The 2022 housing market was savagely unhealthy, with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Housing went into a recession in June and mortgage volume fell off a cliff.

So where does all that drama leave us for 2023? Buckle up as we look at each factor individually.

Home prices

Recapping 2022:

Last year, my price forecast anticipated a noticeable deceleration in price growth, even with inventory levels at all-time lows and mortgage rates still below 4% at the start of the year.

I wrote then: “I am looking for total home-price growth to be between 5.2% and 6.7% for 2022. This would be a meaningful cool down in price growth but would still be a third year straight of too much price growth for my taste.”

That price forecast will be incorrect, as home prices will likely end up between 6.8% to 8.3% in total for the year. What did I get wrong? Well, prices took off in early 2022; January, February, and March saw accelerated price growth as bidding wars took off in the year’s first three months. This was happening while sales trends were also falling in February and March.

It got so bad that I labeled the housing market savagely unhealthy in February and deemed it the worst housing market post-2010, as inventory broke to all-time lows and mortgage rates were simply too low to stop the bidding wars. In February, I called for higher rates to help cool the madness.

Price growth was unhealthy in 2021, and it was savagely unhealthy in the first few months of 2022. I had a strict five-year price growth model for 2020-2024 that said the only thing that could ruin housing in 2020-2024 would be if prices grew above 23% in less than five years, a real risk in this period.

Well, that price model got smashed with 30% price growth in just two years, and it was getting worse early in 2022.

Assuming an 8% growth level in 2022, I would need a 15% decline nationally to get my model back in line to be at the upper end by the end of 2024. Going back to 2013, I have stressed that my affordability index gets tripped up if mortgage rates get above 5.875%, and wrote about this in 2019 as we were about to enter my critical period of 2020-2024.

My 2023 price forecast:

As long as rates stay above 5.875%, my affordability index will see the pressure on home prices continue. For 2023, assuming rates stay above 5.875%, we should see a 5.9%-7.4% national home price decline. The higher the rate from this level, the more significant hit to affordability we will see.

I have been forecasting since 2010 and I’ve only predicted price declines for 2011 and 2012. From 2013 to 2022 I forecasted price growth every year. Hopefully, with my explanations above, you can see why I have discussed prices falling in 2023 due to rates getting above my key level and home prices accelerating above my price growth model tied to this period.

Mortgage rates

Recapping 2022:

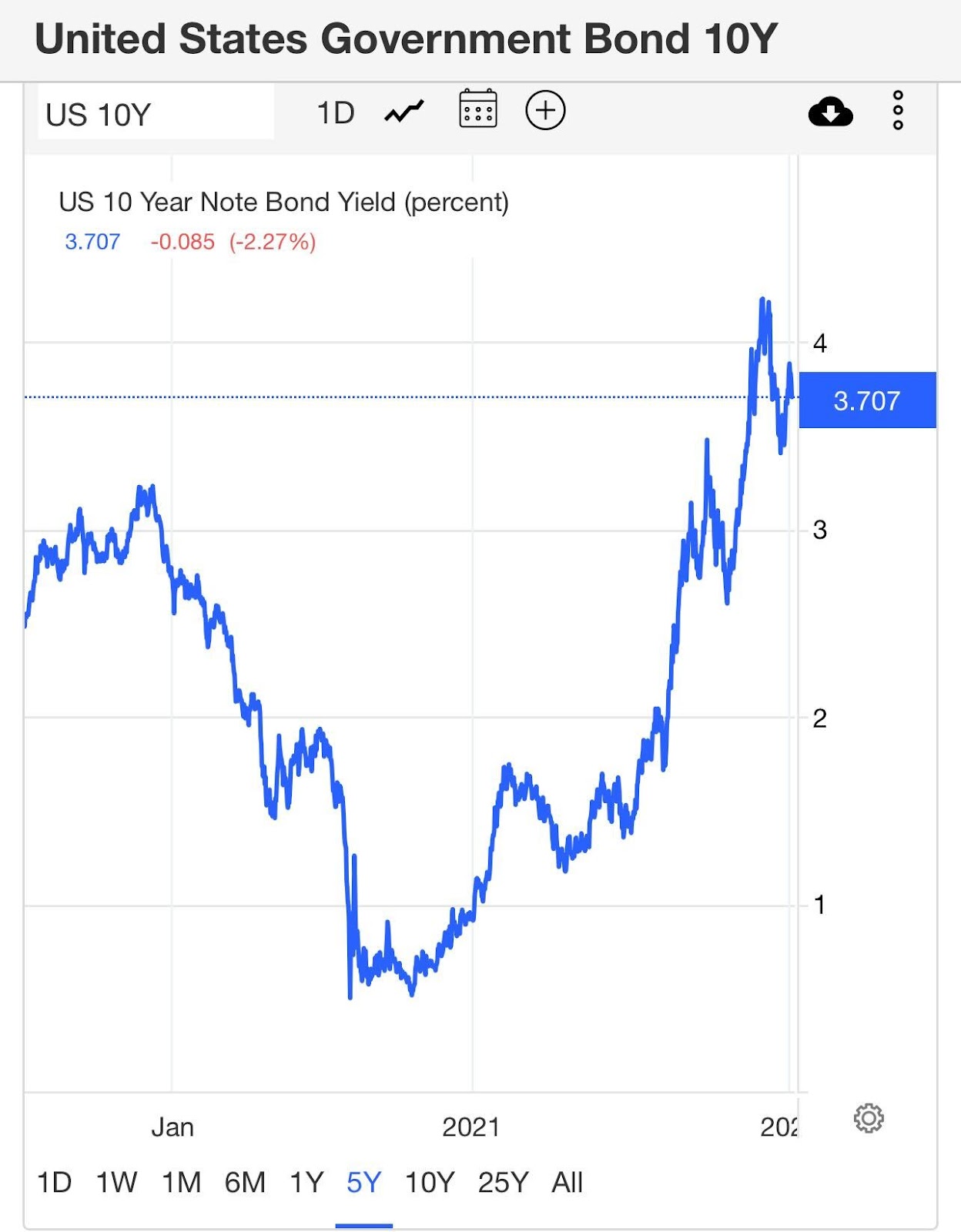

To say we had a historic year in mortgage rates and the bond market in 2022 is an understatement!

How I look at rates is intertwined with how I look at the bond market. In the previous expansion, starting in 2015, I had the same bond forecast every year of 1.60%-3% on the 10-year yield, which roughly means mortgage rates in the 3.50%-4.75% range. It broke under and over those critical levels for a brief time but for the most part it stayed the course.

When it became apparent that COVID-19 was about to break the economy short-term, I talked about the 10-year yield getting between -0.21% and 0.62%, which would lower mortgage rates. In 2021, my bond forecast range was 0.62%-1.94%, and we reached a high of around 1.76% that year.

Since 2019, the critical factor for my economic work has been the 10-year yield breaking 1.94%. However, last year was the first time post-COVID-19 I thought the 10-year yield could break over 1.94% if global yields rose, specifically if Germany and Japan’s 10-year yields rose.

Last year we were trending to break over 4% plus mortgage rates as global yields rose, but everything changed after March. The Federal Reserve reversed course on its slower-than-normal rate hikes, the Russian Invasion spiked oil and wheat prices, and all hell broke loose in the 10-year yield and mortgage rates.

A 10-year yield of 1.94%-2.42% means 4%-4.5 % mortgage rates, and you can make a case with a bad mortgage-backed securities market for rates to reach 4.75% to 5% — that’s it. Nothing in my forecast had mortgage rates of 5.875%-7.37%. Once the Fed talked about a housing reset and being a single mandate Fed to fight inflation, everything changed.

My 2023 rates forecast

In October, I wrote about the case for lower rates going into 2023. Since that article, mortgage rates did fall from 7.37% to 6.12%, then went back up to 6.54%.

For 2023, the inflation growth rate is falling, regardless of what the Fed believes or doesn’t believe. Unless we have another supply shock, there is no way to have massive spending to push durable good pricing crazy again. American households had $2.1 trillion in excess savings during the pandemic, which has now been drawn down to $900 billion. The Fed has expressed concerns about the massive excess savings consumers had but it looks like the majority of that will be drawn down by the end of the year.

For 2023, the 10-year yield is currently at 3.70% and I believe the 10-year yield range this year will be between 3.21%-4.25% as long as the economy stays firm. Now if the economy gets weaker, especially in terms of the labor market breaking, which for me is jobless claims rising to 323,000 and beyond, then we can get as low as 2.73% on the 10-year yield.

With that 10-year yield range (3.21%-4.25%), mortgage rates should be between 5.25%-7.25%. This assumes that the spreads are wide and pricing for mortgages is still weak. However, if the spreads get better, we could even see mortgage rates under 5% if the 10-year yield breaks under 3%

I have tied the Fed pivot to jobless claims breaking and believe the bond market will get ahead of the Fed on that. That could bring the 10-year yield back below 3%. That would be a positive for demand.

We’ll be following this line very closely in my new Housing Market Tracker that publishes every Monday. This is why it is critical to follow the weekly tracker data as we will focus on the jobless claims data each week to see when that data line makes the Fed become a dual mandate Fed again.

Housing Inventory

Recapping 2022:

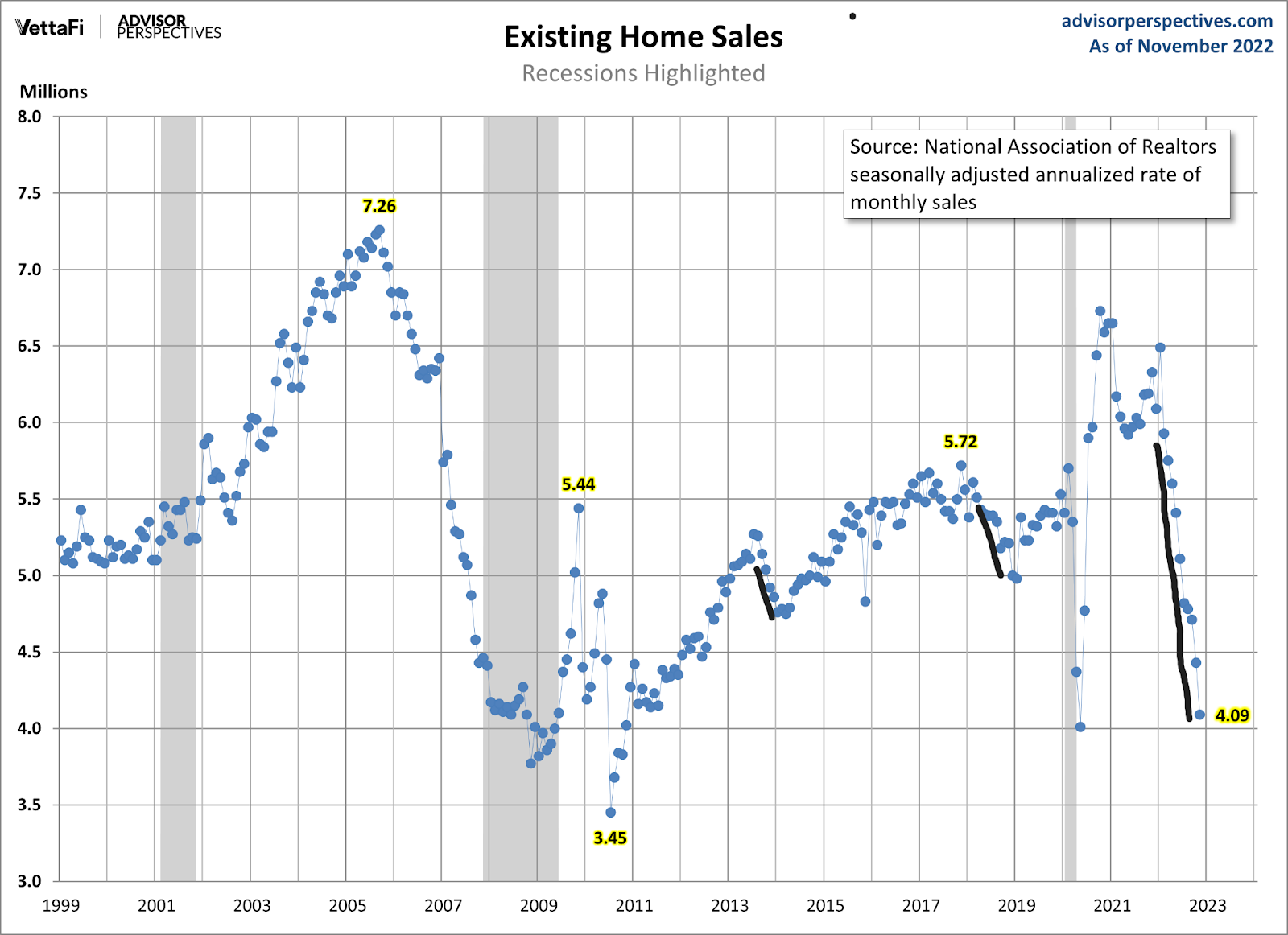

One of my big forecast calls from last year was that I believed as a nation we could get back to 2019 levels of inventory on a national basis using the NAR number of 1.52-1.93 million in 2023. I made this call in June of 2022 in an interview with Mike Simsonsen of Altos Reseach on his Top of Mind podcast.

However, weeks after that call, the new listing data started to decline noticeably, which makes that call much harder to happen in 2023. For some context, going back to 1982, the historical average range has been between 2 million and 2.5 million. We are currently at 1.14 million and the all-time low was 860,000 at the start of 2022. As we can see below, we are far from the historical norms today.

My 2023 inventory forecast:

I am still sticking to my call that we break into the 2019 inventory levels of 1.52-1.93 million for 2023. However, I acknowledge that the housing dynamics have changed a lot since that forecast in June as new listing data declined.

It will be nearly impossible to get national inventory back to 2019 levels if we don’t get traditional new listing growth as we simply don’t have enough homes on the market to get back up there in 2023 otherwise.

Housing recession

My 2023 housing recession forecast:

The Housing Market went into recession on June 16, 2022: sales were declining, production is about to decline, and jobs are being lost, with total incomes falling as well. I talked about this housing recession on CNBC last year. Of course, what can change this housing recession is simple: we need lower mortgage rates to boost up demand. This is also something I talked about last year on CNBC.

On a positive note for lower mortgage rates, the Federal Reserve finally got the memo that rent inflation lags badly on the CPI data, and this year this should be a positive story. I said in this interivew, that by January and February it would be evident that the growth rate of rent inflation would be falling.

Well, the Fed got the clue and created an updated version for rent inflation that doesn’t have such a lag, so they can exclude that data when looking at the progress on fighting inflation. This to me is a real big deal and a positive for the U.S. economy.

Existing home sales fell very fast in 2022 due to higher mortgage rates and a lack of new listing growth, which meant the number of traditional sellers who bought a home was much lower in 2022. The bar is so low in sales data for 2023 that we can trip over it, so the key for sales is to track purchase application data and how rates impact that data line that looks out 30-90 days.

This is another reason I created the Housing Market Tracker — to understand better the forward-looking data regarding sales, purchase apps, rates and inventory.

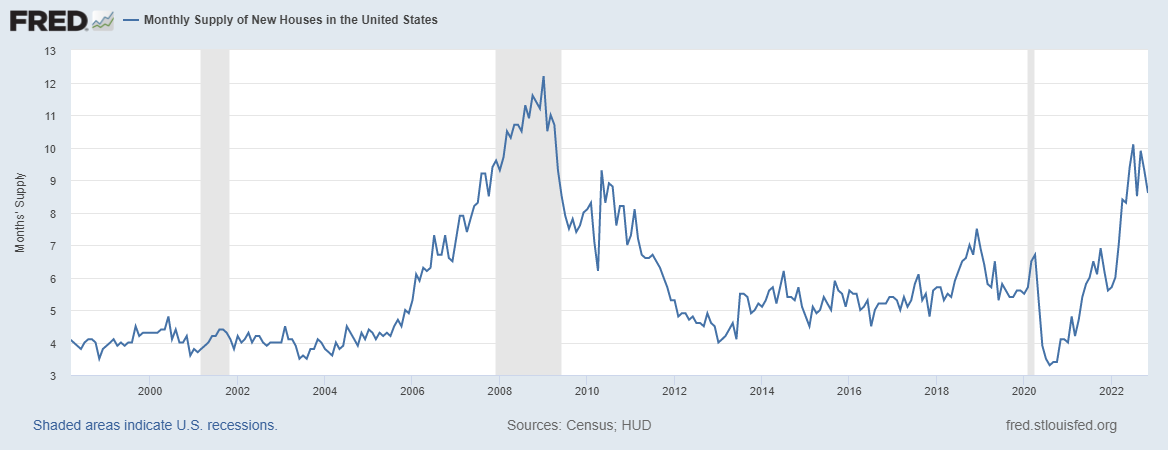

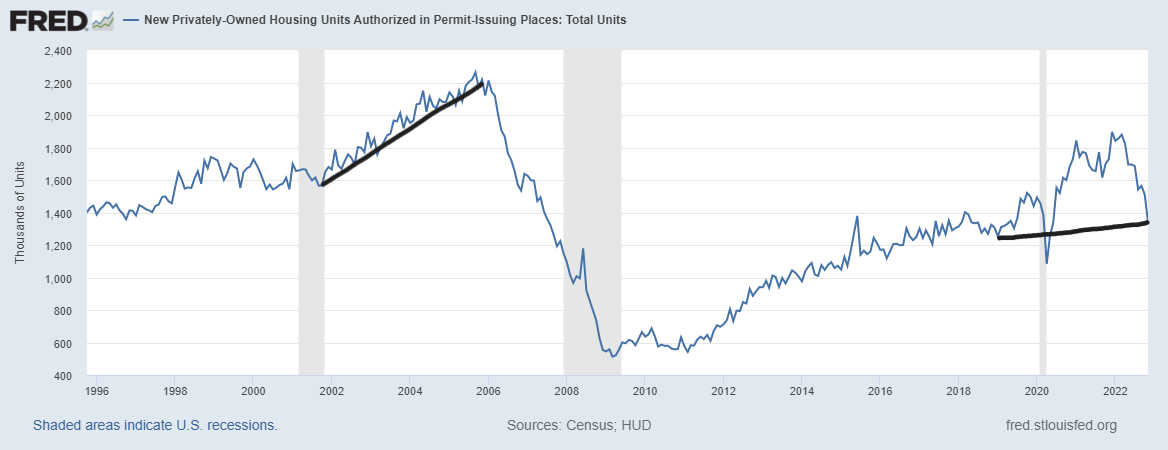

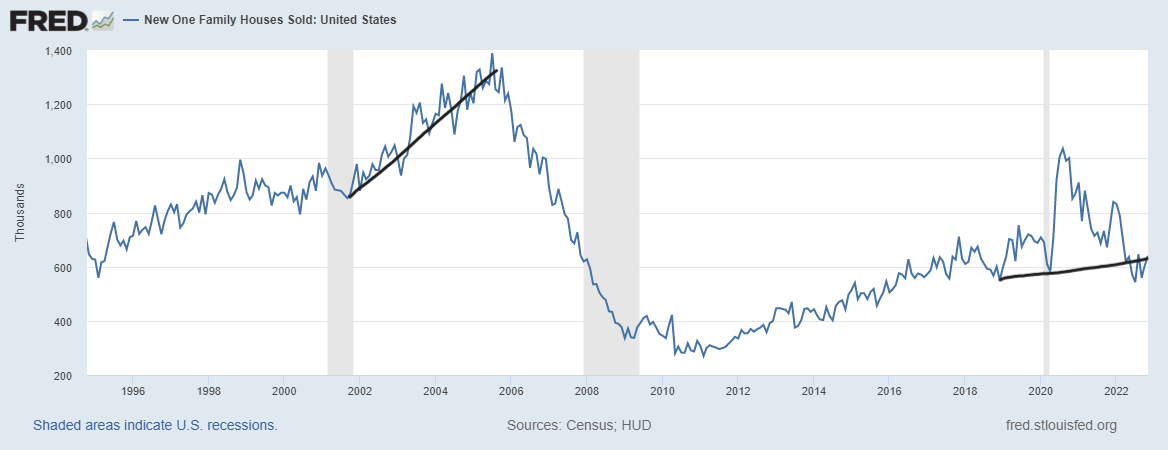

The new home sales sector and housing starts are in a recession and won’t get out of this rut until monthly supply gets below 6.5 months on a three-month average and new home sales are growing. We are at 8.6 months with many homes still under construction or haven’t even started being built yet.

Housing permits and starts will keep falling this year until the above dynamics change. The builders are here to make money and need a financial motive to supply a marketplace when the monthly supply is over 6.5 months, which makes the job harder. However, it’s 100% clear that the builders are in a much better position now to deal with this housing recession than the one from 2005-2008.

One of the reasons why is that new home sales are already historically low today. Even though the headline number is inflated because it doesn’t account for cancelation, sales haven’t gone anywhere for a while after those adjustments. If mortgage rates fall more, the builders will have an easier time moving products.

The general economy

My 2023 general economy forecast:

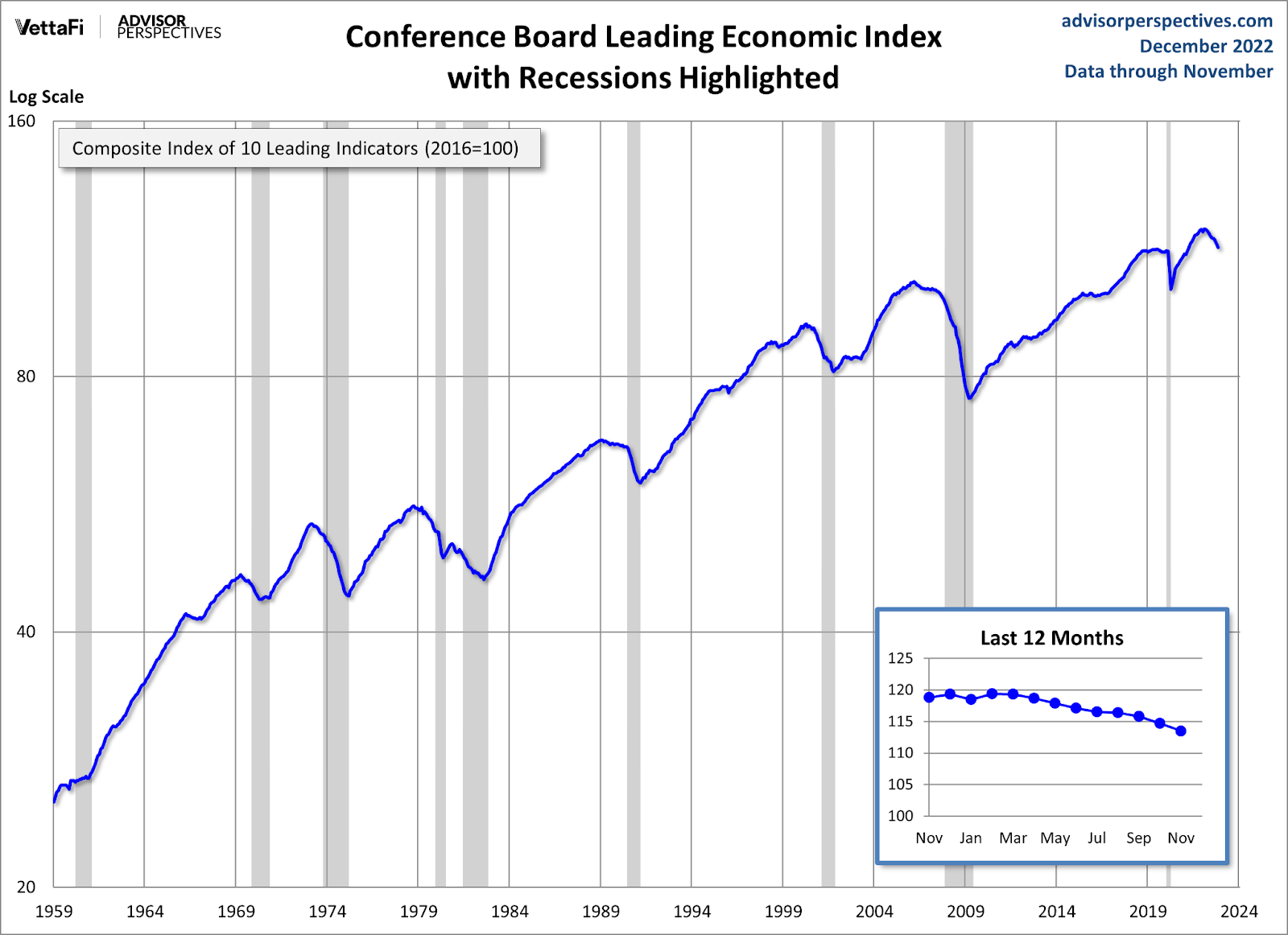

The forecast for the general economy is simple to track for the year 2023 because, on Aug. 5, 2022, I raised my sixth and last recession red flag before making a presentation about my recession model to the Conference Board on July 27.

Applying my model to data starting from the late 1960s, whenever my six recession red flags are raised, a recession isn’t too far away, although sometimes it’s quicker than others. For example, the last time my six recession red flags were all up was late in 2006 and the recession didn’t start until 2008.

We can avoid a recession in 2023 in the U.S. but this would require the growth rate of inflation to fall, which it should. However, the key data line for 2023 is jobless claims. If it stays away from my critical level of 323,000 on the four-week moving average, we won’t have a recession in 2023. Here’s my model for avoiding a recession in the near term, which requires the growth rate of inflation and mortgage rates to fall.

Conclusion

As we can see above, we dealt with a lot of high-velocity crazy data in the housing market of 2022. It’s time to move on to 2023, and this is why I believed it was very critical to create a tracker for weekly housing data because things can turn on a dime, and one year forecast just won’t cut it in this environment.

The plague of housing inflation still haunts both houses, as the star-crossed variables of home prices and mortgage rates sent housing into a recession in 2022. However, a light can be seen, even though the distance is long. A pathway for housing market stabilization can happen if those variables fall together.

HousingWire will host a Housing Market Update on Feb. 6 featuring Lead Analyst Logan Mohtashami and Altos Research President Mike Simonsen. Find out more here.