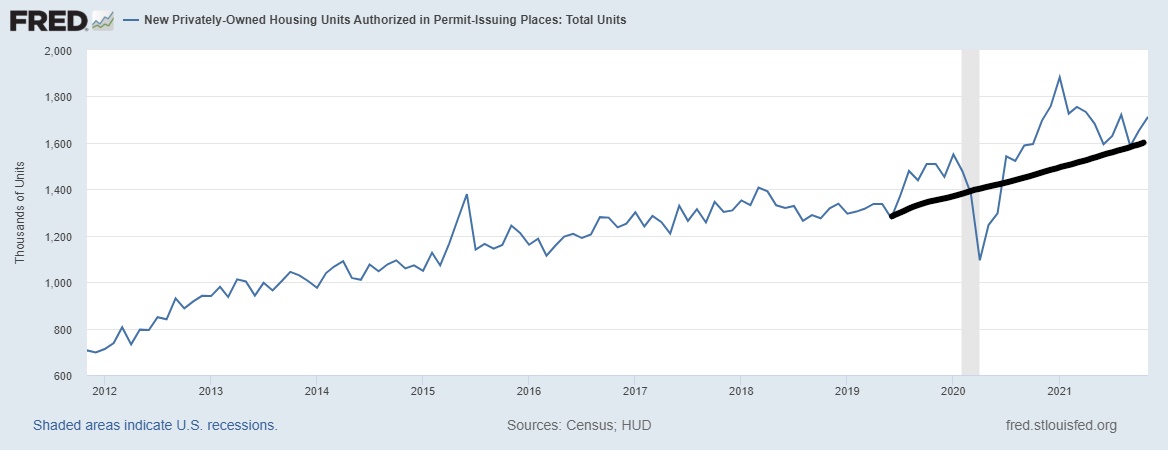

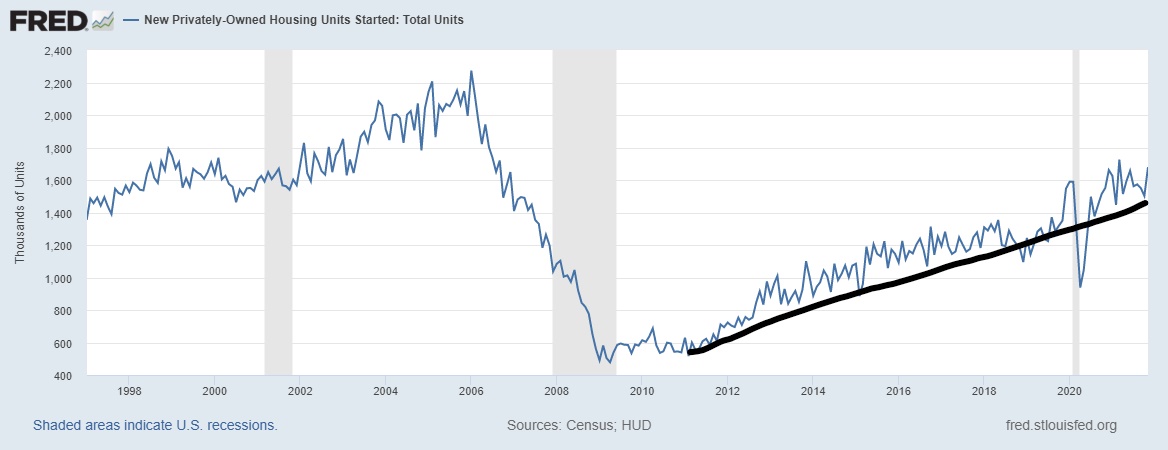

Today, the U.S. Census Bureau reported that housing starts came in as a beat at 1,679,000 for November. The more critical number of housing permits came in 1,712,000, a solid uptick from last month, and we saw slightly positive revisions to previous numbers.

Housing starts data has been choppy lately, as we are all aware of the delays in building homes in America. However, with all that said, the critical indicators for all housing data were consistently positive in 2021. If you knew where to look and expected a moderation from the COVID-19 surge in make-up demand, you would have prevented yourself from the embarrassment of being a housing crash bear in 2021.

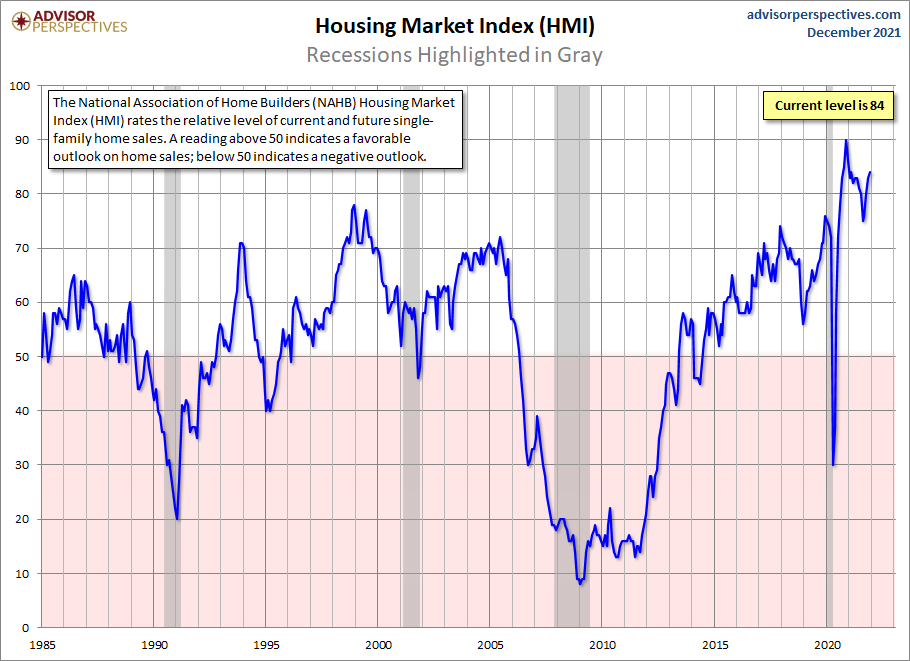

The builder’s confidence data had been rising for months now. At the same time, some people focused their attention on iBuyers, who don’t even account for 1% of total home sales in America. Rookies are always going to roll badly, as rookies do.

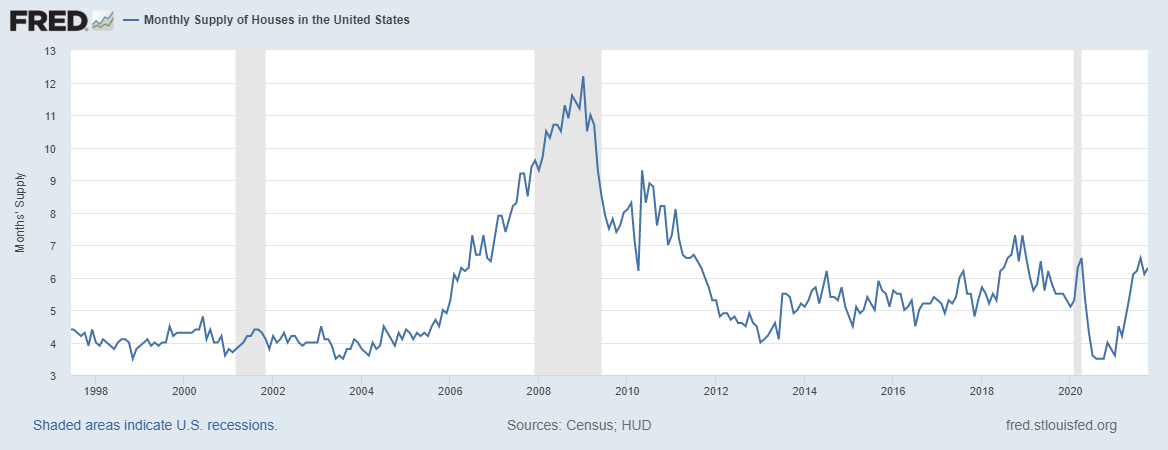

While new home sales aren’t booming in 2021, demand is still good enough to build more homes as the monthly supply of new homes is still below 6.5 months on a three-month average.

Building permits from from Census: Privately‐owned housing units authorized by building permits in November were at a seasonally adjusted annual rate of 1,712,000. This is 3.6 percent (±0.9 percent) above the revised October rate of 1,653,000 and is 0.9 percent (±2.0 percent)* above the November 2020 rate of 1,696,000. Single‐family authorizations in November were at a rate of 1,103,000; this is 2.7 percent (±1.1 percent) above the revised October figure of 1,074,000. Authorizations of units in buildings with five units or more were at a rate of 560,000 in November.

As we can see below, housing permits are not overheating like we saw in the last few years during the housing bubble years where mortgage credit was facilitated by exotic loan debt structures. Now, we have all legit high-quality homebuyers who are buying a home to live in with fixed low debt cost and rising wages.

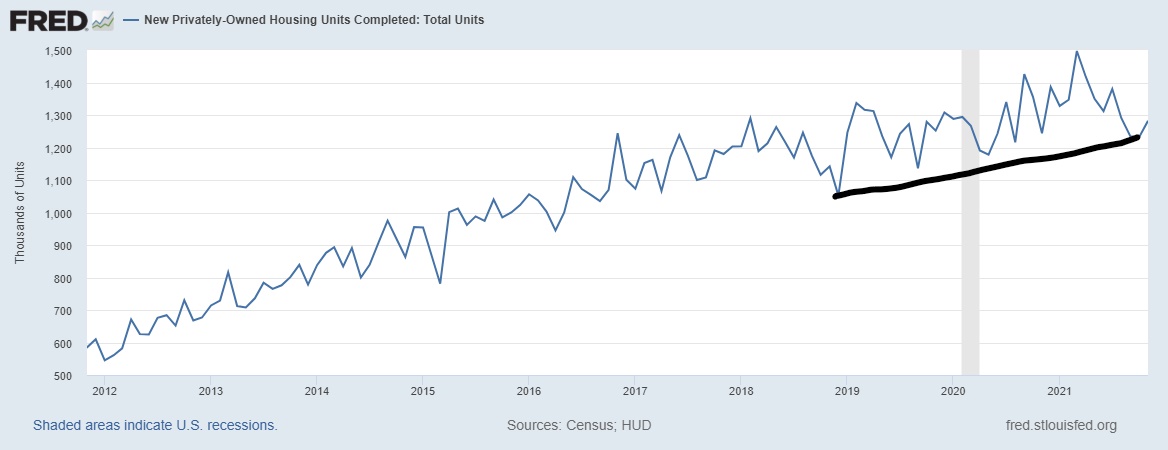

Housing completion data — which I call the Grundy of economics after my tortoise — is slow. We are all aware of the delays due to supply shortages, but this data line has legs to move higher over time slowly.

Housing completions from Census: Privately‐owned housing completions in November were at a seasonally adjusted annual rate of 1,282,000. This is 4.1 percent (±13.5 percent)* above the revised October estimate of 1,231,000 and is 3.1 percent (±13.6 percent)* above the November 2020 rate of 1,244,000. Single‐family housing completions in November were at a rate of 910,000; this is 0.1 percent (±12.0 percent)* below the revised October rate of 911,000. The November rate for units in buildings with five units or more was 364,000.

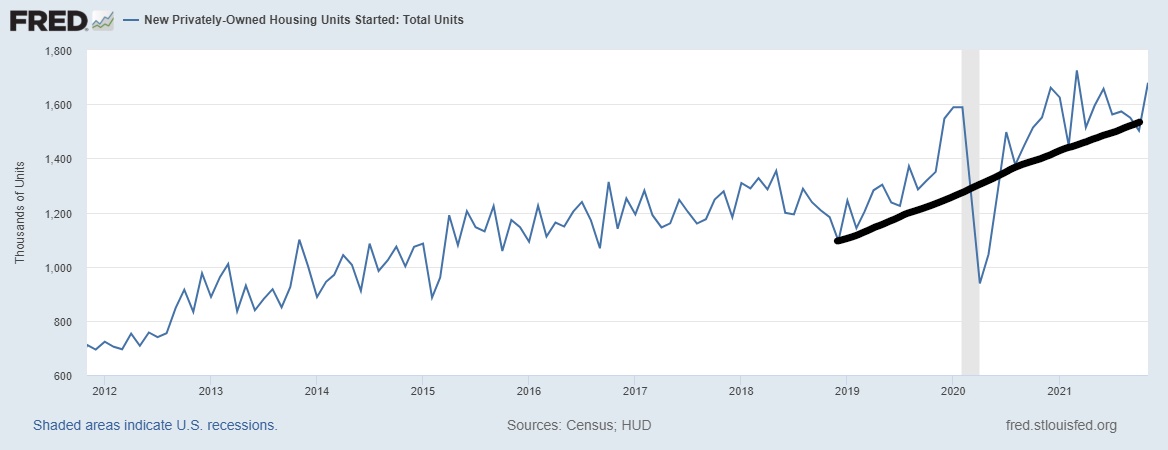

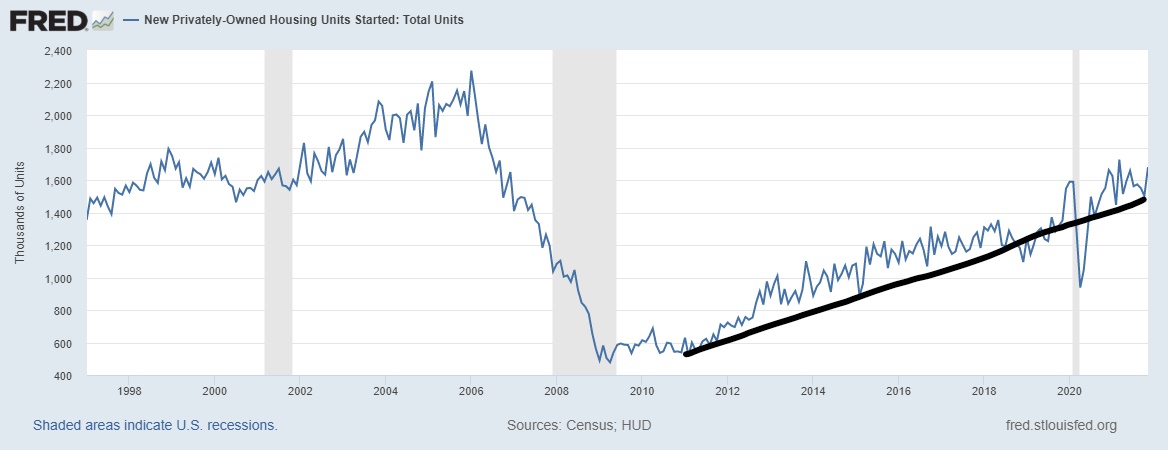

Housing starts data has been choppy for some of the reasons I stated above. However, since we are close to Christmas and 2022 is around the corner, I can finally retire one of my most extended economic calls in the previous expansion. From 2008-2019, my premise for housing was that we would see the weakest housing recovery ever and that housing starts wouldn’t start a year at 1.5 million or higher until 2020-2024, when demand finally warrants it. We are finally here on schedule, which means that the low bar that housing enjoyed from 2008-2019 is also gone.

Housing starts from Census: Privately‐owned housing starts in November were at a seasonally adjusted annual rate of 1,679,000. This is 11.8 percent (±15.2 percent)* above the revised October estimate of 1,502,000 and is 8.3 percent (±14.3 percent)* above the November 2020 rate of 1,551,000. Single‐family housing starts in November were at a rate of 1,173,000; this is 11.3 percent (±15.8 percent)* above the revised October figure of 1,054,000. The November rate for units in buildings with five units or more was 491,000.

Next up for housing starts would be the new home sales report coming out next week. The previous report came in as a miss of estimates and negative revisions. However, as I wrote last month, the builder’s confidence data for months were telling you a different story, and today you got to see why looking forward-looking indicators like confidence and housing permits is vital. Even with the new home sales report coming in as a miss last month, there was another story to tell.

My rule of thumb for housing has always been that if the monthly supply on a three-month average is below 6.5 months, the builders will keep building homes no matter the labor shortage complaints and cost of materials; they find a way to get paid. Still, even with the increases we saw in the monthly supply data this year, we never broke above 6.5 months on a three-month average. Slow and steady wins this race, and as long as you’re not looking for a massive construction boom, you won’t be walking in the wrong path.

Another new twist to the housing story is the comeback in lumber prices! Some of the crazier housing crash addicts in 2021 believed that lumber prices collapsing early in the year were forecasting the collapsing of housing. Like I have often said, the most untalented economic people we have in our country are all housing crash addicts, but as professional grifters, they’re fantastic. Think about being part of the lost decade from 2012-2021 and then going all-in on the crash thesis due to COVID-19, only to move the goal post to 2021 due to forbearance. And then to end up this Christmas as one of the more fraudulent bearish American groups of our generation.

They watched our country have this epic recovery starting from April 7, 2020, and now know that they were forever left behind in the dust as they couldn’t stop screaming that housing was going to crash. In any case, I bet those same people aren’t saying housing is recovering because of higher lumber prices; a troll has always to keep the grift going.

The rise in lumber prices isn’t positive it’s a negative, as all it does is make housing more expensive, but this is the world of commodity prices, and it can get wild from time to time. With all this said, housing starts are still pushing through as supply for new homes is still low enough to keep building going.

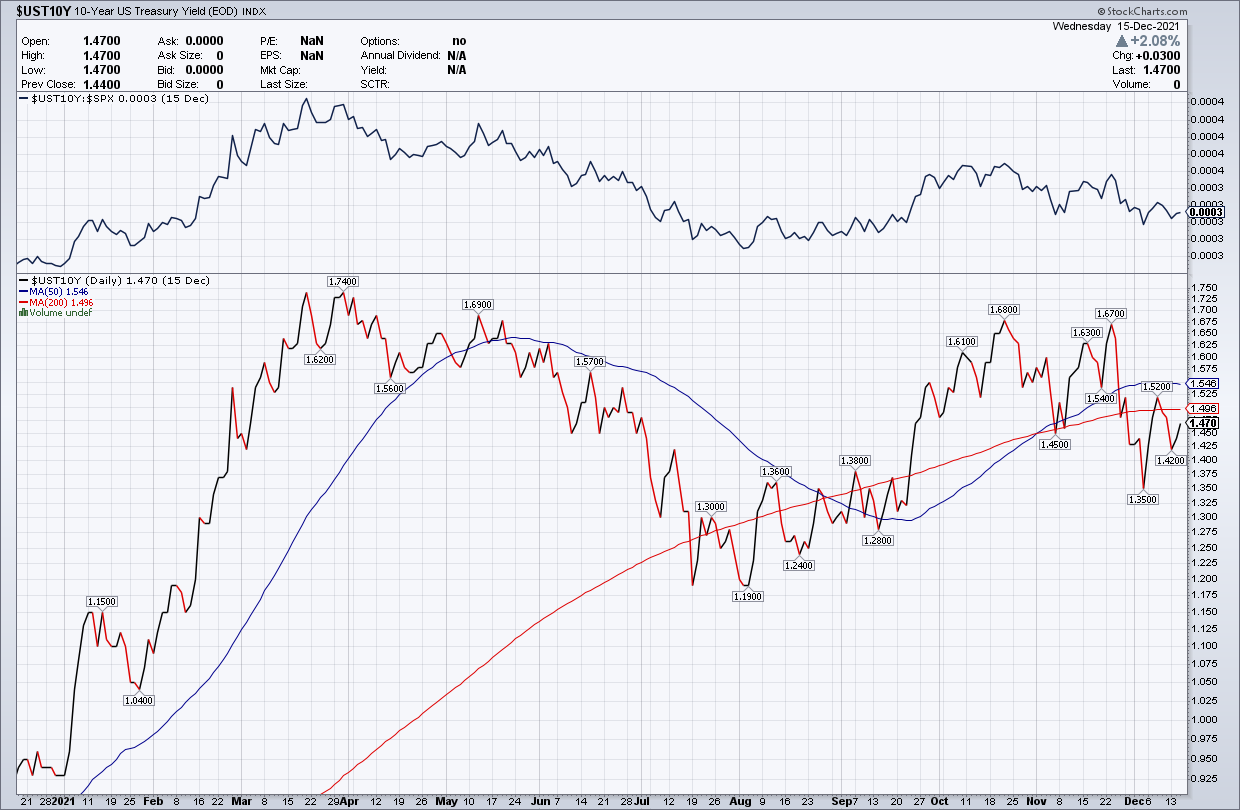

Mortgage rates impact this sector significantly, and I talked about how housing can cool down if the 10-year yield can break above 1.94%, which wasn’t part of my forecast in 2021. It is currently at 1.43% even with all the hot economic data, hotter than average inflation data, and the Fed tapering with rate hikes in play next year. The 10-year yield looks just right to me; as I have said going back to April 7, 2020, when the recovery is here, the 10-year yield should be in a range between 1.33%-1.60%.

Housing shouldn’t be a sexy boom-and-crash story because it’s a necessity. Housing is the cost of shelter to your capacity to own the debt; it’s not an investment. Sometimes just good old tedious economic modeling work gets the job done in telling the story. During the past two years, the lack of economic training and experience from anyone talking about an impending collapse in housing in 2020 and 2021 has shown us all the emperor has no clothes.

Housing starts are growing because demand is up and monthly supply is down; keeping things simple sometimes shuts down the improper noise. The builders’ confidence rising months ago and the fact that monthly supply never broke above my crucial level of 6.5 months was your clue that this sector is fine. On Monday I will be coming out with my 2022 forecast — expect lots of charts — which I will also discuss on the HousingWire Daily podcast, where you can find me every Monday morning.