Homeownership in America was a dream that became a nightmare for some during the financial crisis, and then became a hot topic of conversation for the last several years. We’ve got fresh data on homeownership — how does it look today? It seems perfectly right to me if you believe in demographics, affordability and credit profiles.

In the previous expansion, I always stressed that housing would have its weakest recovery from 2008 to 2019. Part of the reason homeownership rate fell during that time was that when people lose their homes legally, they are taken off the homeownership percentage. We had a lot of deleveraging that needed to occur in those years, and it took time. However, it’s 2022, so let’s look at the state of homeownership in America today and why it still looks right to me.

In 2019 I wrote: “Early in this economic cycle, one of the more controversial calls I made was that the homeownership rate would bottom at 62.2% – 62.7% in this cycle (2008–2019). This prediction was based on three facts: First, demographics during this period supported renting, not home buying. Our demographics were either too young or too old to be in the market to purchase homes.

“Second, over 8 million homeowners were delinquent on their mortgages, and once they lost their home, they would join the ranks of renters. Third, home-ownership and purchase applications were high and could not be sustained at that level with the weaker demographics for homeownership and no exotic loans to boost demand.”

The homeownership rate never got down to the 62.2% – 62.7% range like I thought it would in the previous expansion. The lowest we got was 62.9% and we have been rising since then.

The first-quarter homeownership data is now out, and after the crazy, unrealistic rise during COVID-19, that data has come down to a level that looks about right to me.

From Census: The homeownership rate of 65.4 percent was not statistically different from the rate in the first quarter 2021 (65.6 percent) and the fourth quarter 2021 (65.5 percent).

Part of my 2019 forecast for the next decade is that I believe the target rate goal for homeownership should be 66.21%. I don’t put any serious weight on the spike we had during COVID-19; this data line is usually very slow-moving, so like most COVID-19 economic data, put a giant asterisk on it and move on. Below is what I wrote back in 2019.

As I noted in 2019: “In the last few years, some pundits have been saying that expecting ownership to stay at 62.2% was too bullish. Today, we are less than a year away from the end of this cycle, and the homeownership rate has not gone below 62.2 %. The lowest rate we have seen so far is 62.9%. Now, I am going to make another controversial forecast. I believe the homeownership rate can get back to 66.21% at some point in the years 2022-2026.”

These were the reasons I gave back then:

1. The median age for first-time homebuyers is now 32, and the number of Americans in the range of 25-31 years is massive.

2. Boomers are staying in their homes longer, so they are remaining homeowners.

3. The loan profile of buyers during the post-2010 expansion is excellent, so when the next job loss recession happens, we won’t lose as many homeowners (compared to what occurred after the Great Recession).

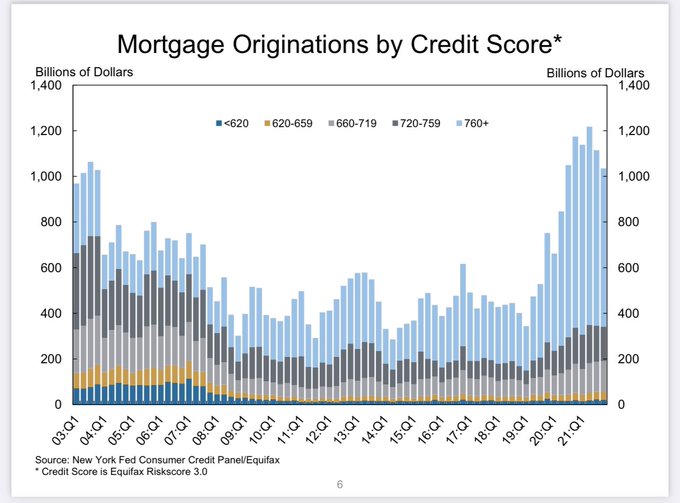

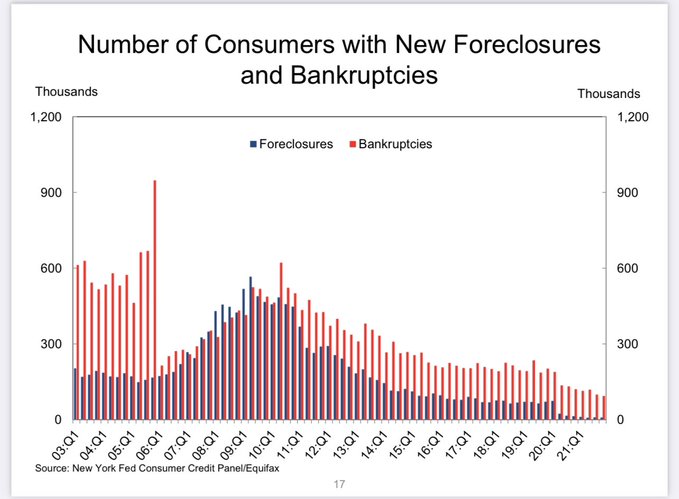

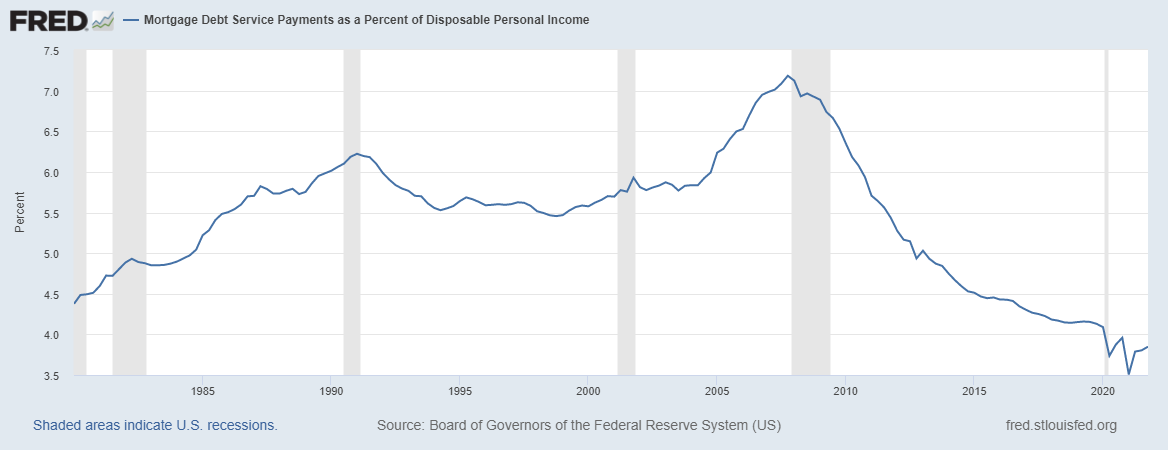

As you can see from the third point, the credit profiles of American homeowners were excellent in 2019. Who knew this would get tested so sharply in a global pandemic with forbearance programs in 2020 and 2021! Up for the challenge, I created the phrase the forbearance crash bros, knowing that the housing crash addicts in America lack a financial credit profile risk analysis background.

It was an easy layup for me to state that forbearance was never going to be the collapse of the U.S. housing market like these bearish Americans and foreign citizens were screaming about in 2020 and 2021. This was a significant victory for the United States of America, our people against the American bears.

As you can see below, the cash flow of U.S. households was and is still outstanding. Loans in U.S. are very dull, which is a good thing, and this won’t change anytime soon because we have made American mortgage debt great again.

This is important because, without a credit risk foreclosure or short sale, the homeownership rate uptrend will be more stable because we haven’t had a mortgage credit boom from 2014 to 2022. It was always slow and steady, and that is precisely how we should be dancing with consumer debt. The market of 2002-2005 not only had an explosion in debt growth, but the debt structures themselves were also very exotic.

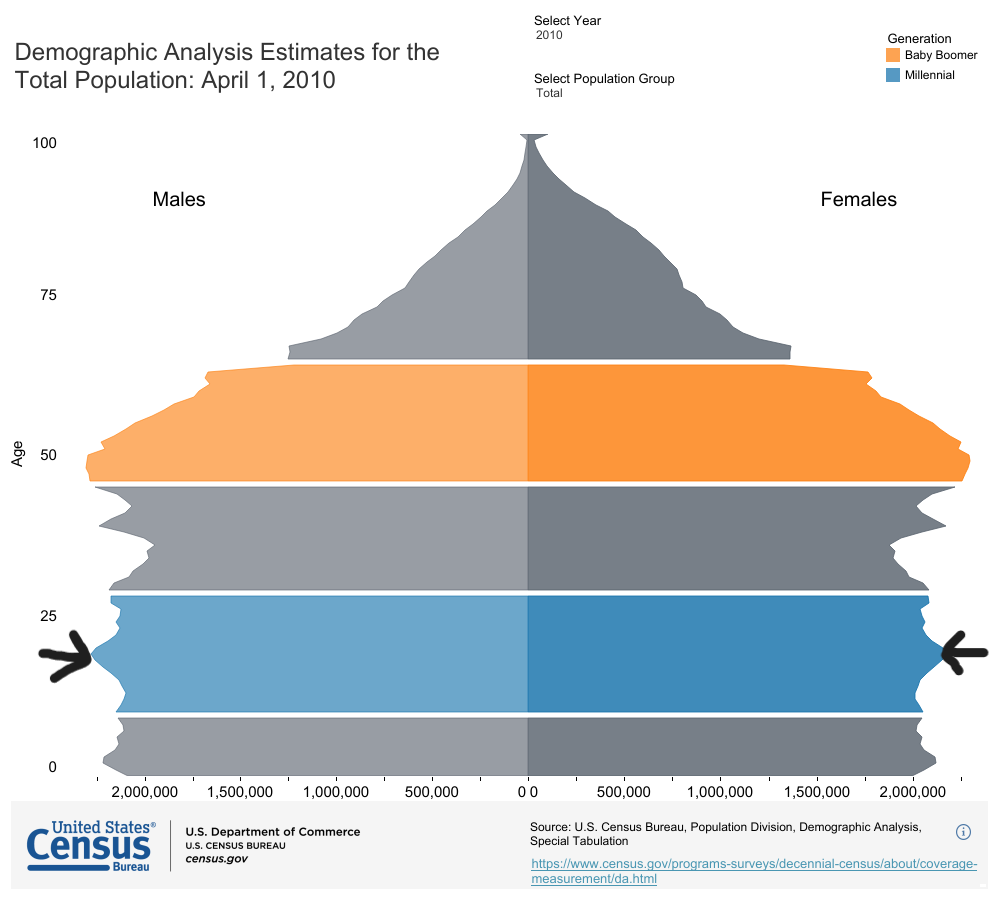

Going back to point No. 1 above, I noted that the average age of first-time homebuyers in 2019 was 32, and that the number of Americans in the range of 25-31 years was massive.

In contrast, the demographics in 2010 weren’t the best for real growth in mortgage debt and demand, as that cohort was only aged 19-24 — they were too young to be buying homes. Millions of people buy houses each year, but our substantial young demographic patch would have to rent first before they got to their home-buying age in more significant numbers.

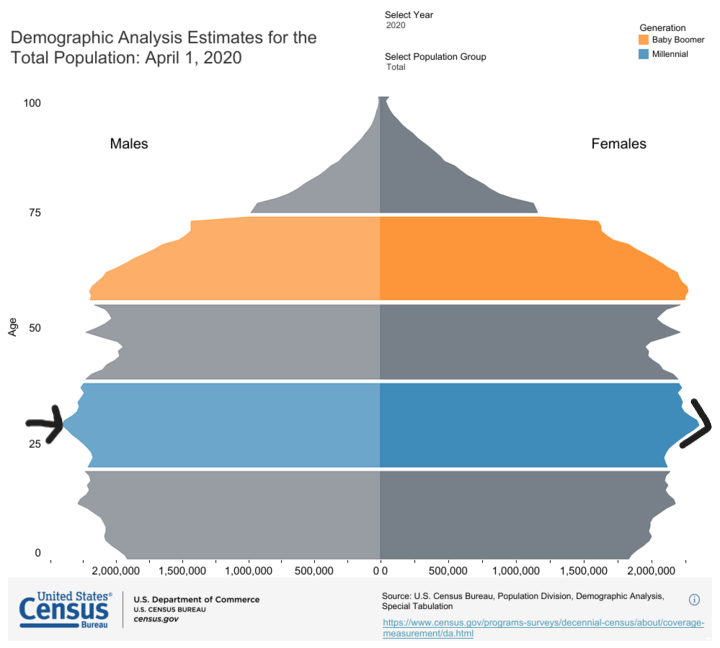

Fast forward to 2020, and currently, the most prominent housing demographic patch in America is ages 28-34. So you can see why housing demand has been stable and higher than what we saw from 2008 to 2019. This extra kick in demand, which I always refer to as replacement buyers, looks right to me. This is not a result of speculative demand, just more Americans running into the first-time homebuyers’ median age of 33.

We Americans aren’t that complicated. We rent, date, mate, get married and typically 3.5 years after marriage we have kids, which is when we don’t tend to live in apartments, condos, or townhomes. We tend to buy single-family homes, raise our kids till they grow up, and then it’s their turn.

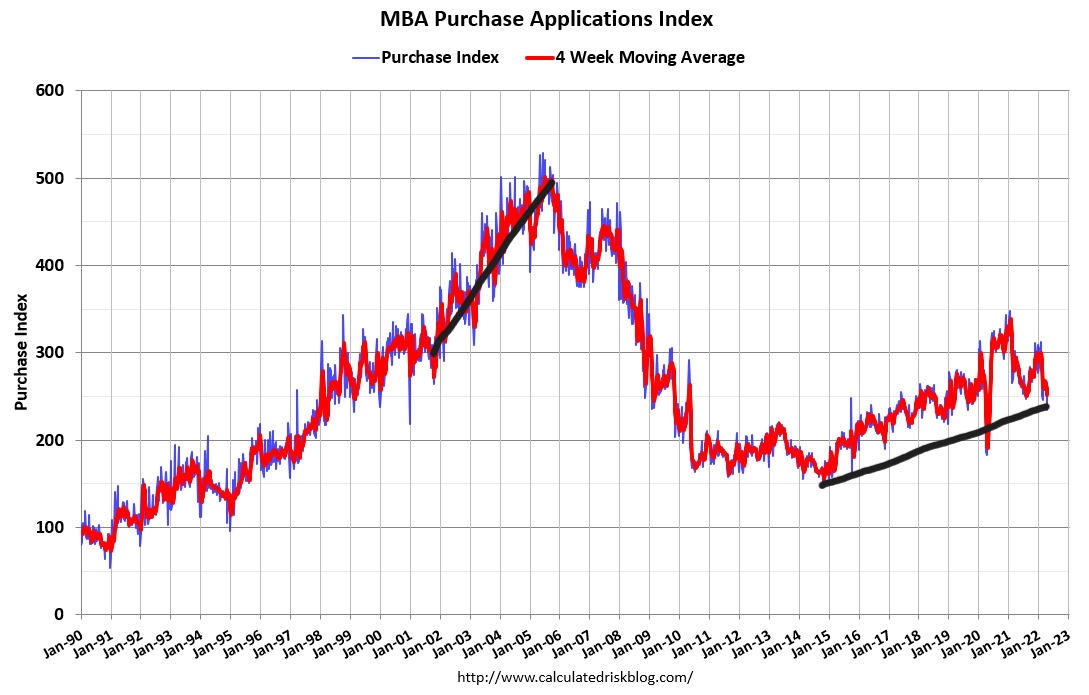

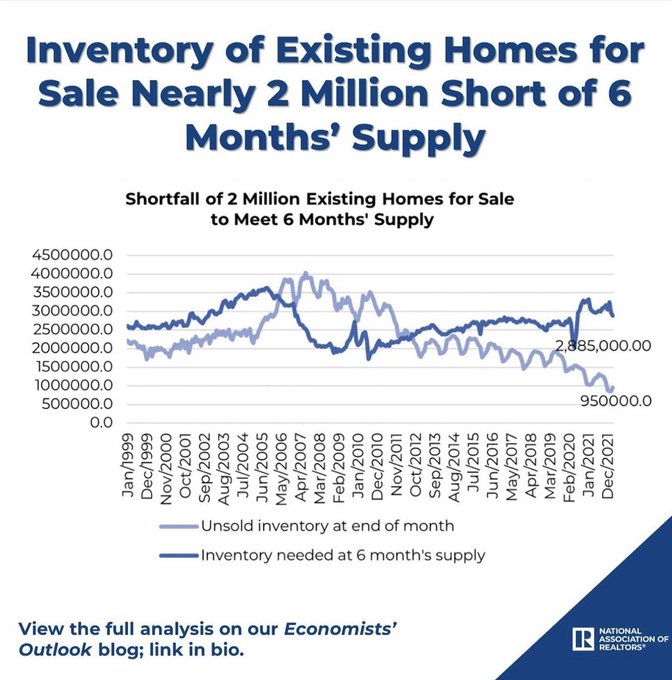

The one considerable risk for housing in the years 2020-2024 is that if demand picks up as it has, inventory breaks down to unhealthy levels. This has already occurred, and my 23% home-price growth cumulative level that I had targeted for 2020-2024 has been smashed in just two years. On top of that, in 2022, inventory got worse, and we are now in a savagely unhealthy year of home-price growth.

I have stated many times that the one big risk to my goal of total home sales levels of 6.2 million every year from 2020-to 2024 would be from home-price growth that rose too fast, and then we got a mortgage rate spike, which is what we are dealing with now.

The homeownership rate looks right today, and it’s on better footing than the rise we saw in the early 2000s. Families after 2010 have been sitting pretty in their homes with a fixed debt product and hedged versus inflation. Since the American homeowner looks excellent on paper today, my forecast call for 2022-2026 of a 66.21% homeownership rate should come true. If it doesn’t, affordability won the battle versus demographics, keeping more people from owning homes.

No matter what happens, the American homeowners who bought homes over the last decade are in great shape, and they’re living the American dream. And this time, no credit risk blow up nightmare is waiting around the corner — just ask the forbearance crash bros how their housing collapse call for 2021 went.

This is great info – really appreciate the insight and perspective!

Echo that, Atrion!