When clients find their dream house and are ready to make an offer, Todd Armstrong’s next call isn’t necessarily to the seller’s agent or the buyer’s loan officer.

“We immediately reach out to an insurance agent to see the insurability of the house because it is becoming more and more of a problem,” Armstrong, a Compass agent in San Diego, told HousingWire’s Brooklee Han in a feature we published Tuesday.

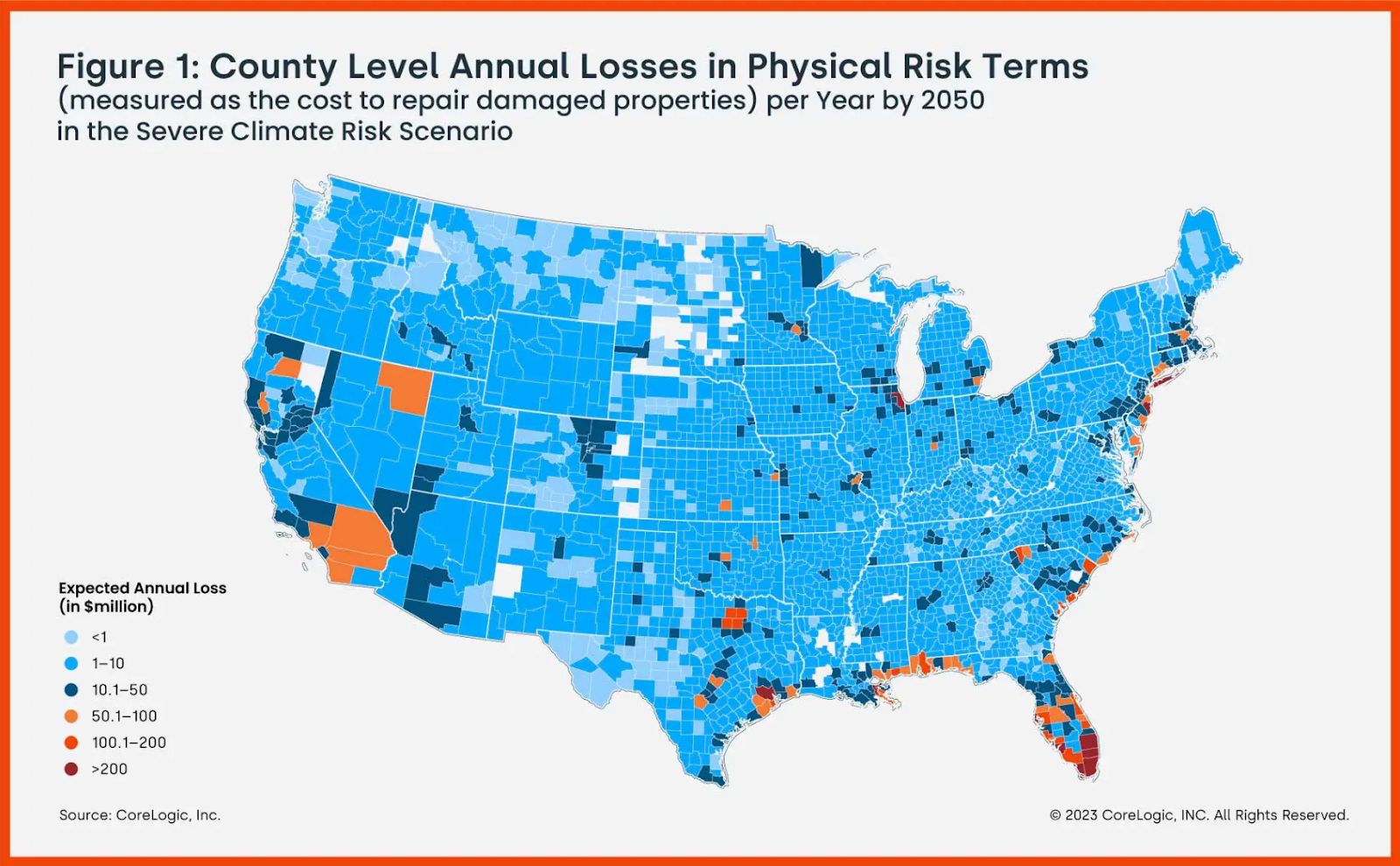

Tight inventory and soaring home prices have pushed more homebuyers to more affordable areas in California. That comes with its own risks – in many cases, wildfires.

Data from CoreLogic shows that the number of homes built in the Very High Fire Hazard Severity Zone (FHSZ) in California has declined to 3.5% over the past 15 years from 5.5%, but building in Moderate FHSZ has nearly doubled since 2008. The fire risk in this zone is less severe, but it is not exactly an unlikely threat either.

Because of historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market, major insurance carriers like State Farm and Allstate are no longer issuing new homeowner insurance policies in California.

The result? Insurance policies for homeowners are skyrocketing. If homeowners can get them at all.

“It is definitely a lot more difficult now than it has been in the past,” Paul Scalone, a San Diego-based Compass agent and the owner of Dignified Insurance Services told Han. “The underwriting requirements for homes are getting a lot more strict. California still has over 100 carriers, but they are scrutinizing the risks a lot more.”

With insurers fleeing the state, the California FAIR Plan, the state’s insurer of last resort, saw enrollment jump to 272,846 homes in 2022. That number will undoubtedly climb in the coming years.

Scalone recently wrote a policy for clients buying a home in Claremont, the Serra Mesa area of San Diego, which he described as a “pretty urban environment.”

“A year or two ago that would have been a slam dunk, no questions asked,” he told Han. “But it probably took me two or three weeks of back and forth with multiple carriers, answering an array of different questions and submitting documentation and photos of the home before we got a carrier to agree to take the risk. It is just a sign of the times here in California.”

In Florida, agents are also grappling with insurability issues that are relatively new and vexing. I don’t just mean mandatory flood insurance, which itself has gotten quite a bit more expensive. But regular ‘ol homeowners insurance in less flood-prone areas is becoming unaffordable for some.

“I do a lot with new construction and homeowners’ insurance is cheaper on new builds because they are brand new,” said Sandy Williams, an eXp Realty agent in Sarasota. “With material and labor shortages, and supply chain issues, it is taking a year-and-a-half to two years to complete a property. A lot of my clients will get insurance quotes three months into the project and then about a year later they are getting their final quote. One of my recent new homebuyers got their final quote on a property a 30-minute drive from the coast and it had gone up 40% from a year ago. This is one of the easiest parts of Florida to insure and costs have gone up over 40%.”

Jacob Watkins, the broker-owner of Corcoran Reverie in the state’s 30A region along the Gulf of Mexico, told Han the insurance issues have changed how agents like him identify properties for clients.

“Prior to now we never really had to pay all that much attention. Insurance was typically not a big factor in the decision-making process, but given the cost now and even the availability of what properties can easily be insured and what cannot is definitely a factor in what properties our customers are looking at and considering.”

According to Redfin, in the past two years, nearly 60,000 more people moved into than out of Lee County, Florida, which includes Fort Myers and Cape Coral, and was slammed by Hurricane Ian in September. That’s the largest net inflow of the 306 high-flood-risk counties Redfin analyzed, and represents an increase of about 65% from the prior two years.

Florida is home to eight of the 10 high-flood risk counties that experienced the largest net inflows of people over the past two years(!). And in case you’re wondering, the counties with the highest wildfire risk saw 446,000 more people move in than out over the past two years, a 51% increase from 2019 and 2020.

People will continue to move into these higher-risk areas because we just haven’t built enough housing in areas with less climate-related risk. Will that translate into a negative impact on property values? Maybe.

In a CoreLogic study that examined the 19 counties impacted by the five largest fires recorded in California’s history (all of which occurred in 2020) the price of properties in the fire perimeter declined 0.64% between June 2021 and May 2023. By contrast, the average price appreciation during the same two-year time period for the state as a whole was 12.3%.

Check out Han’s excellent feature here.

In our weekly DataDigest newsletter, HW Media Managing Editor James Kleimann breaks down the biggest stories in housing through a data lens. Sign up here! Have a subject in mind? Email him at [email protected].