The Census Bureau‘s housing starts report for December shows that housing completions are still too slow, and we are running out of time this year as housing permits are set to fall until the homebuilders get rid of their excess supply.

We had some good news this week for the housing market: purchase application data is up, the builder’s confidence index rose to beat estimates, and the 10-year yield and mortgage rates have fallen. However, even though the headline number of the housing starts report beat estimates, the internals of the report aren’t great as housing completion data once again is still just grinding and not yet breaking out.

The best way to deal with inflation is to add more supply, not to destroy demand, which in time, will ruin production. One area where we have gotten lucky in this housing cycle is that the builders still have a backlog of orders they need to build and put into the market. After that, we’ve got nothing to add as housing permits have room to fall all year.

My economic work differs from other people’s because I don’t believe the builders were under-built in the last economic expansion. My entire working premise in the previous expansion was that we would have the weakest housing recovery ever, from 2008-2019, and that we wouldn’t have housing starts open a year at 1.5 million until 2020-2024, when demand would finally warrant that type of construction.

New home sales missed estimates from 2013 to 2015. Then in 2018, we had a monthly supply spike in the new home sales market, which kept the builders from wanting to produce more housing units for 30 months.

As I have stressed for years, the builders are not running a charity, they need to make money on their homes, and they won’t ever oversupply a market to ruin their business model. So, what I am hoping for in 2023 is that completion data grows as fast as possible because we don’t have much in the pipeline after that.

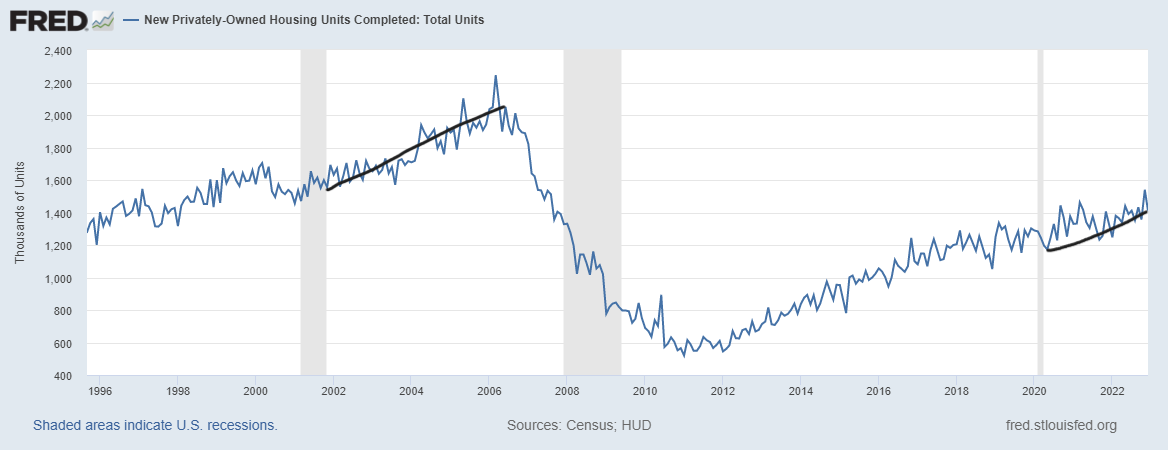

Housing completion

From Census: Housing Completions Privately owned housing completions in December were at a seasonally adjusted annual rate of 1,411,000. This is 8.4 percent (±16.5 percent)* below the revised November estimate of 1,540,000, but is 6.4 percent (±11.4 percent)* above the December 2021 rate of 1,326,000. Single-family housing completions in December were at a rate of 1,005,000; this is 8.0 percent (±11.6 percent)* below the revised November rate of 1,092,000. The December rate for units in buildings with five units or more was 385,000. An estimated 1,392,300 housing units were completed in 2022. This is 3.8 percent (±3.3 percent) above the 2021 figure of 1,341,000.

Below is one of the saddest economic charts you will ever see. Housing completion is so slow that my tortoise, Grundy, looks like the flash next to it. We need more rental supply to hit the markets, so the growth rate of shelter rental inflation falls faster.

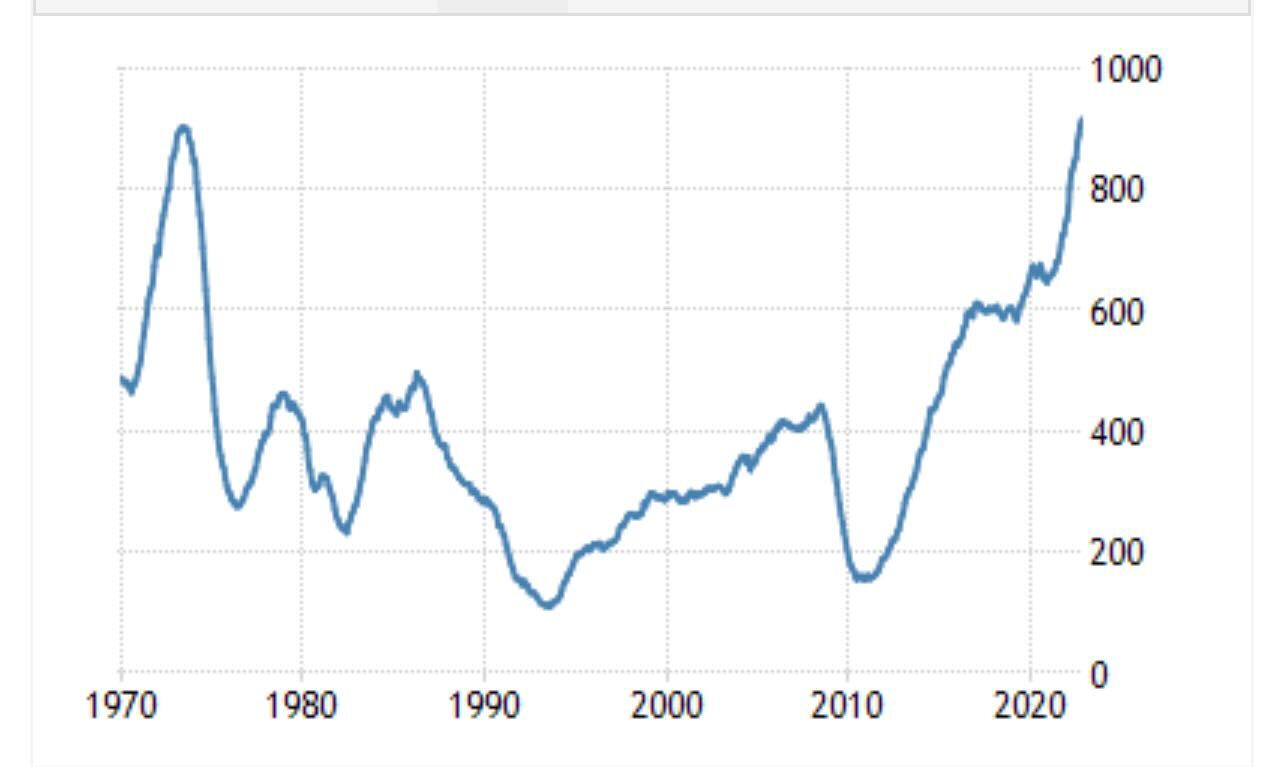

Fortunately, as you can see in the chart below, the number of housing units (five units or more) under construction is historically high. There are 943,000 apartments currently under construction. This is bullish for America and for mortgage rates to head lower.

Housing Permits

Building Permits: Privately-owned housing units authorized by building permits in December were at a seasonally adjusted annual rate of 1,330,000. This is 1.6 percent below the revised November rate of 1,351,000 and 29.9 percent below the December 2021 rate of 1,896,000. Single‐family authorizations in December were at a rate of 730,000; this is 6.5 percent below the revised November figure of 781,000. Authorizations of units in buildings with five units or more were at a rate of 555,000 in December. An estimated 1,649,400 housing units were authorized by building permits in 2022. This is 5.0 percent below the 2021 figure of 1,737,000.

Housing permits have room to fall all year long; we are still in the stabilization period of housing demand, not in the growth phase yet. So, don’t expect housing permits to change this year unless demand improves. As you can see below, housing permits aren’t working from the elevated levels we had in 2005. The builders are in a much better position this time than they were in 2005-2008.

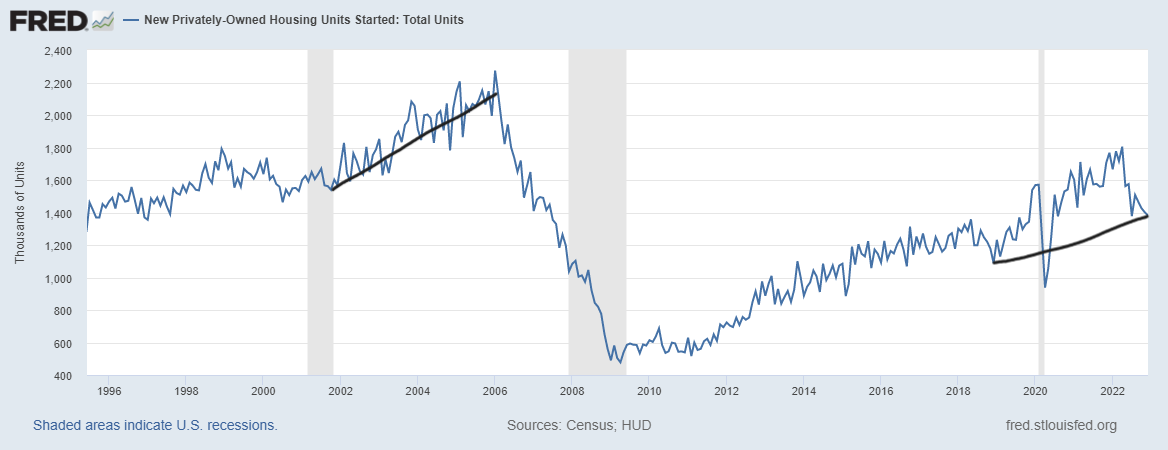

Housing starts

Housing Starts: Privately-owned housing starts in December at a seasonally adjusted annual rate of 1,382,000. This is 1.4 percent (±16.9 percent)* below the revised November estimate of 1,401,000 and is 21.8 percent (±11.2 percent) below the December 2021 rate of 1,768,000. Single-family housing starts in December were at a rate of 909,000; this is 11.3 percent (±20.7 percent)* above the revised November figure of 817,000. The December rate for units in buildings with five units or more was 463,000. An estimated 1,553,300 housing units were started in 2022. This is 3.0 percent (±2.4 percent) below the 2021 figure of 1,601,000.

Housing starts will be trending lower this year as well since the builders have a backlog of homes they need to finish building. There is no appetite from the builders to start building permits for single-family units as long as new home sales are low.

New home supply and builder confidence

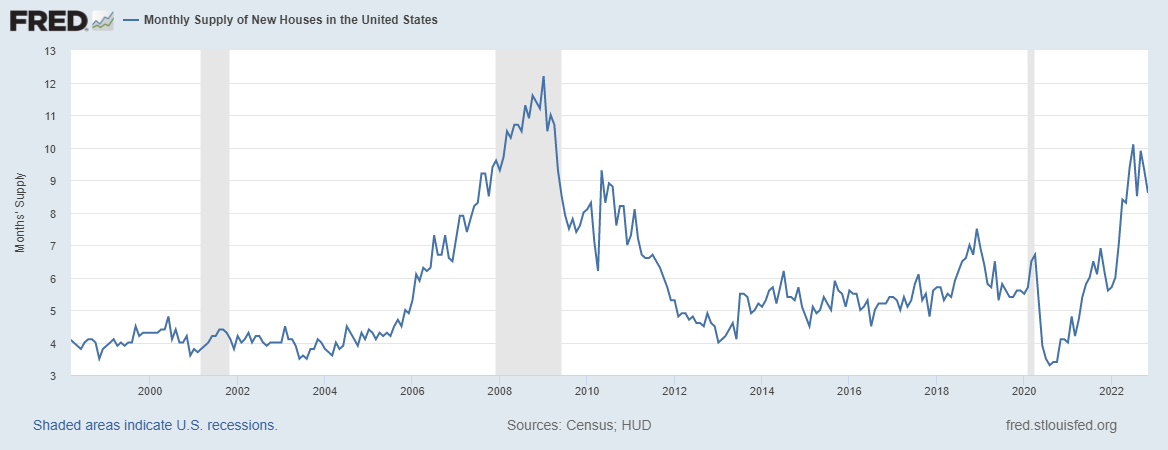

My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market; this monthly supply data only applies to the new home sales market.

- When supply is 4.3 months and below, this is an excellent market for builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

In the last report, for November, the monthly supply of new homes was still too high at 8.6 months, so the builders still need to move more products before thinking about growth again.

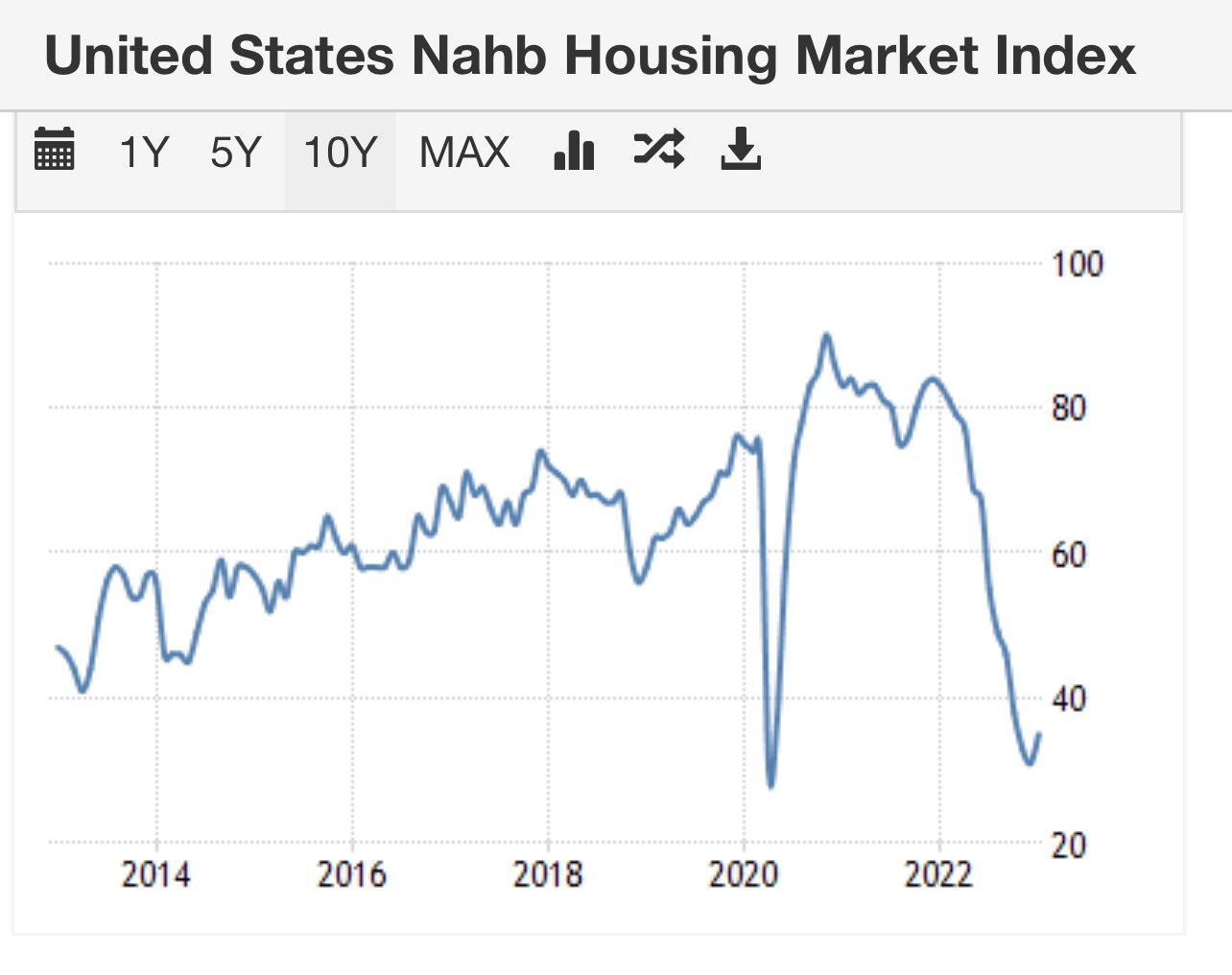

This week’s good news is that the builder’s confidence data finally rose after a waterfall dive in this index. In the previous month, the forward-looking data of the survey was positive, while the other data were still negative. That is not the case anymore, as you can see below. The total report was good, with the headline number beating estimates.

All in all, even though the headline number beat estimates, I am taking a longer view on this economic sector: it’s still in a recession until we can get the builder’s confidence up, the monthly supply of new homes down, and permits to start rising again.

All I am hoping for in 2023 is to get as many housing units completed and into the market to deal with rental inflation data, as that is the biggest driver of core CPI inflation. Over the long run, more housing supply will keep a lid on rent inflation getting out of hand.