Early in 2021, when I was talking about how people should worry about home prices overheating, I had a glimmer of hope that maybe toward the end of 2021 we would be spared another seasonal collapse of inventory. Inventory always falls in the fall and winter, but I hoped it wouldn’t be a repeat of 2020.

Unfortunately, that didn’t happen and recent data shows that we are at fresh new all-time lows in housing inventory, with mortgage rates and the unemployment rate both under 4% currently.

Houston, we have a problem.

I have always been mindful that the years 2020-2024 have the potential for unhealthy home-price growth, but now that we are entering year three of this unique five-year period, it’s time to see when mother economics will give us clues about when this madness with meager inventory will end. We are in the middle of January 2022 and spring selling season isn’t too far away. I don’t believe any of us want 2023 to start off with new fresh all-time lows in inventory.

Mortgage demand needs to slow down

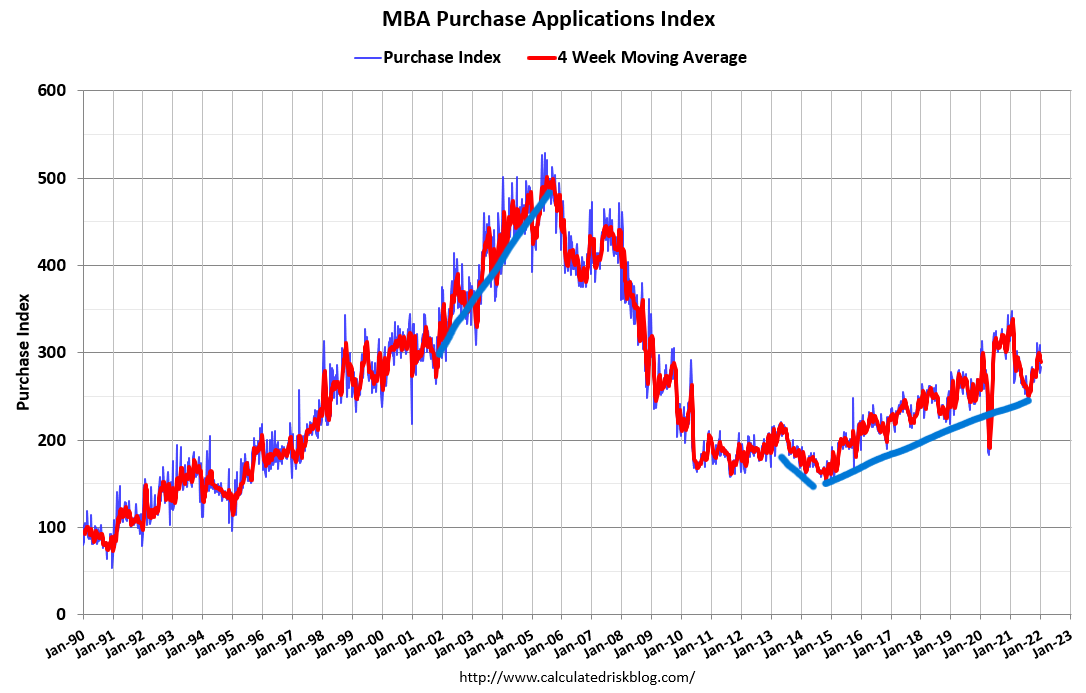

A big theme of my work here at HousingWire has been to show you that since 2014 purchase application data has been rising just as total inventory has been slowly moving lower. Demand is growing and stable, excluding the COVID-19 pause. Unfortunately, we need to see weakness in demand for inventory to rise and get into a range that I am 100% rooting for, between 1.52- 1.93 million. This level, while historically still low, will mean the days on market will go higher, and this will give people choices.

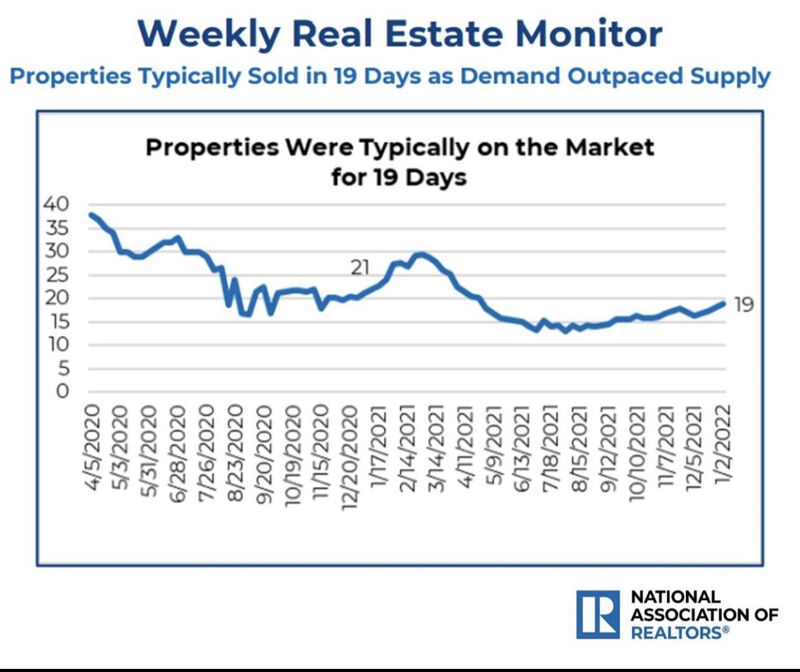

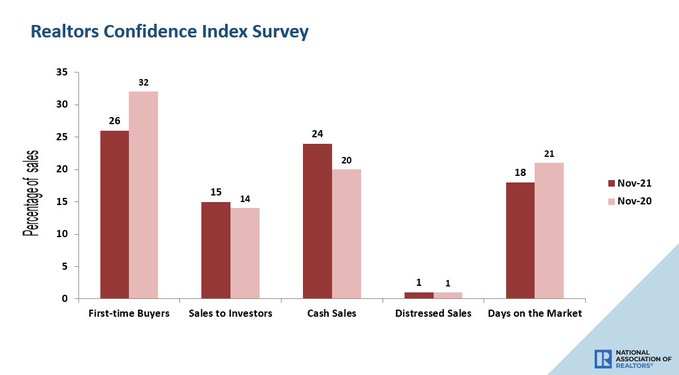

Here are two charts from the National Association of Realtors that will show that homes simply come off the market too fast to give housing a breather.

This data comes from the recent existing home sales report which has been outperforming lately.

The best way to track whether mortgage demand is slowing down is to look at the MBA mortgage purchase application data from the second week of January to the first week of May. Typically, this data line falls in volume past May, so February to April are the real key months to focus on.

For some perspective, you really only want to look at the year-over-year data with this data line and also realize that we are still dealing with COVID-19 comps until mid-February: after that, we should be fine on a year-over-year basis. For example, today, purchase application data is down 17% year over year and has been showing negative year-over-year trends since the middle of 2021. However, once you make COVID-19 adjustments, the demand was stable in 2021 and picked up toward the end of the year.

My 2022 existing home sales range is lower than what we are currently trending at: I am looking for a sale range between 5.74 million and 6.16 million.

If housing is really getting softer, you will see year-over-year declines of 15%-30% in this data line. We had this happen only two times in the past eight years excluding the recent data that need COVID-19 adjustments.

In 2014, purchase application data on-trend was down 20% year over year because rates had spiked up higher in the second half of 2013. We saw softness in housing toward the second half of 2013 as well. Total inventory levels rose in 2014 and adjusting to population, that was the lowest level in MBA purchase application data ever. Still, with that slowdown in demand, monthly supply never broke above six months. However, the rate of price growth cooled down and days on market grew.

Higher rates created balance in the marketplace in 2013-2014 and also in 2018-2019. While I do believe the rate of growth of home prices are cooling, it’s still well above my comfort zone for the years 2020-2024. I don’t want it to seem like I am rooting against housing, I just would like to see more balance in the marketplace. There is a reason I was warning about home price growth with inventory and mortgage rates low amid stable demand.

In 2020, for about six weeks purchase application data took a dive as Americans were pausing due to the first experience of COVID-19. Back then people took their homes off the market so the inventory data didn’t move too much higher outside a brief increase as people realized the world wasn’t ending. We had purchase application data down over 30% year over year, which took sales down as buying paused. However, sales shot right back up higher, quickly.

So, for 2022, you want to keep an eye on the year-over-year data, especially past mid-February toward April. If you see year-over-year declines in the data, then the days on market should grow. I am not talking about 5% – 8% year-over-year declines, I am talking more like 15%-30% year-over-year declines after COVID-19 adjustments are made. When it really matters, this data line will show you double-digit percentage moves both positive and negative. If you’re looking for balance like I am, this is where you want to look. This data line looks out 30-90 days as well, so you get the picture: the critical time for this data line is coming up in 2022.

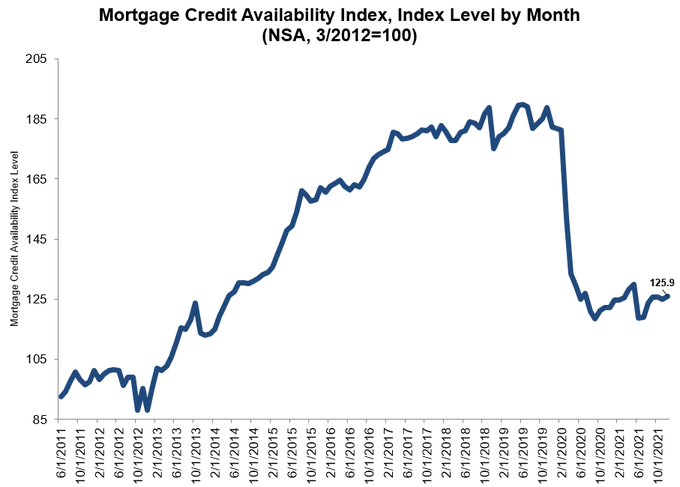

Don’t spend too much time on mortgage credit getting looser or tighter

One area that you don’t need to focus too much on is mortgage credit availability. I know many housing bears had hoped that credit getting tighter in 2020 and 2021 would crash the housing market. However, credit is very liberal today, as it always has been. However, since we’ve had no exotic loan debt structure post-2010, credit looking tight on paper just doesn’t have the same impact as it did from 2005-2009. At that time sales were declining from a high level and credit was getting very tight from the standards that facilitated the demand from 2002-2005.

From the chart below, it looks like credit got very tight from the start of COVID-19 and not much has been happening after that. In reality, most loans in America were basic vanilla 30-year fixed loans, and credit flowed for the most part during the COVID-19 crisis and recovery, all the way from 2021 to 2022. So if credit availability grows or declines, it’s only on the marginal loan products that are being used to buy primary residence homes. This isn’t like the peak of the housing bubble where 35% of the loans that were being done were ARM products. That number is below 5% now, so you don’t need to worry about the 30-year fixed loan being shut down. Or you don’t need to concern yourself that exotic loan debt products are coming back into the system pushing credit availability up

From the MBA:

Lastly, it falls back on the bond market

As you can probably tell from my writing, I believe and love a balanced housing market. What we have currently isn’t a balanced market. I really didn’t need to worry about this from 2008-2019, because I never believed we had the demographic demand to push total sales over 6.2 million to drive inventory levels to such low levels.

Well, that isn’t the case in the years 2020-2024, hence why I have always separated these two periods: from 2008-2019 and then from 2020-2024. With that said, in the past, higher mortgage rates, while never crashing the existing home sales market, have been able to cool things down and create more days on the market. The only problem is that this will require the 10-year yield to break over 1.94% and keep rising with some duration. This obviously hasn’t happened and this hasn’t been part of my forecast in 2021 or 2022. You can see why I am concerned.

Even with the hottest economic growth in decades, smoking hot inflation data — like we saw in the CPI report today — and all the talk about the Fed rate hike and taper, the 10-year yield currently right now is at 1.72%. Don’t forget, with the bond market, the trend is your friend, as I talked about in a recent article on jobs data.

What we know today is that we are starting 2022 spring at fresh new all-time lows in inventory for single family homes. Mike Simonsen, a friend from Altos Research creates weekly charts on the meager supply of inventory.

Here in Southern California, the amount of inventory in Los Angeles County is 4,432 homes, in Orange County it’s 954, and In San Diego it’s 1,254. Think about the millions of people who live in these areas and we are looking to start the year at 6,640 homes for sale.

Now, seasonality works both way. Inventory will pick up in the spring and summer and fade in fall and winter. However, as you can see, we are far from levels I would consider to be balanced, where days on market grow and people have choices. Since we are in year three of my five-year unique housing demographic period, demand being stable means getting the velocity of inventory to rise in a big way is difficult. The only way we can get some relief is if mortgage demand fades because that is the primary driver of housing demand. As we all know, the forbearance crash bros failed dramatically in 2021.

I would keep a close eye on mortgage demand, especially from mid February to April, to gauge whether mortgage demand is fading, which would allow days on market to grow. If this doesn’t happen, we are going to have another year of unhealthy home-price growth. Mother economics, she is a serial killer and will leave clues on what the economy is doing — the trick is always looking in the right spot. Remember, always be the detective, not the troll.