Timed for release alongside a congressional hearing devoted to reverse mortgages last week, a government watchdog is detailing its program recommendations in a new 106-page report.

The report, “Reverse Mortgages: FHA Needs to Improve Monitoring and Oversight of Loan Outcomes and Servicing,” goes into significant detail concerning perceived “weaknesses” that were found in the HECM program during the GAO review, identifying deficiencies in performance evaluation of the program and a substantial increase in defaults over a four-year period. The report then makes a series of recommendations designed to address these issues.

Problems found by GAO

One of the major problems identified within the HECM program by GAO is a substantial increase in borrower default rates.

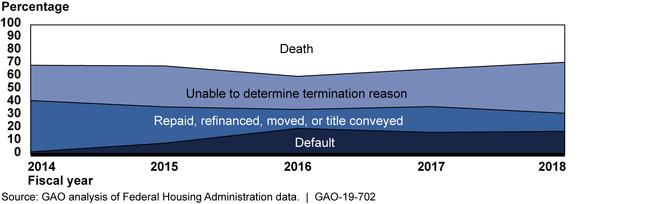

“In recent years, a growing percentage of HECMs insured by FHA have ended because borrowers defaulted on their loans,” the report reads. “While death of the borrower is the most commonly reported reason why HECMs terminate, the percentage of terminations due to borrower defaults increased from 2 percent in fiscal year 2014 to 18 percent in fiscal year 2018.”

While the number itself represents a substantial increase default rates over a short period of time, GAO also specifies the most common reasons for reverse mortgage default.include borrowers not meeting occupancy requirements or failing to pay property charges, such as property taxes or homeowners insurance. Yet many are not using the tools available to prevent defaults from taking place, GAO says.

“Since 2015, FHA has allowed HECM servicers to put borrowers who are behind on property charges onto repayment plans to help prevent foreclosures, but as of fiscal year-end 2018, only about 22 percent of these borrowers had received this option.”

The GAO points to lack of effective communication and information-gathering practices throughout the report, whether between borrowers and servicers or government agencies and program stakeholders. GAO also found that as much as 30% of documented HECM terminations do not feature a recorded reason behind why those terminations actually take place, while FHA has also not developed comprehensive performance indicators for the HECM portfolio.

“[FHA] has not regularly tracked key performance metrics, such as reasons for HECM terminations and the number of distressed borrowers who have received foreclosure prevention options,” the report’s findings read. “Additionally, FHA has not developed internal reports to comprehensively monitor patterns and trends in loan outcomes. As a result, FHA does not know how well the HECM program is serving its purpose of helping meet the financial needs of elderly homeowners.”

Additionally, GAO states that FHA has not conducted any on-site reviews of HECM servicers since the 2013 fiscal year, and has not effectively communicated with the CFPB based on that agency’s oversight and enforcement actions taken against reverse mortgage lenders. While FHA reportedly plans on resuming HECM servicer reviews in fiscal 2020 by starting with the three most prominent servicers, the lack of sufficient information sharing agreements could lead to similar mistakes in the future if those shortcomings are not addressed.

“As of August 2019, FHA had not developed updated review procedures and did not have a risk-based method for prioritizing reviews,” the report reads. “CFPB conducts examinations of reverse mortgage servicers but does not provide the results to FHA because the agencies do not have an agreement for sharing confidential supervisory information. Without better oversight and information sharing, FHA lacks assurance that servicers are following requirements, including those designed to help protect borrowers.”

Recommended solutions

GAO makes a series of eight recommendations to both FHA and CFPB that could address many of the program’s shortcomings found in its review of the HECM program. Most of the recommendations are designed to, “improve [FHA’s] monitoring and assessment of the HECM portfolio and oversight of HECM servicers, and one recommendation to CFPB to share HECM servicer examination information with FHA,” the report reads.

If implemented, the majority of the agency changes would require action from FHA Commissioner Brian Montgomery, who is also the current Acting Deputy HUD Secretary. The specific content of those changes would ask FHA to “improve the quality and accuracy” of HECM termination data; periodically review and report on HECM program performance indicators; develop analytic tools to “better monitor outcomes” for the HECM portfolio; institute an evaluation procedure of FHA’s foreclosure prioritization process for FHA-assigned loans; and spearheading the development and implementation procedures for conducting on-site reviews of HECM servicers.

In terms of the recommendation aimed at creating an information-sharing agreement between FHA and the CFPB, such an agreement currently does not exist between the two agencies. FHA and CFPB “generally agreed” with the proposed recommendations, according to GAO.

GAO additionally recommends that FHA collect and record consumer complaints in order to analyze the frequency of specific grievances that are raised, while also periodically analyzing consumer complaint information about reverse mortgages to, “inform management and oversight of the HECM program,” the report reads.

Likelihood of implementation

Of particular importance to GAO is the review of, and reporting on, HECM program performance indicators, says Alicia Puente Cackley, director of financial markets and community investment at GAO and a co-author of the report. Cackley also served as a witness offering testimony based on the GAO report in last week’s hearing of the House Financial Services Subcommittee.

“While we believe all our recommendations are important for FHA to address, the recommendation on establishing, reviewing and reporting on performance indicators is especially important because it will provide FHA and Congress with information they need to oversee and make decisions about the program,” Cackley tells RMD in an email.

The feasibility of implementing these recommendations was also positively received by FHA, making the likelihood of actual implementation higher, Cackley says.

“GAO always considers the feasibility of implementing any recommendations we make,” Cackley tells RMD. “ With respect to the reporting tools we recommended that FHA develop and implement, not only did the agency agree with the recommendation, but it has previously developed similar tools for its forward mortgage portfolio.”

The GAO’s recommendations also have support from key representatives in Congress who are currently working on drafting new legislation related to the HECM program. Rep. Denny Heck, the primary sponsor of the “Preventing Foreclosures on Seniors Act of 2019,” told Cackley in last week’s hearing that he was working to incorporate all of GAO’s recommendations into a new draft of the bill.

“I hope you’ll be pleased to know that virtually every one of the recommendations in the GAO report I will incorporate into the next draft,” Rep. Heck told Cackley during the hearing. “And, we are in the process of that as we sit.”

Cackley lauded Heck’s support for the recommended changes.

“It is always encouraging when Congress uses our reports to improve the performance and oversight of federal programs,” Cackley tells RMD. “Our recommendations highlight some key areas where FHA can improve its oversight of the HECM program.”

What reverse mortgage industry players should know

FHA will need to engage with industry stakeholders at multiple levels to ensure that any implementation of GAO’s proposals are efficiently carried out, which is something that those within the reverse mortgage industry should keep in mind, Cackley said.

“To implement some of our recommendations – especially with respect to data quality and completeness – FHA will need to engage with HECM servicers and potentially other industry stakeholders in order to assure effective and consistent implementation of any new requirements,” Cackley says.

Read the full report at GAO.