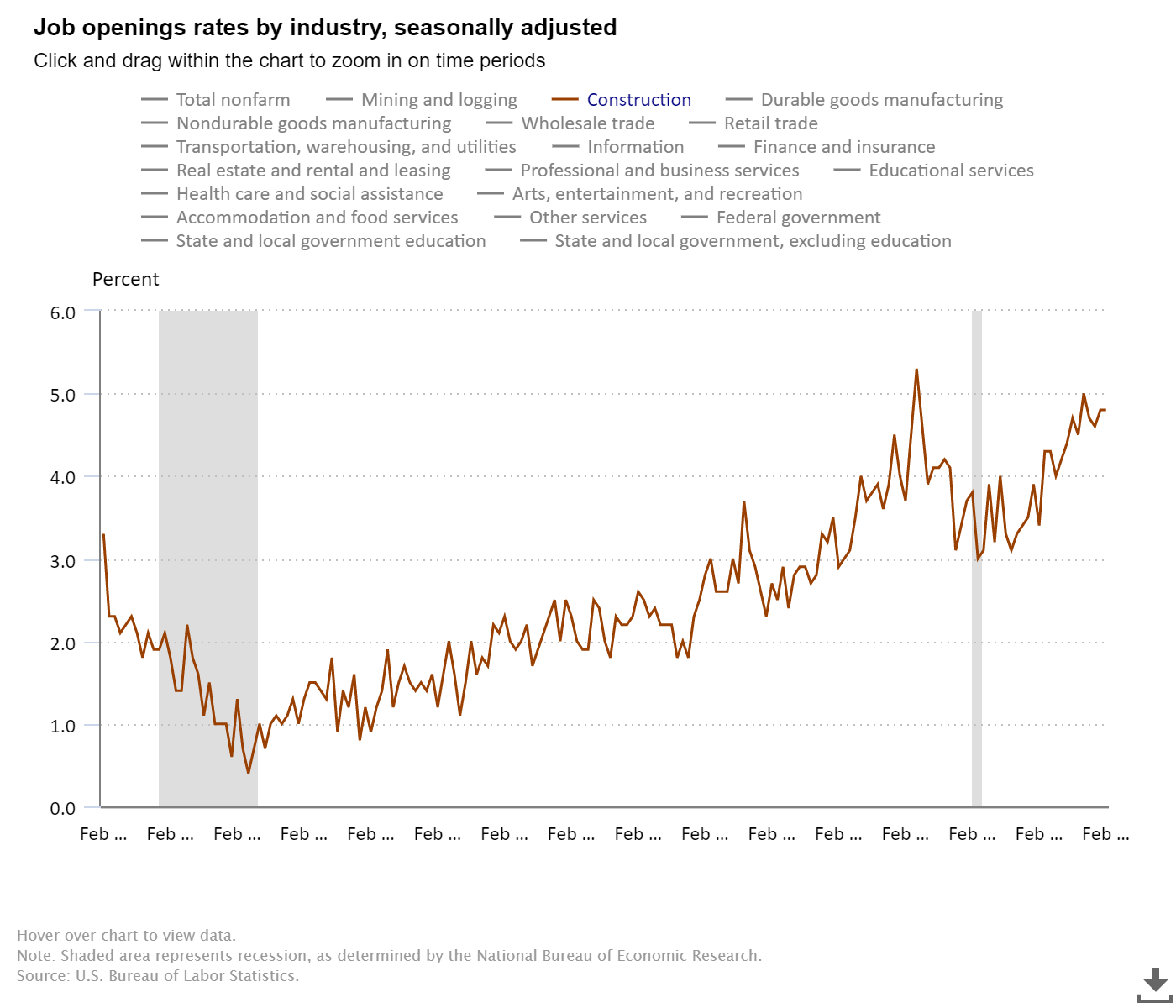

Look at the jobs data and which sector added jobs in March: Construction jobs came in positively, which we need in this country.

Job openings for construction workers are still historically high today, as the need for labor in America is high.

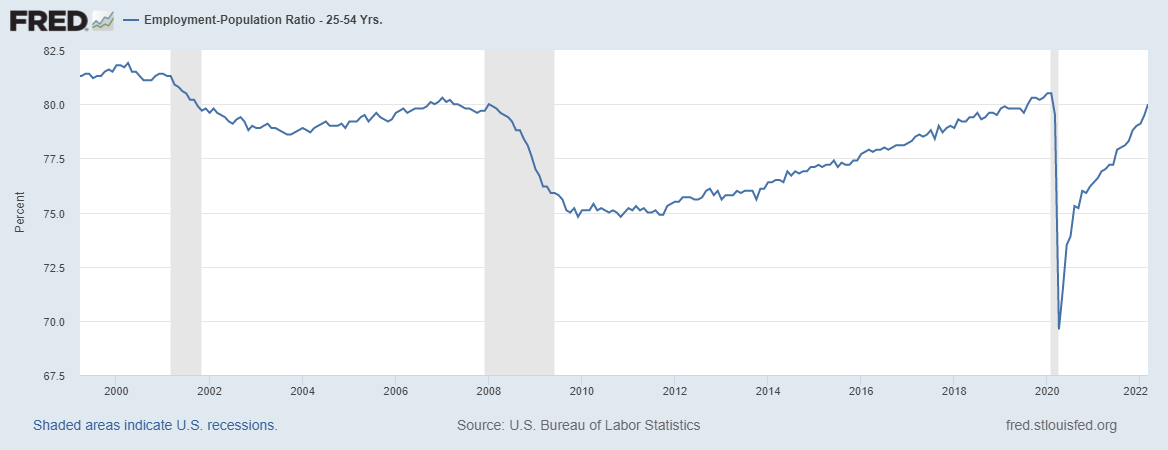

Looking at jobs data is always about prime-age employment data for ages 25-54. The employment-to-population percentage for the prime-age labor force is 0.5% away from being back to February 2020 levels. The jobs recovery in this new expansion has been much better than we saw during the recovery phase after the great financial crisis.

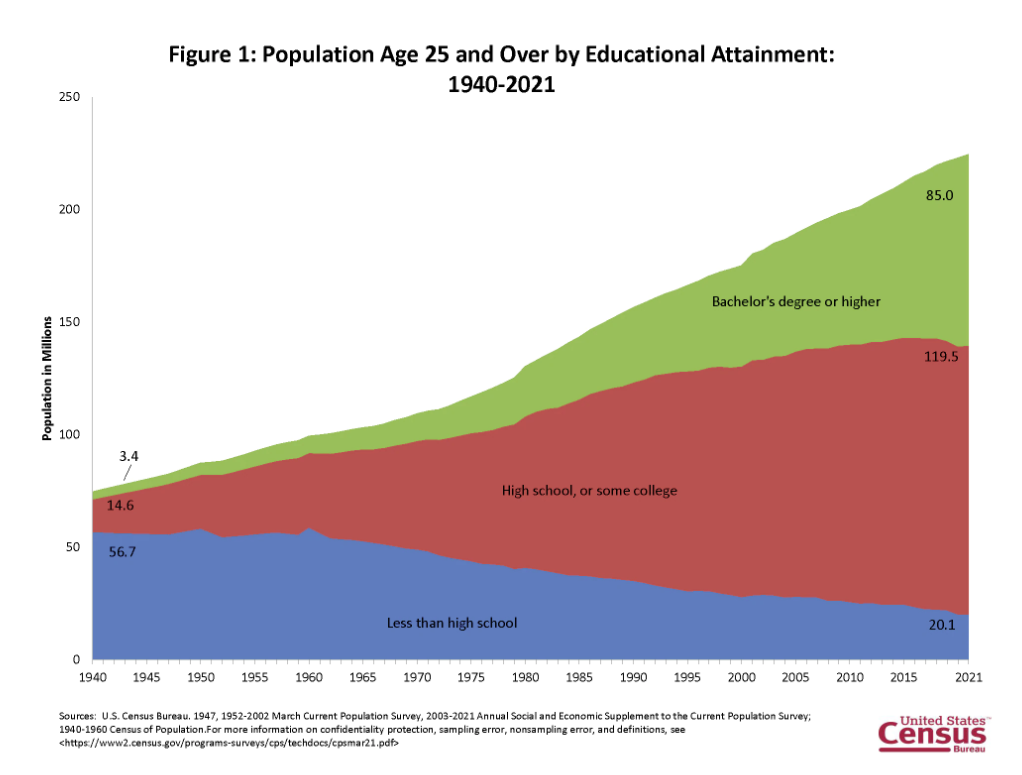

Education and employment

Most Americans have always been working, even if they’re not college-educated. The labor force with the least educational attainment tends to have a higher unemployment rate. I started the hashtag A Tighter Labor Market Is A Good Thing to remind everyone that the economy runs hot when we have a tighter labor market. We want to see the kind of unemployment rates that college-educated people have spread to everyone because we have tons of jobs that don’t need a college education.

Here is a breakdown of the unemployment rate and educational attainment for those 25 years and older:

—Less than a high school diploma: 5.2%.

—High school graduate and no college: 4.0%

—Some college or associate degree: 3.0%

—Bachelor’s degree and higher: 2.0%

As we can see, the labor market is solid and has some legs.

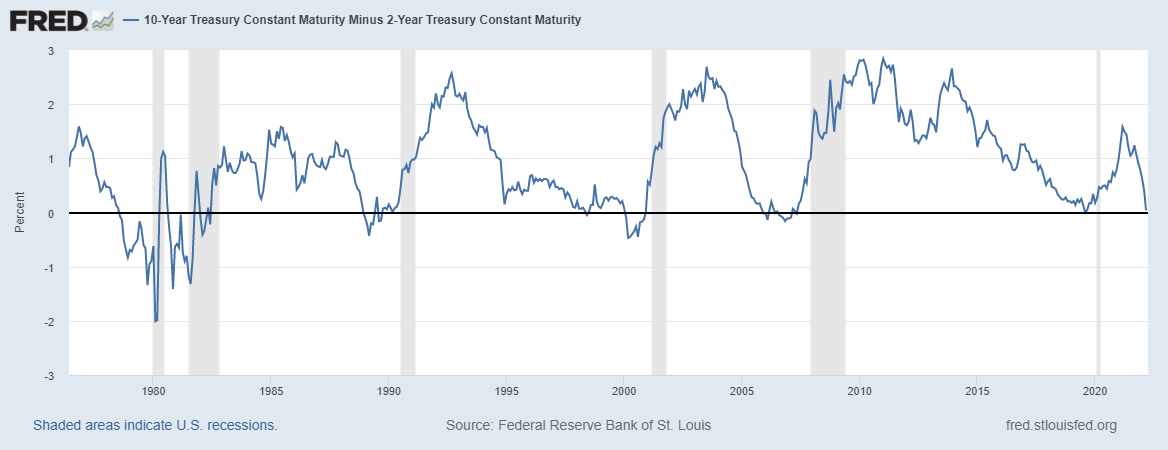

Now for a health check of the economy. Recession red flag No. 3 has been raised: the 2 year yield and 10 year yield inverted.

Recession red flag No. 3: Inverted yield curve

The inverted yield curve is when the 2-year yield and the 10-year yield high-five each other and say hello. The long end of the bond market and short end of the market collide, and stock traders go nuts over this event. Historically speaking, a recession isn’t too far away once this happens as this shows a more mature economic expansion, and the Fed has started its rate-hike process.

Now that this has happened, I need to explain my logic here because I have been on an inverted yield curve watch since Thanksgiving of 2021. Many people were surprised by my statement back then, but it’s the same premise I had at the end of 2017 when I had forecast an inversion in 2018.

2018 was when I crossed off the inverted yield curve for myself. Never one day since then have I talked about recessionary data. The only time I brought up a possible recession was early in 2020 when I spoke of the chaos theory with COVID-19. So, in essence, every American and Russian troll that has been talking about an impending recession since 2010 based on economic data has been wrong. Without COVID-19, we would still be in the longest economic and job expansion ever recorded.

As I write this, the 10-year yield is at 2.375%, and the two-year yield is at 2.43%. So we are inverted by near six basis points.

My 2022 forecast for bond yields did leave an opening for the 10-year yield to get to 2.42% if global yields rise, especially in Japan and Germany. They did it in a significant fashion too. In the previous expansion, when I wrote the bond yield forecast in 2015, they were the same always: we would be in a range between 1.60% – 3%.

“We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.“

The 10-year yield is below the peak 2.42% level and we have an inverted yield curve. My best advice is to ignore this talking point and move on to more important economic data. I am doing this; yes, I checked it off the recession red flag watch.

My recession model shows a progression of an expansion into a recession, and once each red flag is checked, you need to move on. COVID-19 was an anomaly; the economy was expanding. If you want to see how my model worked against the housing bubble, see here.

The other red flags raised were when the unemployment rate was 4%, and the two-year yield was above 0.56%. Also, when the first Fed rate hike happened. Let’s review the three recession red flags that are left: Nos. 4, 5 and 6.

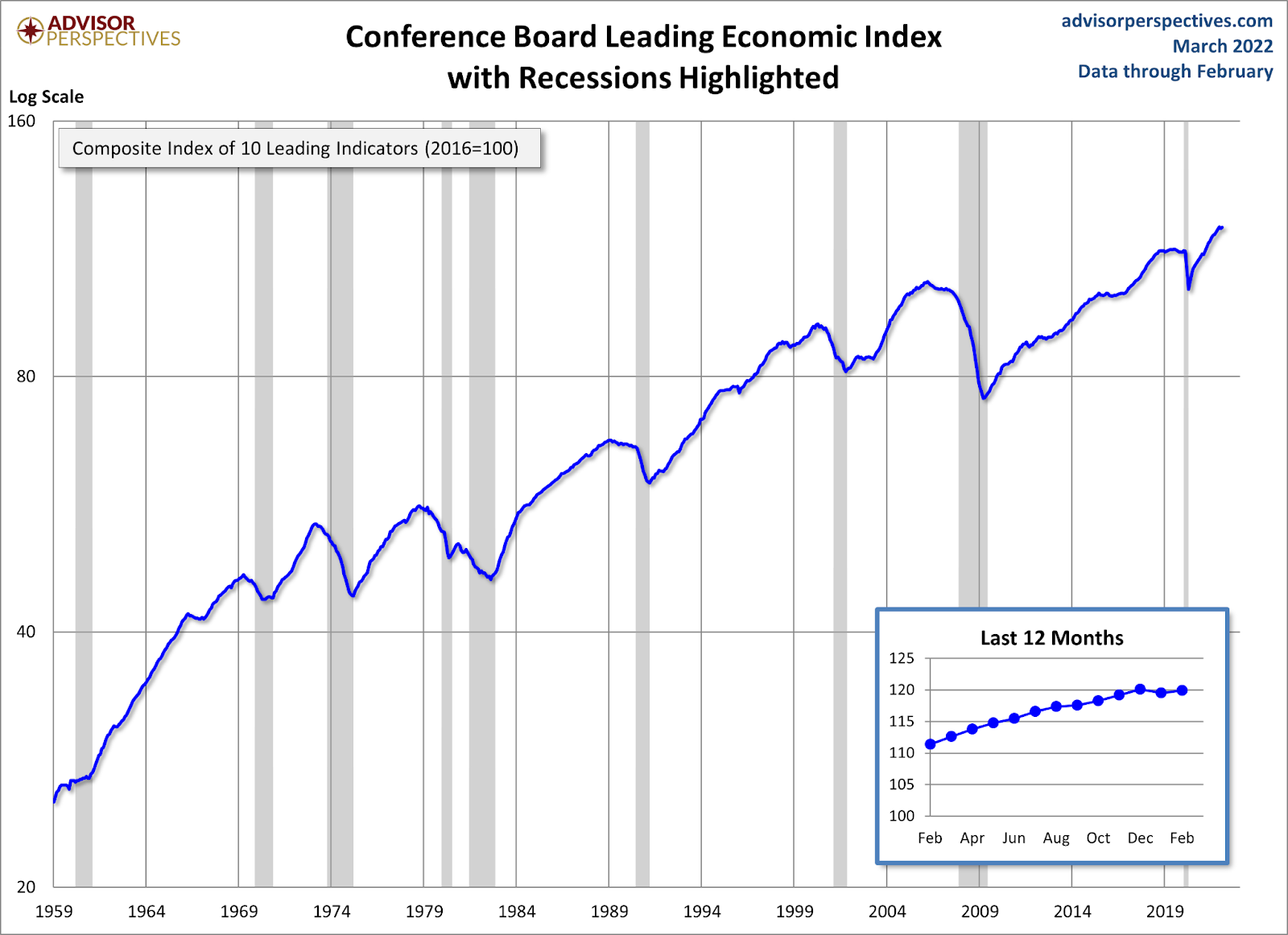

4th recession red flag: The lending economic index fades for four to six months before a recession. Now that the first three red flags are up, we need to be more mindful of this one. We have many components here to work with, and as you can see, excluding COVID-19, this data line has been solid over the decades.

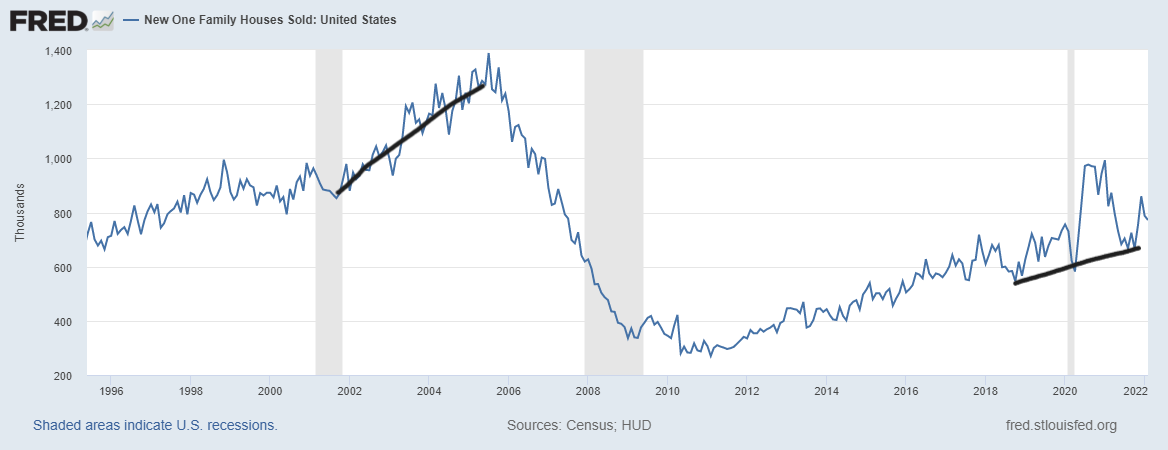

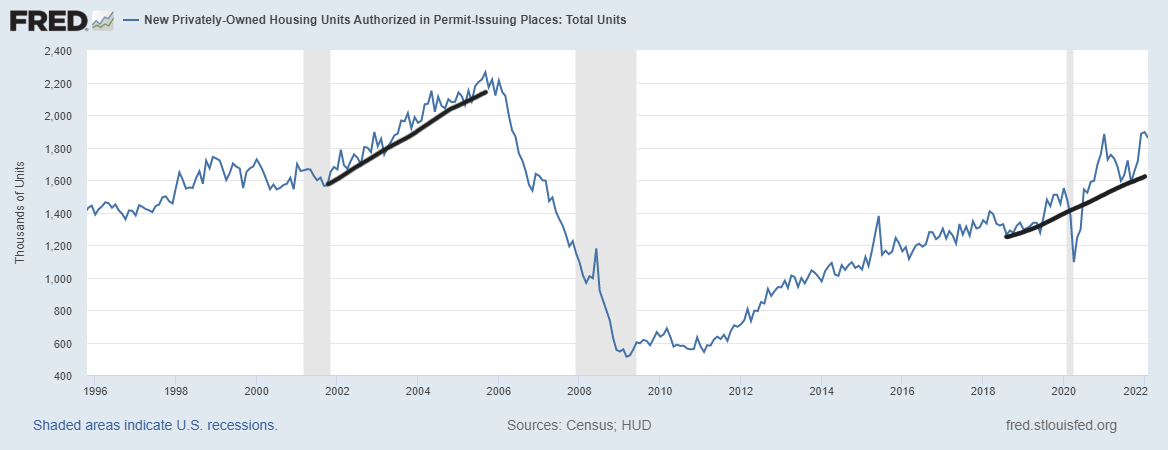

5th recession red flag: Housing starts and new home sales fade into a recession. Now that mortgage rates have spiked, the new home sales and housing start data need to be examined more closely. Read more about that here.

So far, we are still ok on this one.

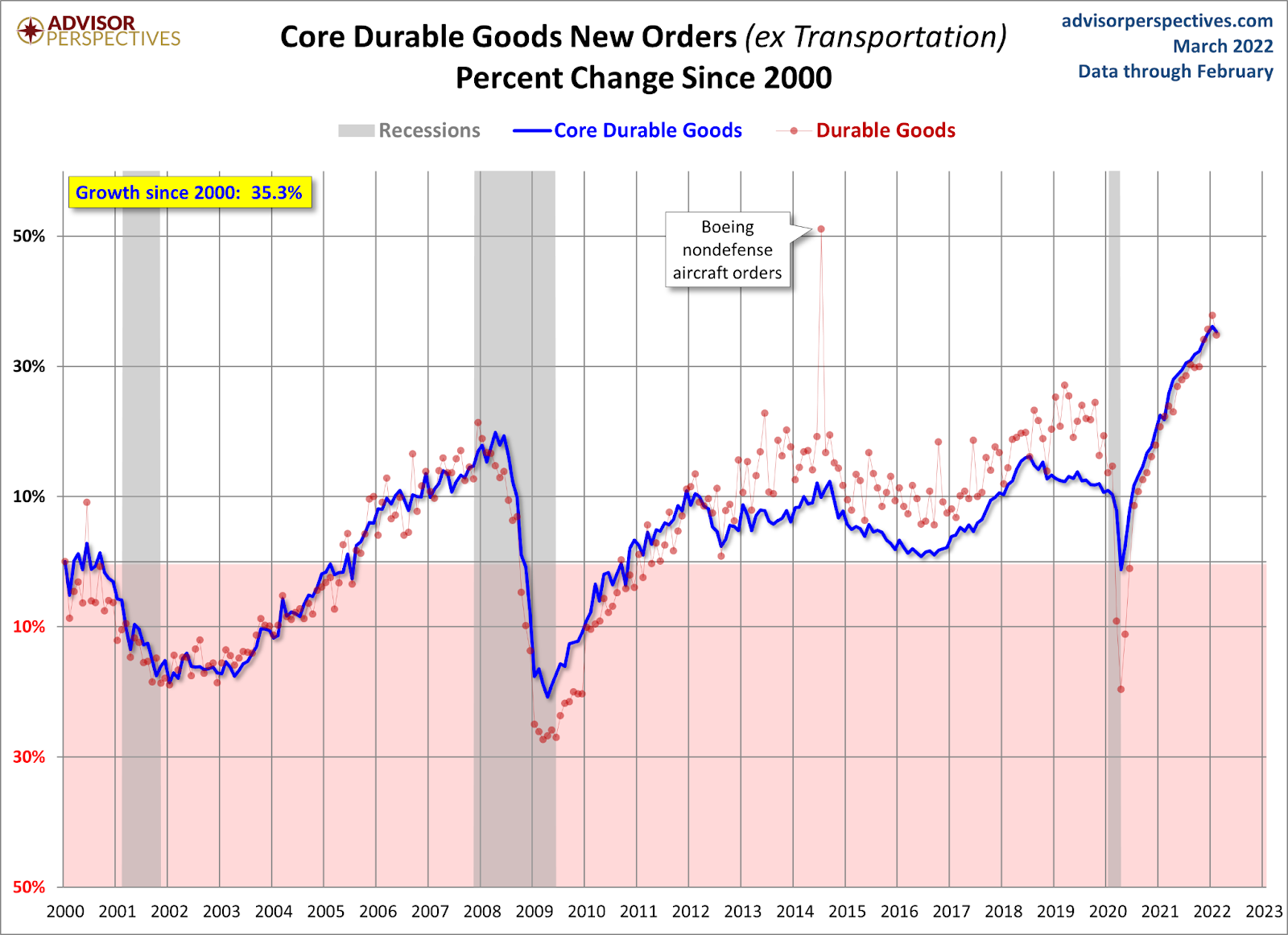

6th recession red flag: Look for where there is over-investment in the economy. Now that three red flags are up, one area that has had booming demand that can’t be sustained is purchasing durable goods. It’s been one of the most amazing things I have ever seen data-wise in my life.

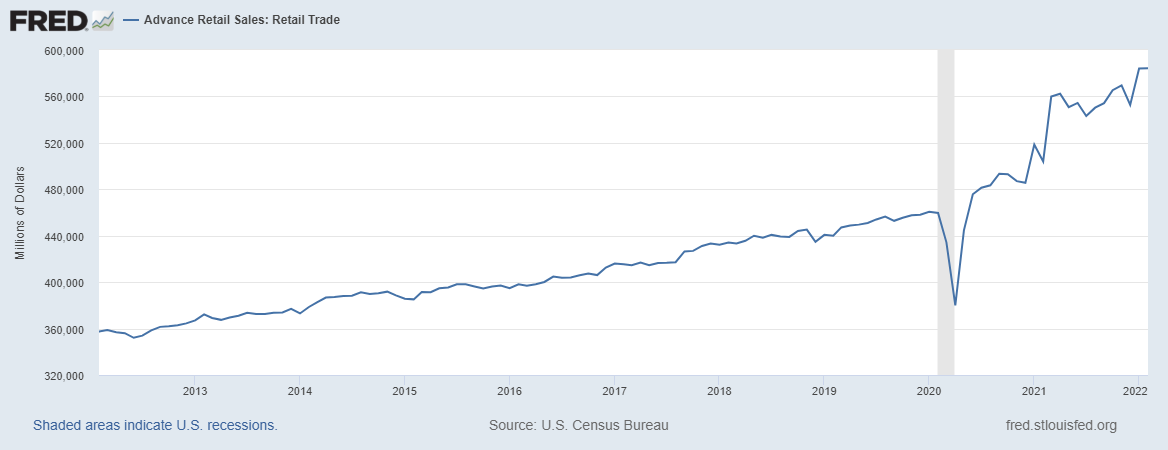

As we can see, retail sales are also off the charts. Now, this data line is moderating from what we saw in 2021. But still, it’s been a historic run of consumption in America.

I will be very mindful of these next three recession red flags. Of course, the Russian Invasion of Ukraine has added a new variable into the mix. Apparently nothing is drama free these days.

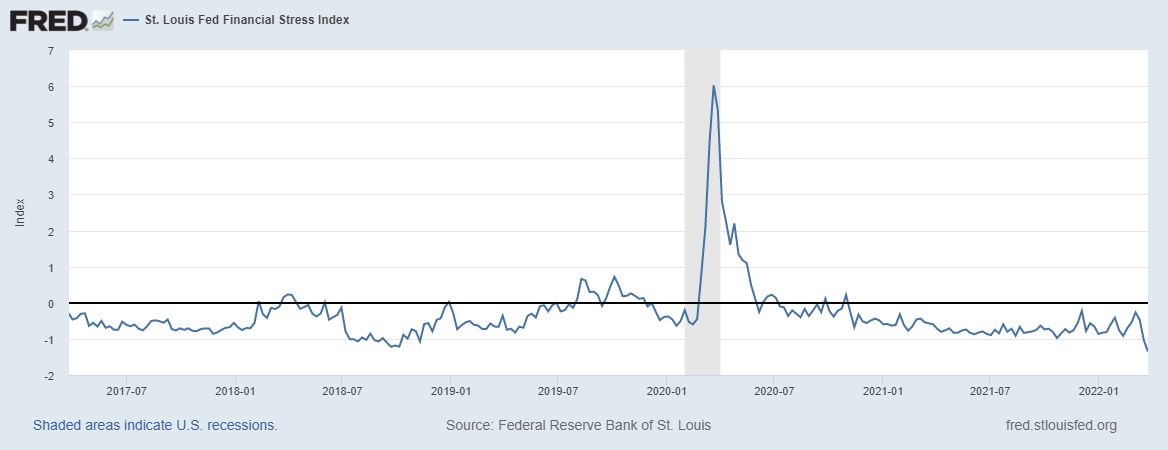

Well, one thing is, The St. Louis Financial Stress Index, which I have been talking about on HousingWire since the COVID-19 crisis, just broke to an all-time low this week.

We will go through this expansion and the next recession together, one data line at a time. I know social media is full of drama people all the time, especially stock traders on Twitter. These people are on a cliff 24/7.

Just remember the two key rules

1. Economics done right should be very boring.

2. Always be the detective, not the troll.

Have a great weekend.