Back in April when darkness was looking us straight in our eyes, I wrote this:

“These are dark times. But even in dark times, we are preternaturally prepared to see the light at the end of the tunnel. We learned in human physiology class that the photoreceptors of the human eye can detect a single photon of light. While it may not be until nine or more photons hit the retina that we perceived dawn, we see before we can perceive. Likewise, if we are diligent, we will be able to identify the return of hope and light coming back into the American economy before it is perceived by all those poor masked souls around us.”

Lead Analyst

In many ways, the era of COVID-19 in America shifted society into a dimension outside of traditional time. Birthdays, anniversaries, and major holidays slip by without family gatherings or restaurant celebrations. Days working from home trudge by like weeks while whole seasons pass almost unnoticed. Is Halloween really just around the corner?

The fiscal calendar, a mainstay of marking economic activity has served little purpose in COVID America. Where it once provided a structure by which to analyze balance sheets and economic trends, in these virus-directed times, it has become a vestigial anomaly like the little toe or the appendix of the human body.

In order to understand the economic performance of various sectors during these times, we need to abide by the dictates of the virus. For this reason, I divided 2020 into this economic-timeline into three phases: Before COVID (BC), After the onset of the Disease (AD), and America is Back (AB).

In a previous article, I wrote about five economic and/or social landmarks that we would need to pass in order to determine that we had exited the AD phase and entered the AB recovery phase. This serves as a report card on that recovery with a final word about the U.S. housing market.

On April 7, 2020 I wrote this for HousingWire and now you can see why the housing market has recovered, as most of these five variables have been met to a degree.

1. Flattened Curve

Status: Complete (with an asterisk)

“It is from this data that I have based my virus turnaround thesis, which is that by May 18 or sooner, we will see a flattening of the new infection curve, and by Sept. 1, we will be at a much higher capacity to fight this virus.“

By May 18 we had flattened the curve of new infections in most communities, which led to loosening or removal of stay-at-home restrictions. But this was done too soon and we got sloppy resulting in a resurgence of new cases. Keeping in line with my Sept. 1 date for progress, I needed to make a decision that I believe we could get this second surge under control.

Before the July 4th weekend I believed we could do this as a country if we worked together by Sept. 1st. I made sure to let everyone on twitter know that Sept. 1 is coming and the data should get better. Our government friends finally got on board with the promotion of mask wearing and containment policies in individual states. Currently the data has gotten better, but not perfect by any means.

It’s been a bumpy ride and it is not over yet. We will need to stay vigilant and united in following safety and containment measures in order to avoid another relapse into high infection rates. I’m checking this one off as complete but adding a big caution flag to indicate that we can easily undo our progress. Winter is coming, we are attempting to reopen schools so we do have some high velocity events that can increase cases fast. I still fall back to my core belief on what I said on April 7.

“I believe the months of April and May are going to tell an epic story of America’s start in defeating this virus. If we do this right and document the cause and effect of our efforts, future generations will be able to look to this period in time for how to handle a global pandemic.

“My faith in America winning has never let me down because I always believe in my people and country. I can tell you now, this virus isn’t changing my view on that. Before that reality is more common for a lot of Americans, bond yields will have headed higher while jobless claims and the St. Louis Financial Stress Index have already gone lower. Let’s all be here to see it.”

2. End of Stay-at-Home Orders

Status: Semi-complete

We never had a full-blown national stay-at-home policy with every state following it. Where restrictions were put in place, some have been lifted to a degree.

One aspect that we haven’t given enough attention to is that we were confused as a country during the first few weeks of the pandemic. We were hoarding toilet paper instead of making offers on homes that had no bidding war competition. This is totally understandable, it’s our first virus that we all had to deal with on a mass scale. The stock market was falling and we just weren’t sure how bad it was going to get.

Today it’s much different. Even when restrictions were put into place in certain states, we never saw the hoarding of toilet paper again, instead we are seeing multiple bids on homes now. We are starting to live and consume goods and services with an active virus in play. As a country, our purchasing habits have shifted to even more online shopping and home delivery. And this may be the new normal until we get a vaccine. If we mind our Ps and Qs for a bit longer, at least until a vaccine is released, we may not have to revisit the need for stay-at-home orders or limit certain business from operating.

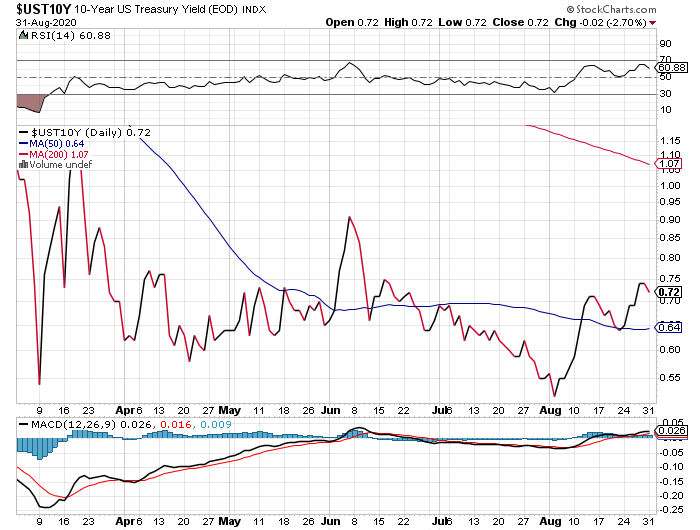

3. 10-Year Yield Goes Above 1%

Status: Incomplete

Before the 10-year yield broke under 1%, Bankrate.com published my forecast that 10-year yield during a recession would be in the range of -0.21% to 0.62%. The following Monday, March 9th bond yields dropped to a low of 0.33%. Currently the 10-year yield is at 0.72% on the morning of Sept. 1, 2020.

Since then, the 10-year yield has been above 0.62%. This tells me that the bond market believes the economy is going to get better. Having said that, yields haven’t broken above 1% yet. I expect some volatility in the markets in the next four months. When growth is slow and steady for two to three quarters, I expect yields to not only rise above 1% but stay in a range of 1.33% – 1.60% when real growth is stable.

While we can’t check off this landmark as “met,” note that the 10-year yield has been above 0.62% for most of this crisis. I know this 0.62% levels seems odd to some, but for me personally it was my biggest indicator that the bond market was telling me things are going to get better in the next few quarters.

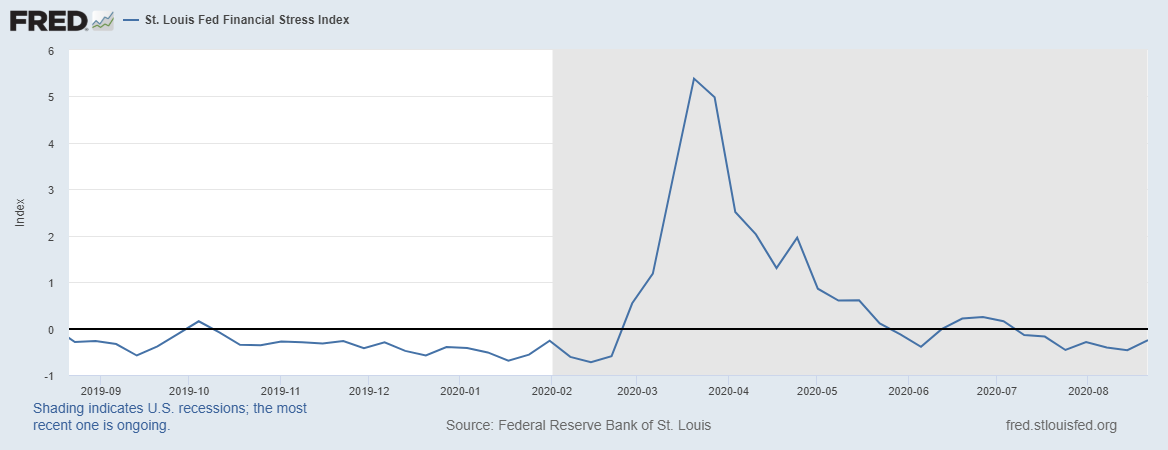

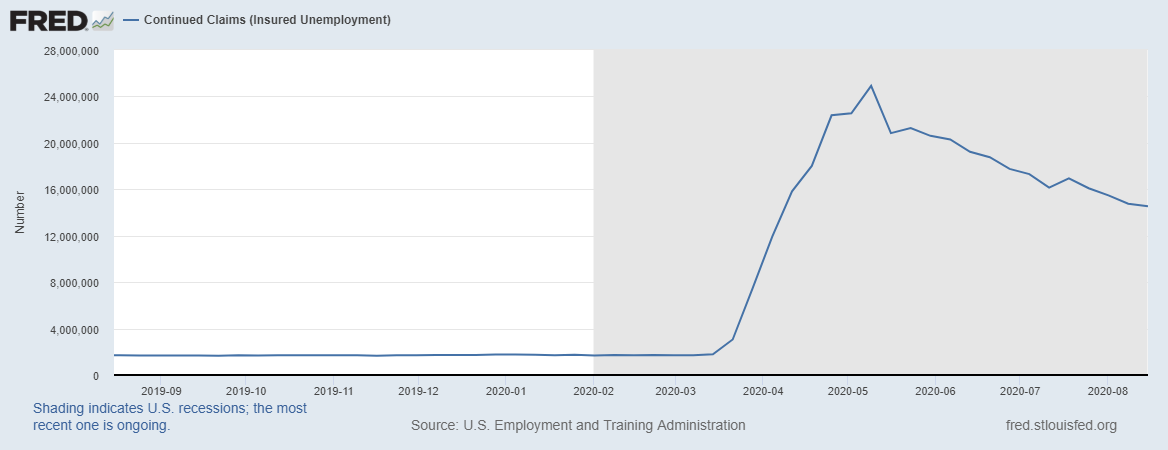

4. A decline in Credit Stress and Jobless Claims

Status: Complete

The St. Louis Financial Stress Index, possibly the most unloved metric among analysts in America, has made an impressive recovery and has stayed below my critical level of 1.21% and below zero for a while now. The index currently sits at -0.2468%. Credit stability is essential for a recovery phase so this metric is an important barometer for a functioning economy to recover.

While credit stress is low, jobless claims and continuing claims remain extraordinarily high. Continuing Claims are falling though – they just have a long way to go to get to pre-COVID level. As long as we are making progress in this area while continuing to provide fiscal and monetary disaster relief, we should not see a reversal of this positive trend.

Once we have defeated this virus, I believe the government will provide a major stimulus plan, as what they have been doing these last few months is really a disaster relief package. The goal is always to get a tighter labor market so wages can increase faster. This means it might be many years from now until the Fed raises rates.

5. Data from the hardest-hit sectors start to trend upward.

Status: Complete

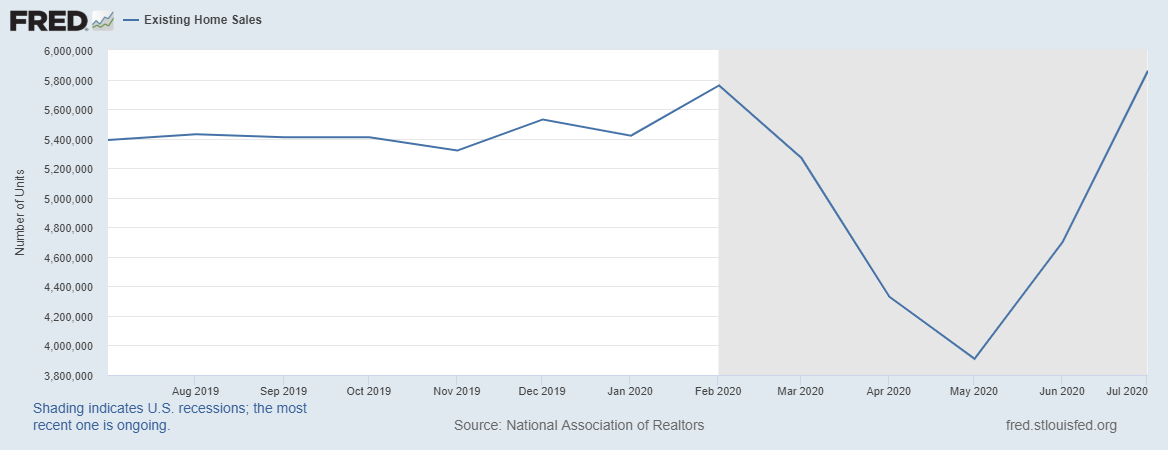

While housing was the first sector to show a V-shaped recovery, it is no longer the only sector in recovery mode. Some data lines like retail sales and Manufacturing data are showing V-shape recoveries as well. Other sectors may not be showing a dramatic V-shaped recovery yet, but the numbers are still showing improvement. We’ve been through a lot so it will take a while to get back to firing on all cylinders while this virus is still infecting and killing people every day.

The United States housing market was hit early on during COVID. We went from weekly double-digit year-over-year growth on the MBA purchase application data to nine straight weeks of negative year-over-year data. Since that ninth week of negative data, we have recovered to become the best-performing sector in the world. New home sales, pending home sales, existing home sales, builders confidence Index, mortgage purchase applications and housing starts have all shown V-shaped recoveries.

The two most important factors that drive housing, demographics and mortgage rates are both in sweet spots to support housing. If you consider Millennials as potential replacement buyers, then add in downsizing Baby Boomers and move-up home buyers, we should see a lot of activity in the housing market in the coming months and years. Plus, we still have 15%-20% of market sales purchasing homes with cash each year.

We only need 4 million mortgage buyers a year to have a stable market and this is out of over 140 million people currently working – and the job market is still in recovery mode. It’s very rare to have any existing home sales print under 4 million in the 21st century. Typically this happens around events such as the last few months of the housing bubble crash, the aftermath of the pull forward demand from the homebuyer tax credit, and one month of COVID-19 induced sales. With mortgage rates safely under 4%, we have the cushion of low mortgage rates as well.

When one puts all this into perspective, I think we can agree, the worst of times are largely behind us for the housing market. It’s time to start looking at our future with caution as long as this virus is still with us. We can’t forget the housing bubble boys are ready for the 2021 forbearance home-price crash trolling game plan. Trust me when I say this, I’ve got a few tricks up my sleeve for them.

Lastly, we are going through a lot right now as a country and the next four months is going to be full with more drama than we are used to. This is why I needed to see us make some progress by our Sept. 1 date: winter is coming. Just remember, darkness only wins if you allow it to. Love each other, fight for one another and remember, when it’s all said and done, even though we don’t agree with each other, we are all Americans.