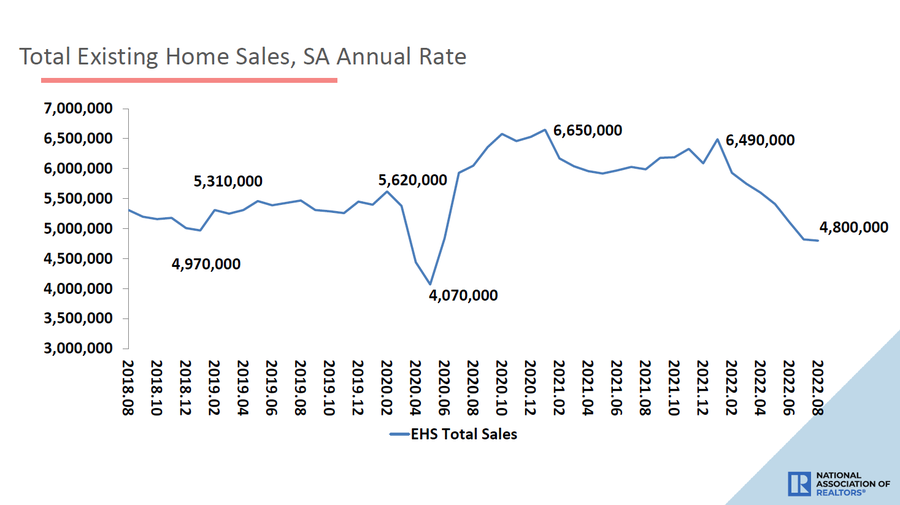

Today the National Association of Realtors reported that existing home sales fell once again to 4.80 million. Even though this was a beat of estimates, the sales decline trend due to higher mortgage rates and home prices continues. The savagely unhealthy housing market theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates.

With the home-price growth we had in 2020 and 2021, my five-year price-growth model that I set for 2020-2024 of 23% was already smashed in just two years. That was a huge red flag, hence all the statements in 2021 about unhealthy housing.

However, the secondary negative impact was going to be more painful. Since the summer of 2020, I have talked about what could change the housing market, which was a 10-year yield above 1.94%, which means rates over 4%. Now that mortgage rates are over 6%, this one-two punch of rising prices and rising rates is the core basis of the savagely unhealthy housing market.

From NAR Research: “Total existing-home sales notched a minor contraction of 0.4% from July to a seasonally adjusted annual rate of 4.80 million in August.”

Existing home sales have more legs to go lower, especially now that new listing data is falling. A traditional primary resident seller is also a buyer, which means if they don’t list, they’re not just taking a potential home to be bought off the table — they’re taking a future sale off the books as well.

Total Inventory data fell in this report from 1.31 million to 1.28 million. It doesn’t even look like we will breach the lower level of my inventory wish list of 1.52 to 1.93 million this year: Savage, man, purely savage.

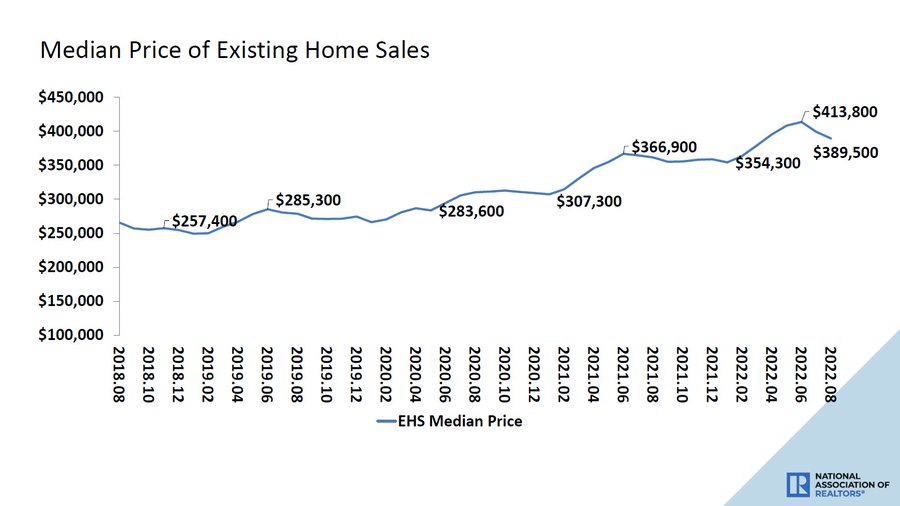

From NAR: “The median existing-home price for all housing types in August was $389,500, a 7.7% jump from August 2021 ($361,500), as prices ascended in all regions. This marks 126 consecutive months of year-over-year increases, the longest-running streak on record.”

While home prices have been up in every report this year, the price growth is cooling on a year-over-year basis. I am a big fan of inventory to 2019 levels. We have parts of the U.S. that are at 2019 levels, and they are off the savagely unhealthy housing market list. Even though 2019 inventory levels were historically low, they were at four-decade lows before 2020; they’re a more effective pricing market.

NAR Research “The total housing inventory registered at the end of August was 1,280,000 units, a decrease of 1.5% from July and unchanged from the previous year. Unsold inventory sits at a 3.2-month supply at the current sales pace – identical to July and up from 2.6 months in August 2021.”

Due to the revisions to last month’s data, monthly supply data didn’t grow. It would have fallen slightly from last’s 3.3 monthly print, which was revised to 3.2 months. I prefer four months of supply nationally to be balanced. However, seasonality will kick in soon, and it doesn’t look that 2022 will get us there. Unlike most people, I believe a balanced market is a four-month story, not the six months people have talked about over the years. We can have effective pricing in a four- to five- month housing supply market, so four months is my goal.

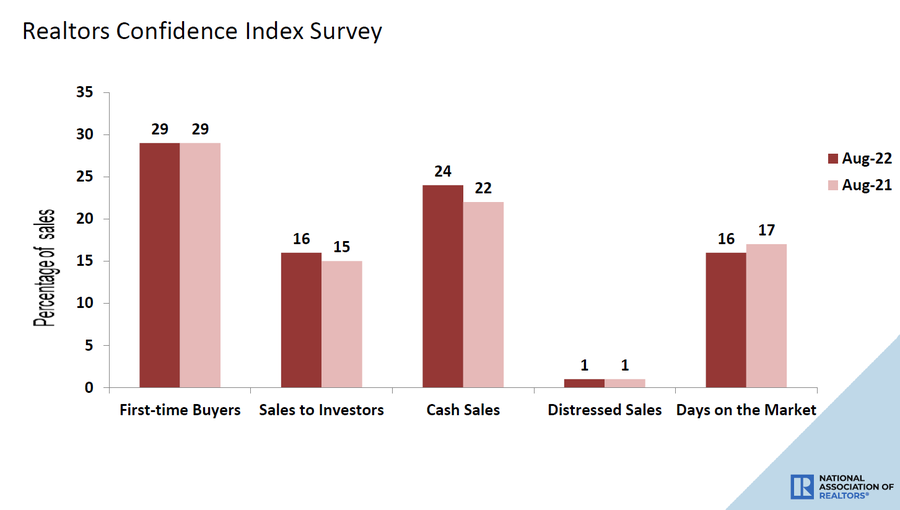

NAR Research: “First-time buyers were responsible for 29% of sales in August; Individual investors purchased 16% of homes; All-cash sales accounted for 24% of transactions; Distressed sales represented approximately 1% of sales; Properties typically remained on the market for 16 days.”

The days on the market have always been a critical data line for me. Nothing is good when the data line is low. I prefer 30 days plus, meaning it’s a more typical marketplace with choices for people all over the country.

On the good side, the days on the market in August grew to 16 days coming off historic all-time lows of 14 days. Homes priced right are selling in America, and homes that are not waking up to reality are staying on the market longer and longer.

Since total inventory levels are so low, this data line has broken to all-time lows, which alarms me. We simply didn’t have enough housing products for people post 2020. This explains the historical price growth since 2020 and why prices are still up yearly, even in a market with sales falling year over year.

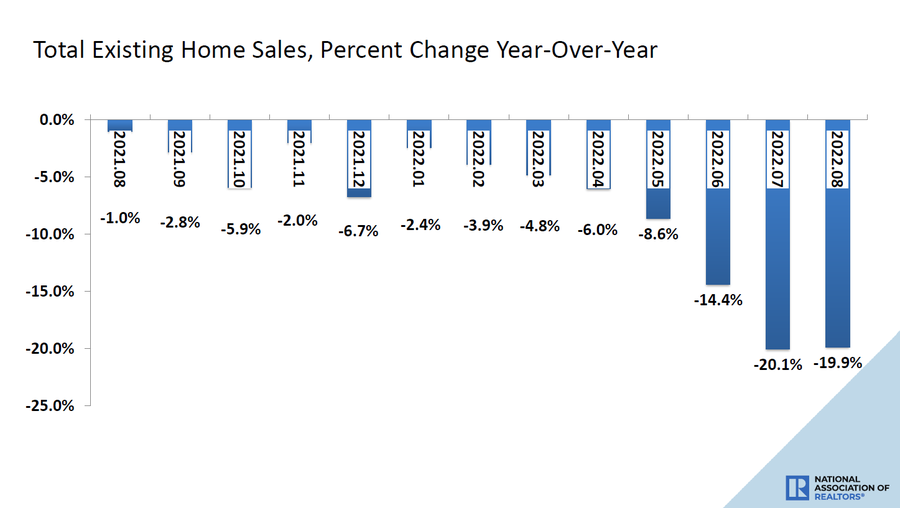

NAR Research: “Year-over-year, sales faded by 19.9% (5.99 million in August 2021).”

We have entered a period in time where we have high comps for housing demand, and the year-over-year data is going to get worse until 2023 because existing home sales, just like purchase application data, made a run toward the end of the year, sending existing home sales toward 6.49 million in January of 2022.

I have talked about this often with purchase application data, that we should expect some significant year-over-year declines for the rest of the year, of 25% to 35%. Even if the weekly data doesn’t go anywhere, with rates heading higher, you can see drops of 40% + due to the high comps and higher mortgage rates.

All in all, the report looks right to me. Some people might be surprised that total inventory fell, but with the new listing data declining since late June of this year, it’s not a shock to me that this is happening.

Is this the first stage of a mortgage rate lockdown? We don’t want to see that in America, but that might be a reality in 2023. Home-price growth is falling as it should; we have had a massive housing inflationary event in America with rising home prices and mortgage rates coming off hot 2020 and 2021 prices. With mortgage rates rising, 2022 has seen the most significant housing inflationary event in recent modern history as the total cost to buy a home took a historic run higher, one that is for the record books.

I have worried about this trend since mid-February, and unfortunately the housing market is still savagely unhealthy for most of the country. However, it’s not the market of 2002-2011. Different dynamics are at play here, so the economic discussion has to be different.