Today’s existing home sales report was a massive beat, similar to what happened last year in this month. Will this mark the high point for sales this year like it did in 2023? Unless mortgage rates go lower, that’s what we should expect, because that’s what happened last year.

When mortgage rates headed lower at the end of 2022 into 2023, we had 12 weeks of positive weekly purchase application data. That filtered itself into one massive report in March. This year, we’ve had eight positive purchase application reports and the sales were spread out over two months — last month and this month. The purchase application data has weakened as mortgage rates headed higher earlier in the year. So, unless rates go down, this might be the high in sales in 2024. Below is a chart of some of the data lines from the report.

From the National Association of Realtors: Total existing-home sales– completed transactions that include single-family homes, townhomes, condominiums and co-ops – bounced 9.5% from January to a seasonally adjusted annual rate of 4.38 million in February. Year-over-year, sales slid 3.3% (down from 4.53 million in February 2023).

The last existing home sales report didn’t have a big bounce, so I suspected we would have some spillover demand in this month’s report. We have moved from 3.85 million to 4.38 million in two reports. For an average year, that would be a big move if we ended the year today. However, like last year, we were just riding the wave of better purchase application data. This is why we created the housing market tracker articles to keep everyone versed in forward-looking demand and the forward-looking demand was getting better as mortgage rates fell from 8% to below 7%.

From NAR: Year-over-year, sales slid 3.3% (down from 4.53 million in February 2023).

The year-over-year comps were tough this month; for most of the year, we would have been positive year over year. However, last month’s report was the one significant gain in existing home sales, which explains why the data is still negative year over year. These comps will get easier as the year progresses. We will be laser-focused on tracking the purchase application data in relationship to the 10-year yield and mortgage rates going out the rest of the year

From NAR: Total housing inventory registered at the end of February was 1.07 million units, up 5.9% from January and 10.3% from one year ago (970,000).

Here is some perspective on the NAR active inventory data:

- Since 1982, traditional normal inventory levels range between 2 million and 2.5 million.

- In 2007, they were 4 million.

- Today, they are 1,070,000.

- The monthly supply now stands at 2.9 months.

As you can see, we are far from average. With the NAR data, I would be throwing a party if inventory could just get into a range of 1.52-1.93 million. So, it’s heading in the right direction, just very slowly.

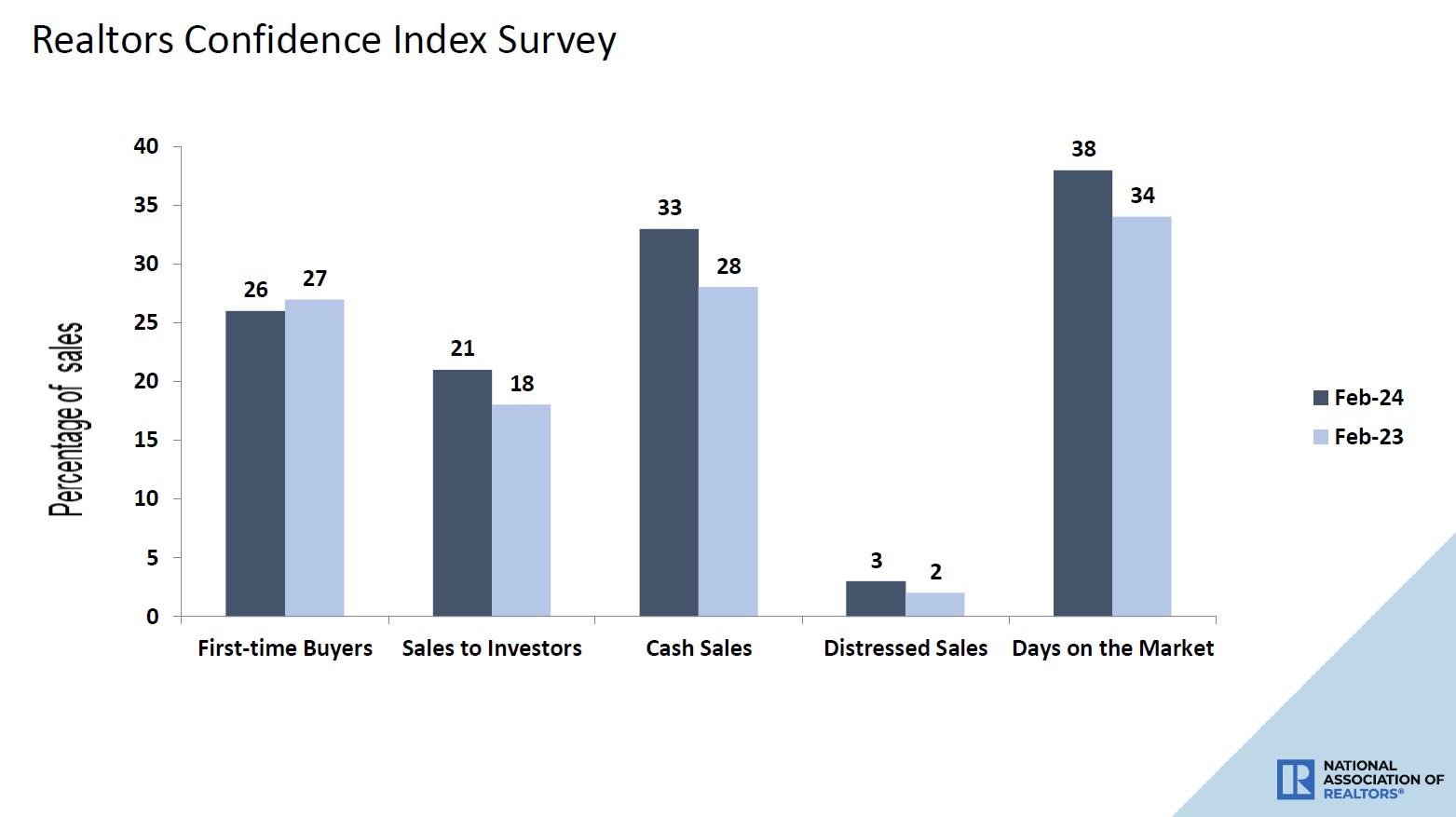

From NAR: First-time buyers were responsible for 26% of sales in February; Individual investors purchased 21% of homes; All-cash sales accounted for 33% of transactions; Distressed sales represented 3% of sales; Properties typically remained on the market for 38 days.

What I love about this data is that the days on the market are over 30 days. My entire savagely unhealthy housing market theme was about the days on the market being a teenager, which means too many people chasing too few homes. Today, we are over 30 days old, which is good. This data line is very seasonal, so it will take its seasonal fall and increase later in the year. However, over 30 days on market brings a smile to my face.

We had a big beat in existing home sales today, but can it last? History says with lower mortgage rates, yes! We don’t need tax credits to get demand going, but we need lower mortgage rates.

It’s a shame that we have such a restrictive housing policy today because our demographics are massive for ages 30-39! As you can see, just one big mortgage rate move lower, and demand comes out. As I have stressed time and time again, we are working from the lowest sales ever, it doesn’t take much to move the needle.

Appreciate your insight as always.