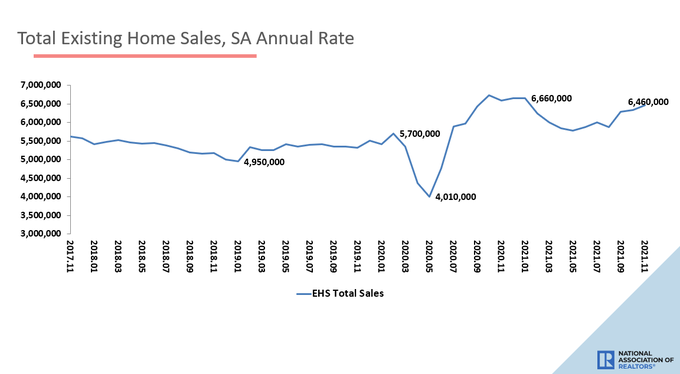

The National Association of Realtors reported that existing home sales for November came in hot at 6.46 million. This number is above my sales trend peak of 6.2 million, which means we have now had three straight months of sales of over 6.2 million.

Early in the year, I wrote that if existing home sales stay in a range between 5.84 million and 6.2 million, that would mean it’s a good year for housing demand. We ended 2020 with 5.64 million, so every single existing home sales print in 2021 has been higher than what we closed in 2020 — which was higher than any single year from 2008 to 2019.

Regarding the sales range for 2021, I had anticipated a few prints under 5.84 million and we only had one print under that number. Now, sale trends are growing into 2022 with a more positive tone. The housing crash addicts in America had a terrible 2020 and 2021: I have always stressed that these people are professional grifters, not housing analysts.

However, before we go into this report, I have to explain why so many people missed this surge in demand in the second half of 2021. It’s the same reason I have given for many years: the American bears who are typically housing crash addicts can’t read data correctly, and the mortgage purchase application data just proved my point once again.

Early in the year, I talked about how the purchase application data would be negative year over year in the second half of 2021 due to the make-up demand in 2020 creating abnormal high comps. Typically, volumes always fall after May, but of course 2020 was an abnormal year.

Knowing that the housing crash addicts on YouTube, Twitter, Facebook, and Clubhouse would incorrectly push the negative year-over-year data spin, I wanted to get ahead of that narrative. Then everyone went crazy on investors and iBuyers, suggesting that these people were holding up the entire housing market. I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers.

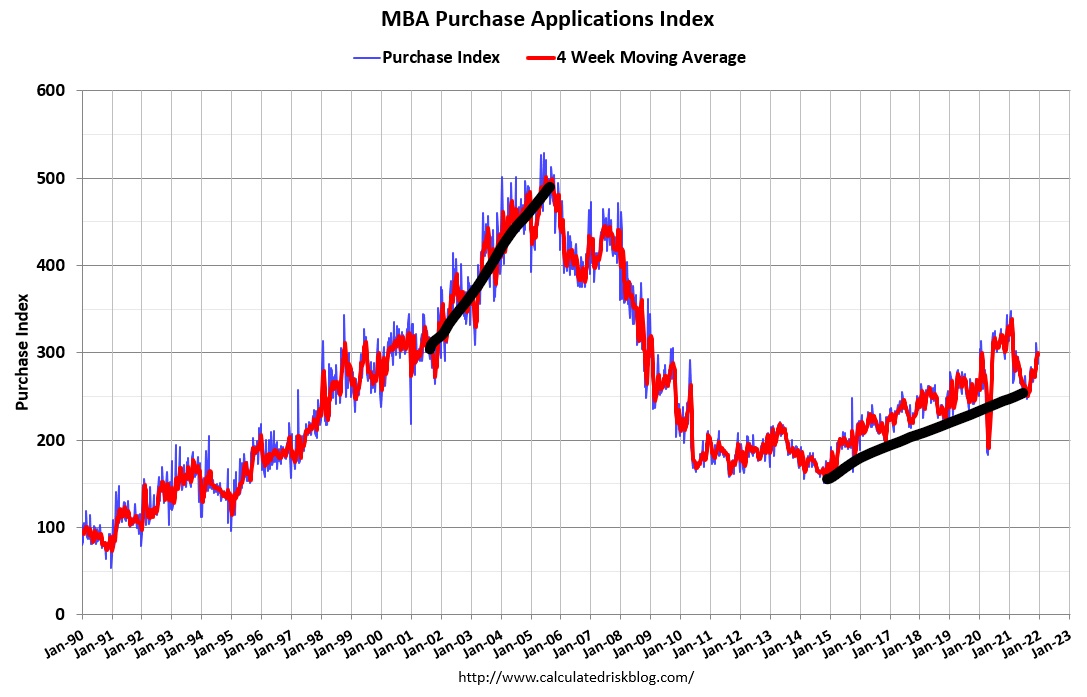

What has happened is that purchase application data made a noticeable push higher in the year-over-year data starting 16 weeks ago. So for four months, this data line was getting better and better, and so many people ignored it because they didn’t know where to look. Since September, we have had a double-digit year-over-year growth trend, which is a big deal in this data line while the data was still showing negative growth year over year.

This would have been easy to spot if you had made COVID-19 adjustments to the data and recognized that the year-over-year declines were getting much less. Now, we can see why existing home sales, pending home sales, builders confidence, housing starts, and housing permits look better toward the end of the year: we are back to that 300 level in the MBA index that I have often talked about.

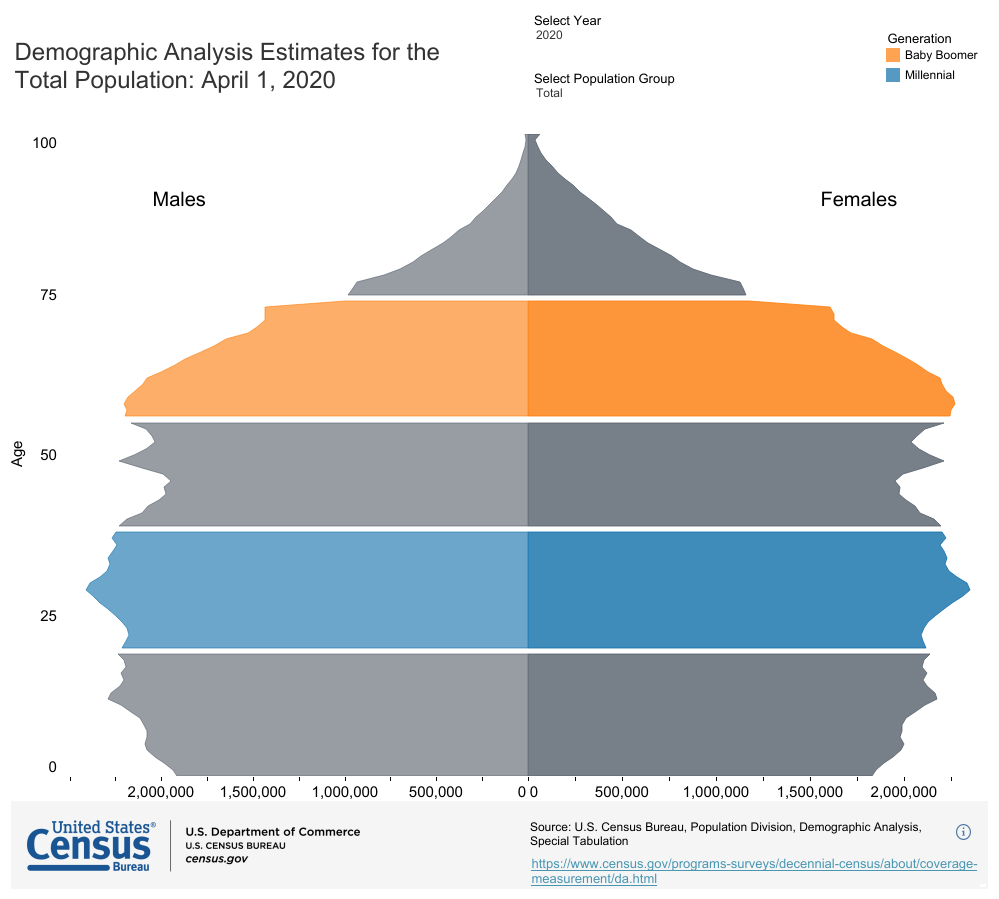

As you can see below, we don’t have a booming credit housing market as we saw from 2002-2005; we have steady replacement buyer demand. In 2020-2024, we just have that kick from the most prominent housing demographic patch ever recorded in history, as ages 28-34 are the biggest in America and need somewhere to live. You don’t need to make it any more complicated than that.

All this information was available for people to read in the Census data — it wasn’t hidden. I can understand if this was the 1500s and you needed to dispatch horses to get information that might come to you many months or years later. However, it’s 2021. We have the internet, access to census data is open to the public, and reading is a good thing.

This is why I stress my two rules always when talking about economics:

- Economics done right, should be boring

- You always want to be the detective, not the troll.

Anyone who has been predicting a housing crash every year from 2012-2019, then went all-in during 2020, only to double down in 2021 and push for a second-half crash in 2021 — you have all lost your privileges to talk about housing ever again.

Now on to the report and some of the details from NAR.

Home sales

From NAR: Total existing-home sales completed transactions that include single-family homes, townhomes, condominiums, and co-ops, grew 1.9% from October to a seasonally adjusted annual rate of 6.46 million in November.

As discussed, sales trends are now above my 6.2 million level for three straight months, aligning with the better mortgage demand growth that we saw for four months. Typically, purchase application data looks out 30-90 days, and we know that we will be dealing with COVID-19 comps to mid-February. One last item with existing home sales, our best sales prints the previous year, this year, and even in the previous expansion have all come in the winter and fall, not the spring or summer. This is a fact that not many people consider.

Home prices and days on market

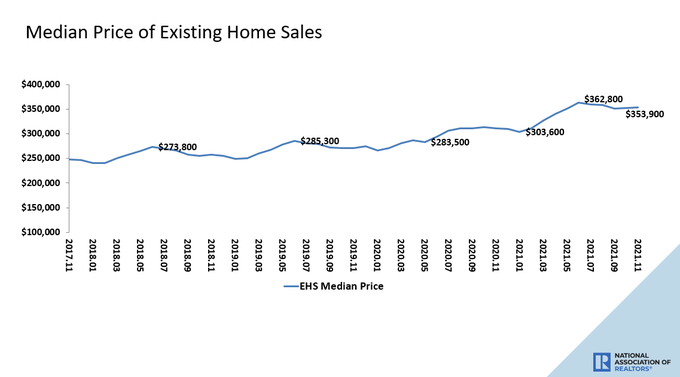

From NAR: In November, the median existing-home price for all housing types was $353,900, up 13.9% from November 2020 ($310,800), as prices increased in each region, with the highest pace of appreciation in the South region.

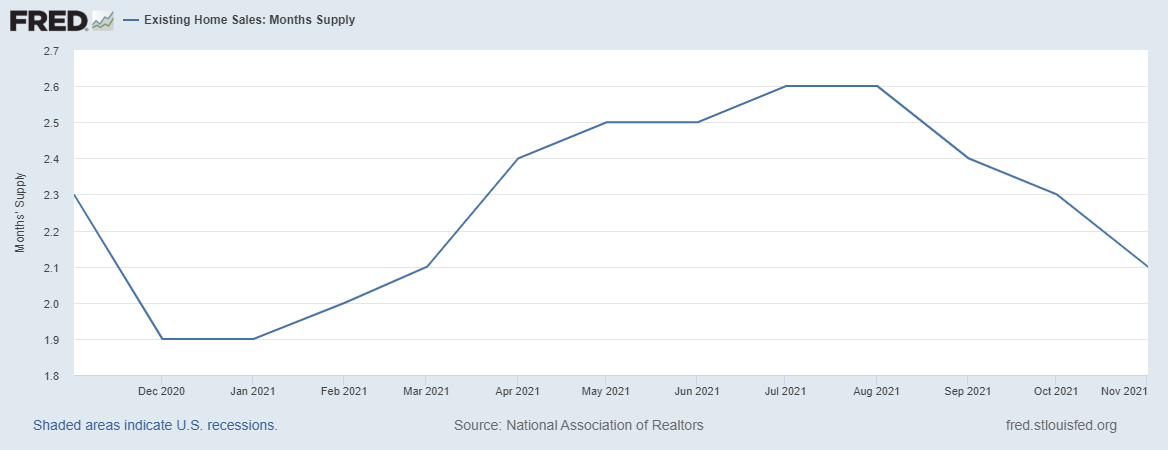

For every positive, we do have a negative, and as we can see, the housing world is just different in the years 2020-2021 than what we saw from 2008-2019 regarding home prices. While the growth rate or pricing is slowing because we don’t have a credit boom in housing, the increase in prices in the first two years of my 2020-2024 time period has reached my comfort zone of cumulative price growth of 23%. Higher mortgage rates would create more days on the market, but this would mean the 10-year yield getting above 1.94% with duration in 2021, which wasn’t part of my forecast in 2021 and 2022.

A positive outcome for me in 2022 would be to see days on the market grow above the teenager age. More choices are better for homebuyers and sellers who need to buy a home typically as well.

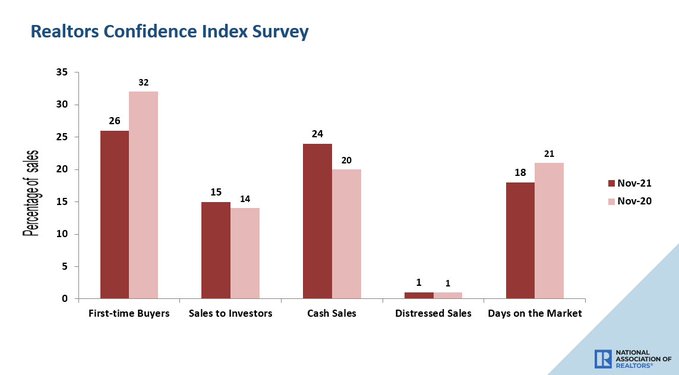

From NAR: First-time buyers were responsible for 26% of sales in November; Individual investors purchased 15% of homes; All-cash sales accounted for 24% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 18 days.

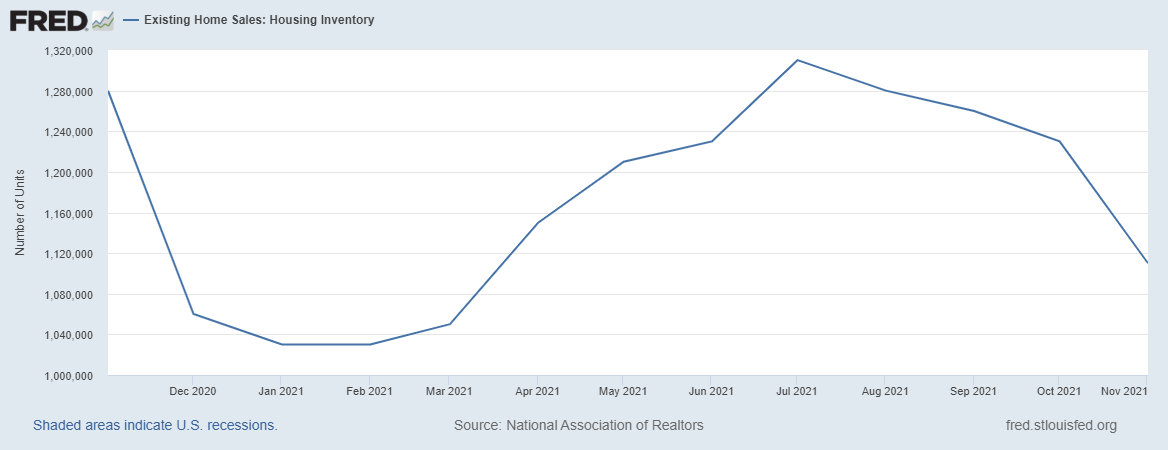

Now for the real bad news, which is still a first-world problem, but the big concern for me during 2020-2024: inventory.

Seasonality has kicked in with inventory already, which is expected every year. However, I had hoped that we wouldn’t start spring 2022 with all-time lows in inventory. Unfortunately, that can’t be ruled out anymore and we might have a shot at a fresh new all-time low going into the spring of 2022 with mortgage rates under 4% still. Yikes!

The target level for me to stop talking about the unhealthiness of this housing market is to see inventory levels between 1.52 – 1.93 million. While this is still meager inventory historically, it will bring more balance into the market, and I can call it a B&B market: boring and balanced. Until then, it’s still the hunger games for housing.

As we end the year on a positive note and we still have one more existing report month left, we can clearly see that housing is driven by demographics and mortgage rates and those who pushed terrible Forbearance Crash narratives didn’t even get coal for Christmas.

If you want to read about my 2022 Housing and Economic Forecast you can find that here, or if you would rather listen than read, I provided an overview of the forecast on this episode of the HousingWire Daily podcast.