On Thursday, the U.S. Census Bureau reported that housing permits came in at an excellent print at 1,899,000, surprising me. Then I took a look at housing completions at 1,246,000, and it reminded me of the sad state of the housing market. We have the demand — we just don’t have the supply.

Global pandemics have always created short-term shortages due to a lack of production capacity. However, the COVID-19 pandemic happened in the middle of the most enormous housing demographic patch ever recorded in our history. Then on top of all that, existing total inventory has broken to all-time lows. You can understand why I keep saying this is the unhealthiest housing market post-2010.

Housing starts, just like new home sales, can be wild month to month, so the trend is your friend and the direction in housing permits has been good enough to keep construction going.

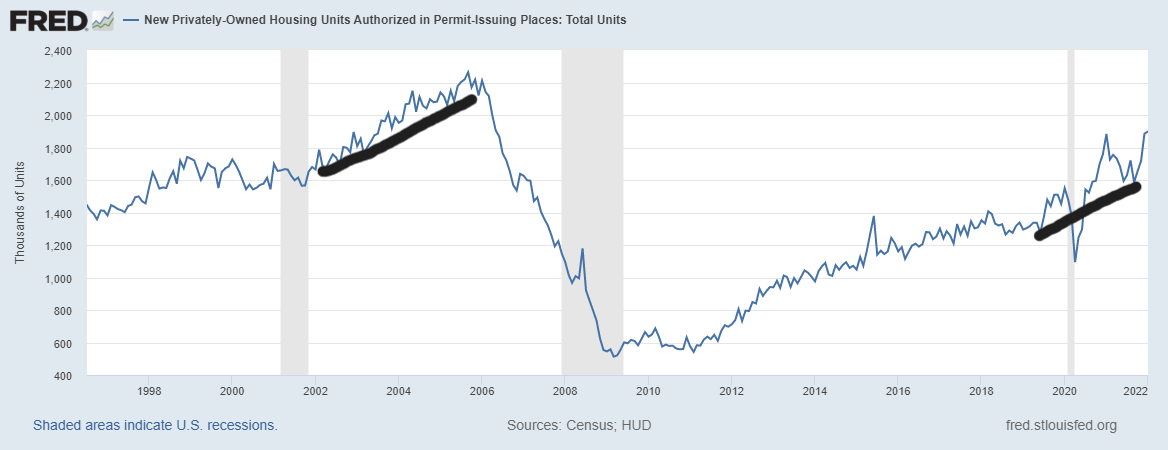

Housing permits

From Census: Privately-owned housing units authorized by building permits in January were at a seasonally adjusted annual rate of 1,899,000. This is 0.7 percent above the revised December rate of 1,885,000 and is 0.8 percent above the January 2021 rate of 1,883,000. Single-family authorizations in January were at a rate of 1,205,000; this is 6.8 percent above the revised December figure of 1,128,000. Authorizations of units in buildings with five units or more were at a rate of 629,000 in January.

As we can see below, as long as new home sales don’t fade, permits will keep this uptrend going. With rental inflation kicking into high gear, the need for multifamily construction will stay.

Since new home sales aren’t booming, we haven’t surpassed the housing bubble peak in total housing permits. We don’t have a massive credit boom happening in housing and the builders don’t oversupply a marketplace, so the trend of slow and steady keeps on moving.

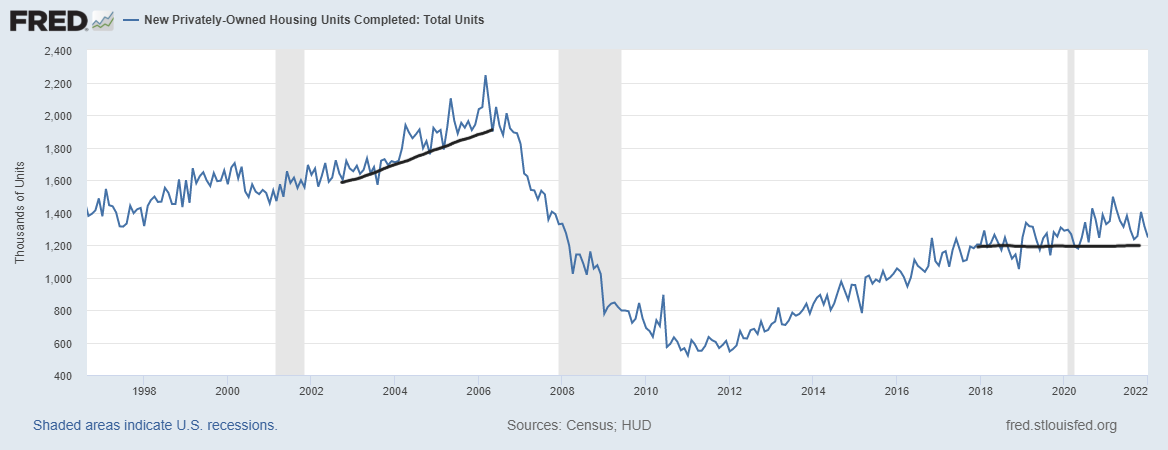

Housing completions

From Census: Privately‐owned housing completions in January were at a seasonally adjusted annual rate of 1,246,000. This is 5.2 percent (±8.0 percent)* below the revised December estimate of 1,315,000 and is 6.2 percent (±10.0 percent)* below the January 2021 rate of 1,328,000. Single‐family housing completions in January were at a rate of 927,000; this is 7.3 percent (±6.8 percent) below the revised December rate of 1,000,000. The January rate for units in buildings with five units or more was 309,000.

This is heartbreaking to see, but the housing completion data shows how stressed the new home sales market is when it comes to getting homes finished. Also, note the risk of cancellations can be an issue at a certain point for builders if mortgage rates keep rising higher. This has happened before but as of yet, it isn’t an issue.

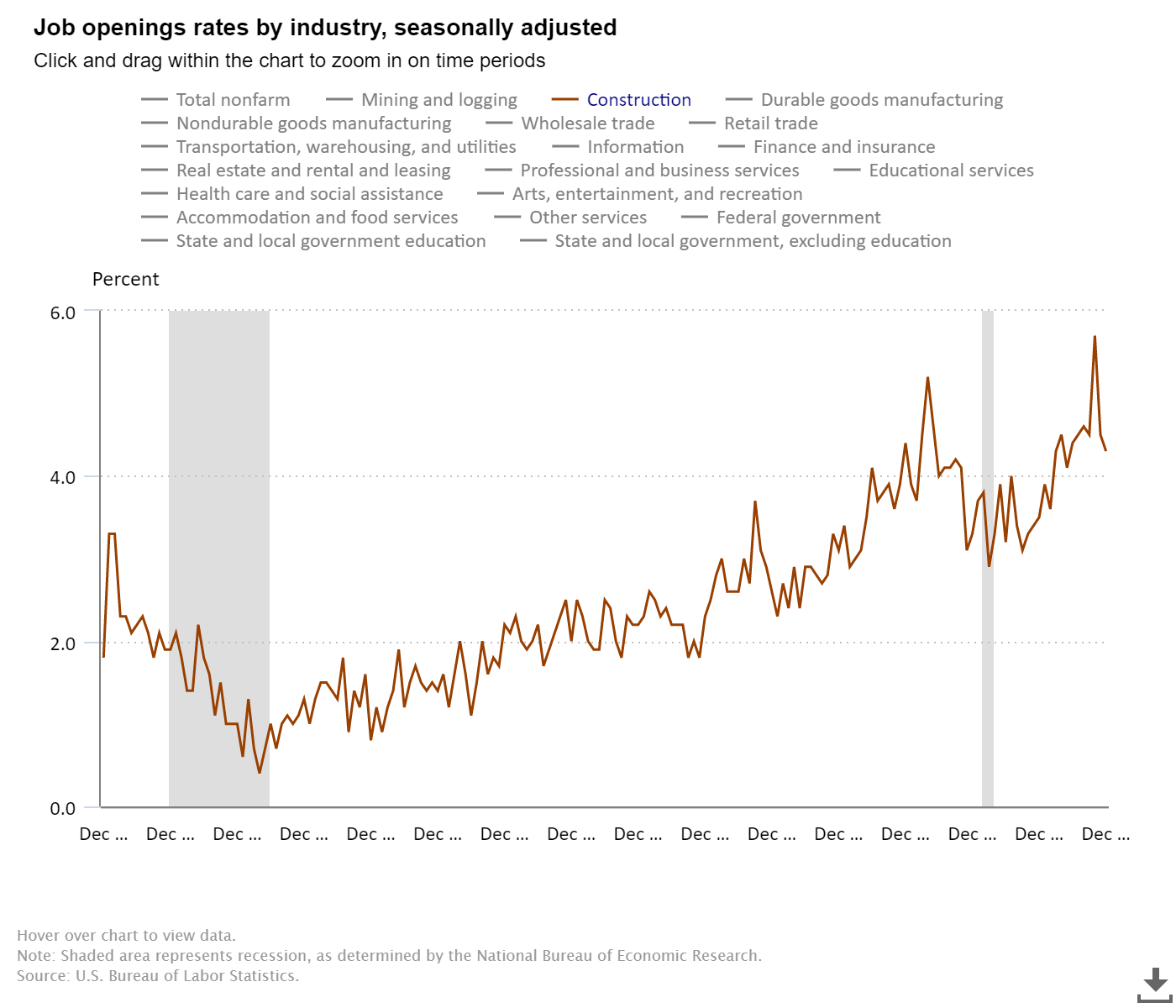

Regarding labor for housing construction, job openings are very high in the construction sector. We have nearly 11 million job openings in the U.S. and 330,000 of those are for construction workers, so the need for labor is real! Again, this is a first-world problem to have in America.

However, the lack of construction productivity has hampered us for decades. Where have all the great robots gone? Oh wait, we don’t have that in this sector. So, with that in mind, know the limits of what can be done with construction. As we all can see, it isn’t easy to finish a house amid supply shortages.

Housing starts

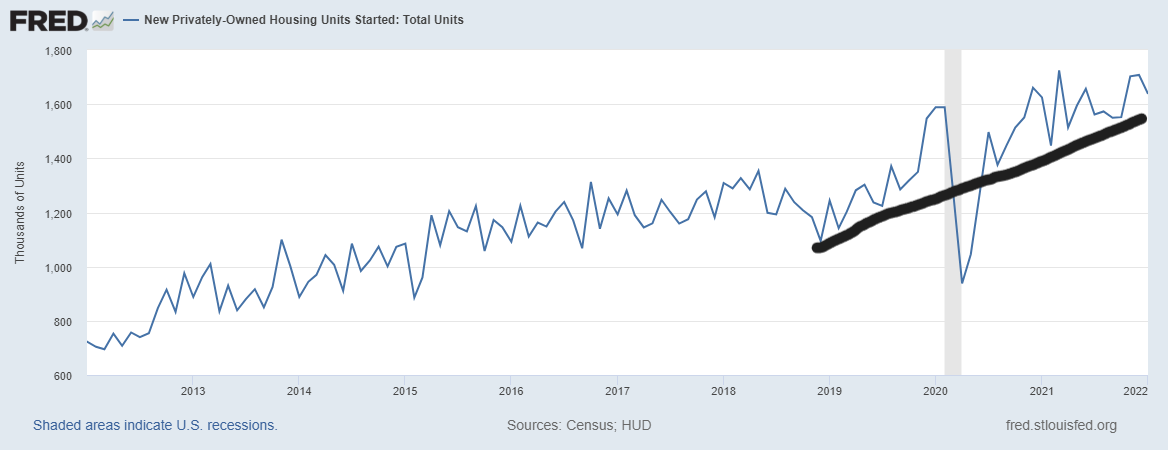

From Census: Privately-owned housing starts in January were at a seasonally adjusted annual rate of 1,638,000. This is 4.1 percent (±13.7 percent)* below the revised December estimate of 1,708,000, but is 0.8 percent (±12.5 percent)* above the January 2021 rate of 1,625,000. ingle-family housing starts in January were at a rate of 1,116,000; this is 5.6 percent (±12.0 percent)* below the revised December figure of 1,182,000. The January rate for units in buildings with five units or more was 510,000

Housing starts, like permits, are still showing a slow and steady climb. New home sales aren’t exactly booming, so the growth with single-family starts is still somewhat limited unless we get a faster increase in sales. In a rising mortgage rate environment, there is a risk that this sector will get hit. We had many years in the previous expansion where new home sales missed estimates, which can create housing starts to stall.

However, that was working from a shallow bar. We no longer have that low bar, so the builders are mindful of demand staying at these levels and growing.

The builder surveys haven’t been moving much in either direction recently. Even though they’re high historically, don’t put too much weight on that aspect. If we see a noticeable decline from the trend lower, the builders are telling us something is wrong. I have often seen people neglect the lower trend movement and use the bottom of the housing bubble crash as a reference point. I would never use the bottom of the housing bubble crash as a reference point, ever. Once the trend goes lower for a few months, something is wrong.

I believe the builders are mindful of higher rates and all the delays in finishing a home. Since COVID-19 did a number on a lot of economic data lines, the adjustments that we had to make in 2020 and 2021 are coming to an end, so weakness is weakness, and strength is strength.

From NAHB:

While the housing permits data is fantastic, and it came off a more substantial number last month, the housing completion story is a giant mess right now. We see housing inflation on both fronts in America — in home prices and rents — and inventory for both sectors is low, with a massive young population needing shelter. Anything we can do to create more supply will be welcomed in America because shelter inflation matters, and it isn’t just a home-price story anymore.

We shall see if higher rates impact the new home sales sector. So far, purchase application data has been stable this year, and starting next week, we don’t have any more COVID-19 comps to make adjustments to.

Until then, buckle up — this year looks like a crazy year and my job is to try to make sense of all the madness we are dealing with in the housing market and the U.S. economy.