The housing market faced some serious obstacles last week as the 10-year yield broke over 4%, mortgage rates rose to over 7%, purchase apps fell again and we are still trying to find the elusive seasonal bottom for housing inventory.

Here is a quick rundown of the last week:

- Purchase application data was down 6% weekly.

- Weekly inventory fell much more than the previous two weeks, down 11,021; new listing growth had its lowest weekly calendar print for this previous week.

- The 10-year yield attempted to reach my peak forecast level for 2023 but failed to stay above 4%; we had over 7% mortgage rates for a day.

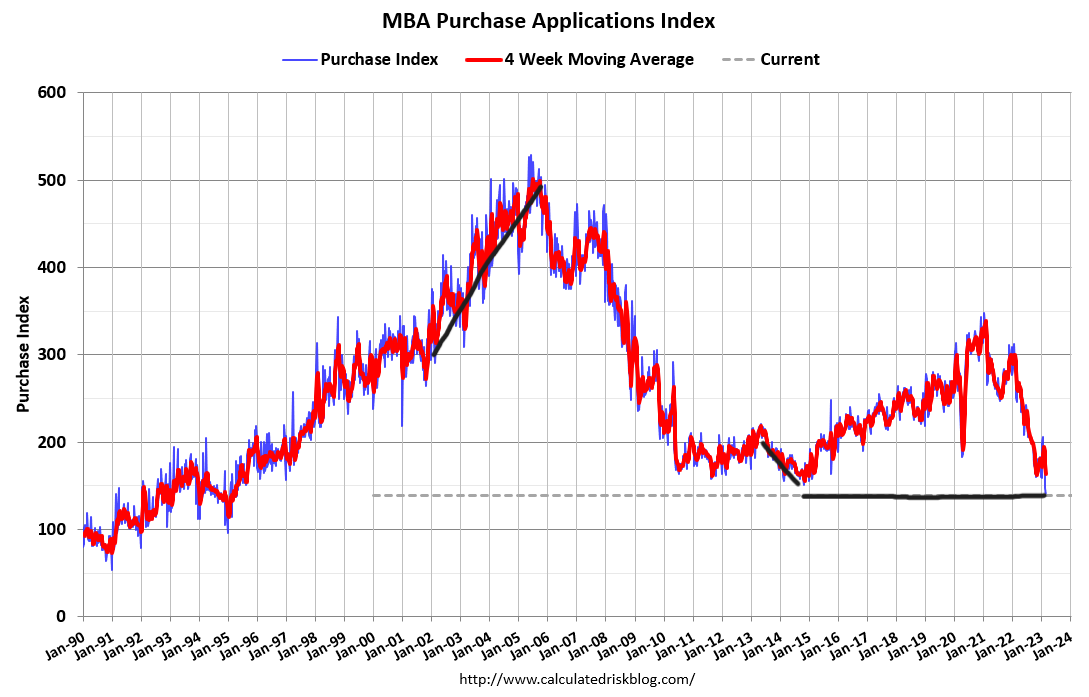

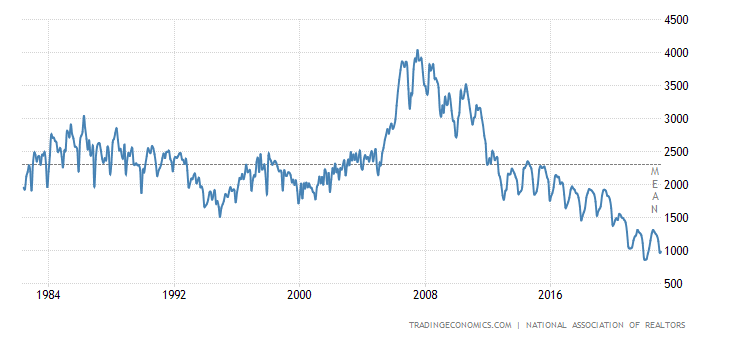

Purchase application data

Keep it simple here, folks; once rates started to rise so quickly, they zapped the purchase application data so we’ve now had three weeks of a negative trend. We did have a good run in purchase apps from Nov. 9, 2022, until February and we can see how that is playing out in home sales.

However, the trend has turned and the mother of all low bars just got lower, as the last time purchase application data was this low was in 1995, when Gangsta’s Paradise was the No. 1 song of the year. The chart below is a great illustration of where we are.

Purchase apps look out for 30-90 days, so it will be some time before this hits the home sales data. When mortgage rates fall again and we see an increase in this data line, we need to remind ourselves that we’re working from an extremely low bar.

The seasonality of this data line is typically the second week of January to the first week of May. After May, traditionally speaking, volumes always fall, so we have about three more months here before the seasonal decline, which will be very interesting to watch since we are already at 1995 levels today.

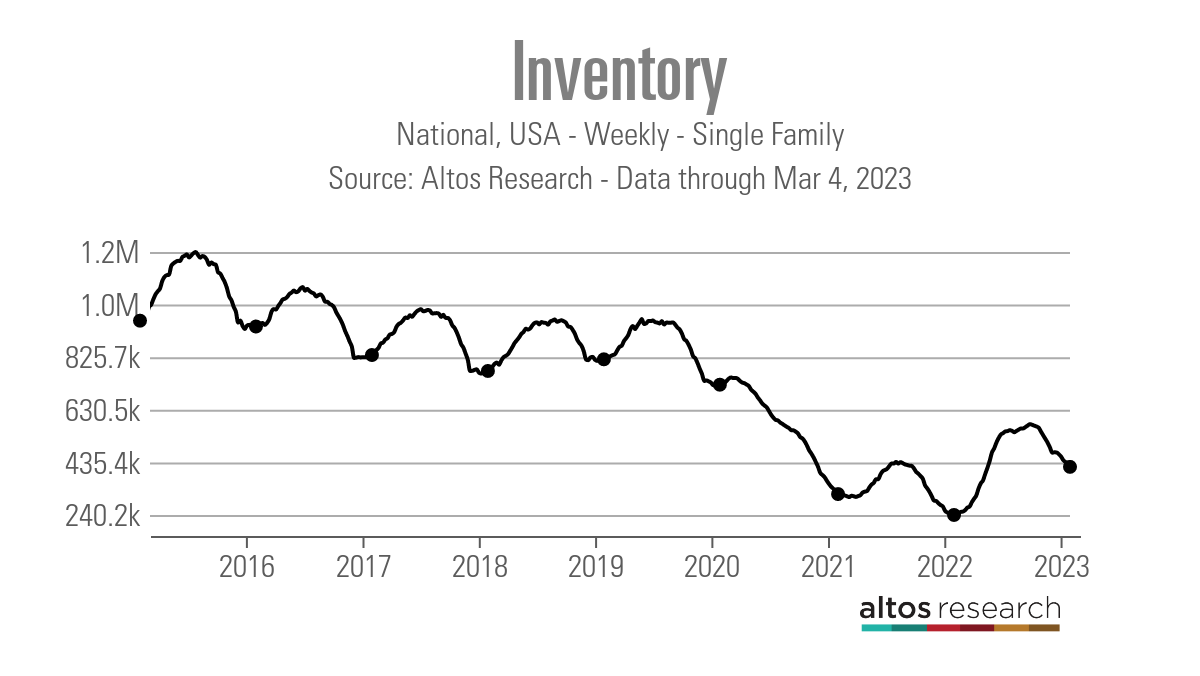

Weekly housing inventory

We still haven’t hit the elusive bottom for seasonal inventory, which traditionally happens in January. Instead, we are now going into the third year in a row when it bottoms out in March or beyond.

According to Altos Research data, housing Inventory fell by 11,021 over the last week, which is noticeably more than we saw the previous week, meaning the downtrend is picking up steam instead of slowing down as we head into March.

Hopefully, this is just a by-product of the three months of positive purchase application data from November to February. (I discussed my theory on why inventory bottoms out later in the year on this HousingWire Daily podcast.

However, inventory is still above where it was last year, so now we are waiting to see when the seasonal inventory increase will start to happen. We still aren’t back to pre-COVID-19 housing inventory levels, as shown below.

- Weekly inventory change (Feb. 24 – March 3): Fell from 429,757 to 418,736

- Same week last year: (Feb 25 – March 4): Fell from 243,916 to 240,194

Looking at last year, this week was when we found the bottom in seasonal inventory before the rise. However, last year the weekly decline was much less. We should be mindful that the seasonal inventory increase should happen shortly.

The new listing data had its lowest weekly print ever, down slightly from last year but more noticeably from what we traditionally saw in the previous decade. You can see the decline of new listing data below:

- 2021 51,975

- 2022 49,374

- 2023 49,363

Last year we did have some year-over-year growth in the weekly new listings data, as shown in the chart above, during May and June. However, that sharply reversed after June, and we haven’t seen any year-over-year growth in new listing since then.

However, new listings have been declining for years, no matter where mortgage rates have been trending since 2020. Just to give you more historical context to how low we are today, here is the data from previous years before COVID-19, and mind that in the last expansion, mortgage rates had a range between 3.25%-5%.

- 2015 77,189

- 2016 71,101

- 2017 61,205

- 2018 63,251

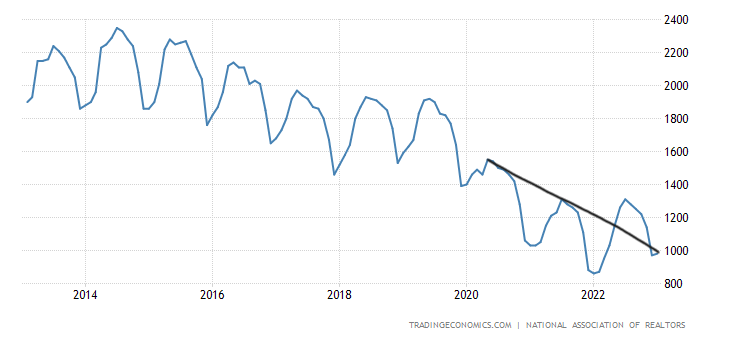

On a positive note for future inventory growth, per the last existing home sales report, the days on the market are over 30 days. I am a big believer that instead of listening to internet conspiracy theories about massive housing inventory increases for 11 years, there is a valid premise to be made that inventory can grow over time as days on market grow.

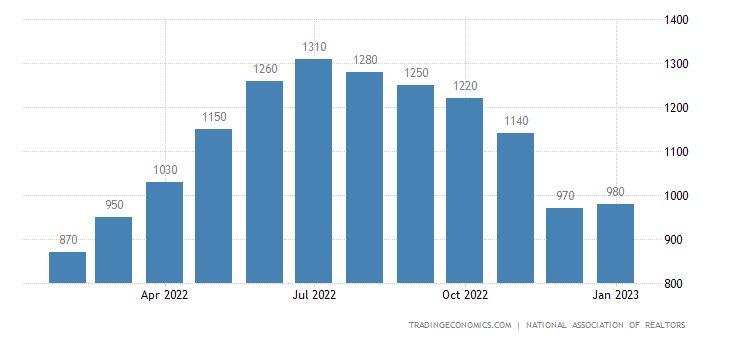

Using the NAR data, this was the premise of my forecast last year for housing inventory to break over 1.52 million in 2023. This is also a four-decade low in inventory before COVID-19. My 2023 inventory forecast needs a lot of help, as new listing data isn’t growing at all still. Per the last existing home sales report, we are at 980,000.

Here is a look at last year’s seasonal housing inventory increase using the NAR data. Even with the most significant monthly sales collapse in modern history for the existing home sales market, we never got within the 2019 range of 1.52- 1.93 million.

A longer-term historical look at the national inventory levels using the NAR numbers shows that 2 million to 2.5 million is the norm, as you can see below.

10-year yield and mortgage rates

In my 2023 forecast, I posited that if the economy stayed firm, the 10-year yield range should be between 3.21% and 4.25%, equating to mortgage rates of 5.75% to 7.25%.

Earlier this year, the bond market tried to make a break under 3.42% on the 10-year yield, which I believed would be hard to do with the firm economic data, as you can see in the black line I drew on the chart below. It has failed to break that level three times recently, and now it is testing a key level higher.

Last week we had a lot of action on the bond market just to end up exactly where we were the previous Friday. So, while we didn’t test my 4.25% peak level for 2023 on the 10-year yield, mortgage rates went all the way to 7.10% for a day before falling back to 6.97% on Friday.

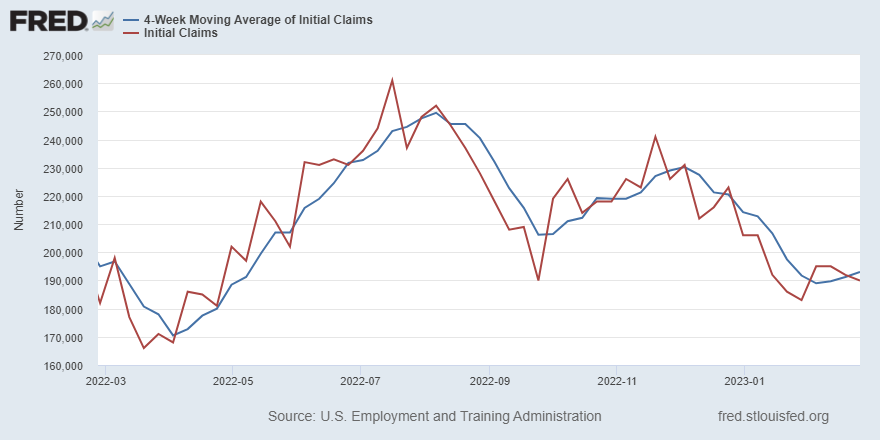

What can bring mortgage rates down, even below 5.75%? Per my 2023 forecast, the 10-year yield would have to go below 3.21% as a result of weakening economic data, especially in the labor market.

I don’t believe the Federal Reserve will pivot their rate strategy until jobless claims break over 323,000 on the four-week moving average. Once this crucial data line starts heading in that direction, the bond market will get ahead of the Fed and send the 10-year yield lower, meaning mortgage rates will also go down.

As you can see below, we are far from that level today, with the jobless claim data still below 200,000.

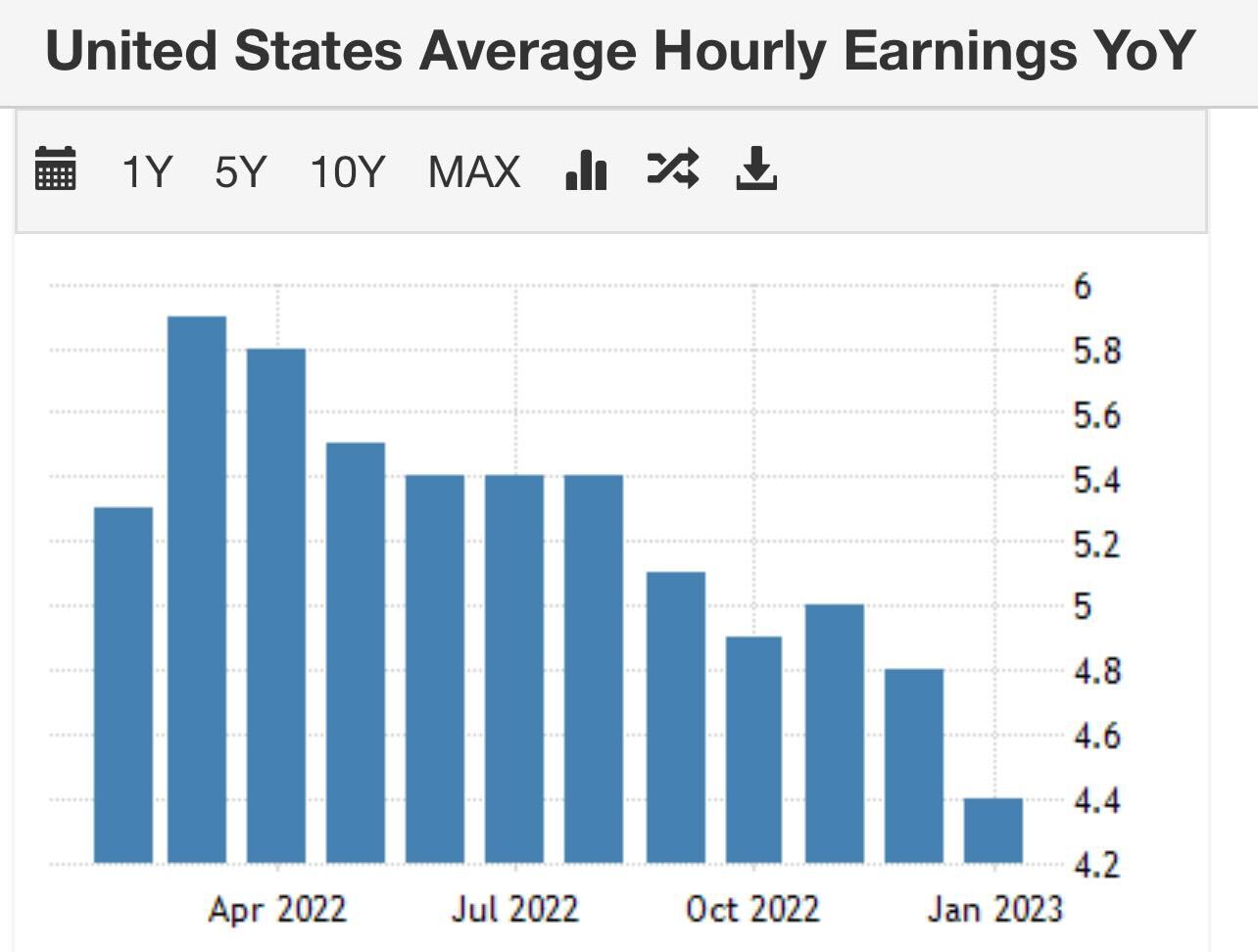

While we have seen a big swing in mortgage rates this year, it’s still in the range I was looking for while the economic and inflation data stays firm. Over time, the growth rate of inflation will cool off with the slowdown in rental inflation. This is one reason why the inflation we see now is so different from the 1970s.

The week ahead

We have some big things happening in housing market data this week! On Tuesday, Federal Reserve Chair Jerome Powell will present his semiannual Monetary Policy Report to Congress, which will no doubt feature some grand-standing from politicians.

Also, this week is jobs, jobs and more jobs, with a hat trick of employment data this week including job openings, jobless claims and the BLS jobs report on Friday.

The Federal Reserve wants job openings to fall, slowing wage growth. So the Fed wants jobless claims data to increase, meaning wage growth should slow down more.

As the only person on planet earth who was predicting job openings to 10 million during the COVID-19 labor recovery, I will revisit this subject following the jobs report on Friday. I will try to explain the confusion about the labor market to everyone, including some Fed members who might be reading this.

Buckle up for another crazy week in the U.S. housing market as we watch the 10-year yield and mortgage rates, purchase apps and housing inventory data.