One of the biggest questions in real estate right now is how rising interest rates will impact the housing market. This used to be a pretty easy question to answer: when interest rates go up, it costs more to purchase a home, and demand drops. Price appreciation slows, and homes take longer to sell. More expensive money also meant fewer investors holding homes so inventory would climb too.

This year, the numbers aren’t that straightforward. The market has been so hot, many worry that rising rates will finally be the catalyst to pop the bubble. Yet, even as rates have begun to climb, homes are still flying off the market nearly three times faster than before the pandemic. The price of new listings continues to rise, which is a very bullish indicator for sales prices in the coming months. Americans have been lined up to buy homes for so long that increased costs haven’t deterred any demand… at least, not yet.

That being said, if interest rates continue to rise, we may see some small shifts in the market, and a short window of opportunity for eager buyers.

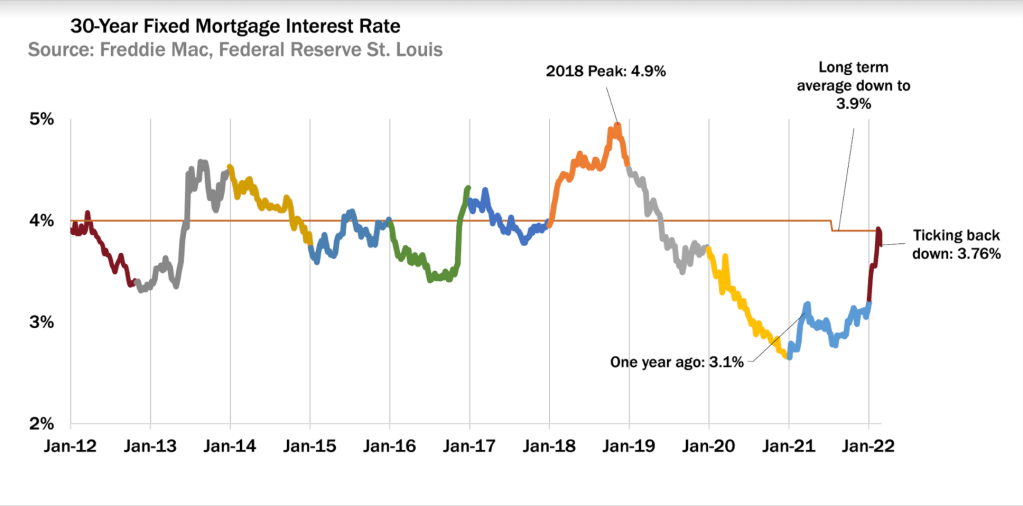

Fortunately we have 2018 as a guide to understand the impact of rising interest rates on the housing market in 2022. From September 2017 through November 2018, the 30-year mortgage rate rose from 3.8% to 4.9%, which was the highest point in the whole decade.

Based on the patterns from 2018, here’s what to expect, and the most important signals to watch:

1. Inventory will inch up… but not much.

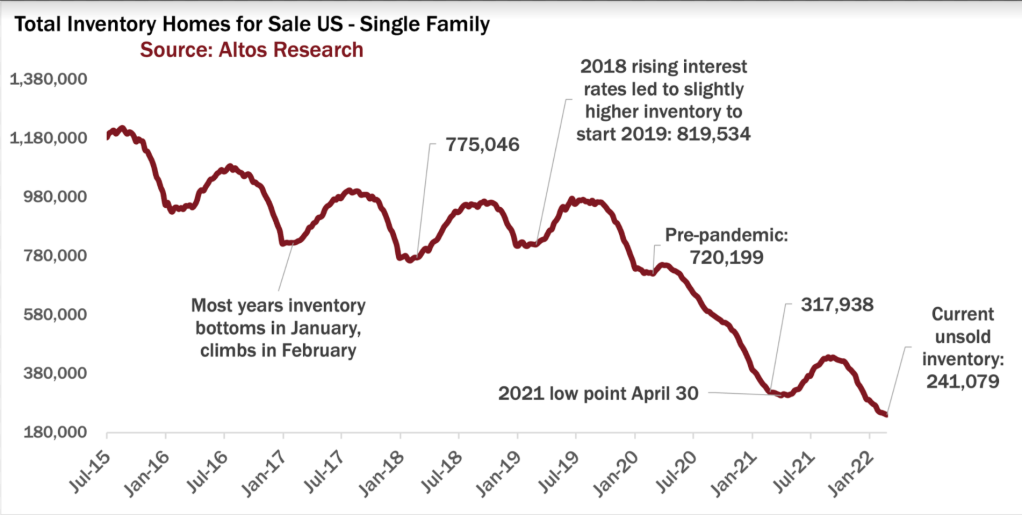

In the 2010s, as interest rates remained low, more and more Americans became real estate investors, and available inventory of homes for sale dropped every year. That trend reversed for a short time in 2018 when mortgage rates rose, and in 2019 we began the year with 7% more inventory than in the previous year.

If interest rates climb above 4.5%, we’re likely to see this pattern repeat, which would add some more listings to inventory. But because nearly all American homeowners have a 30-year fixed mortgage below 4%, most will choose to hold onto that mortgage instead of selling.

2. Home price growth will slow, but don’t expect prices to drop.

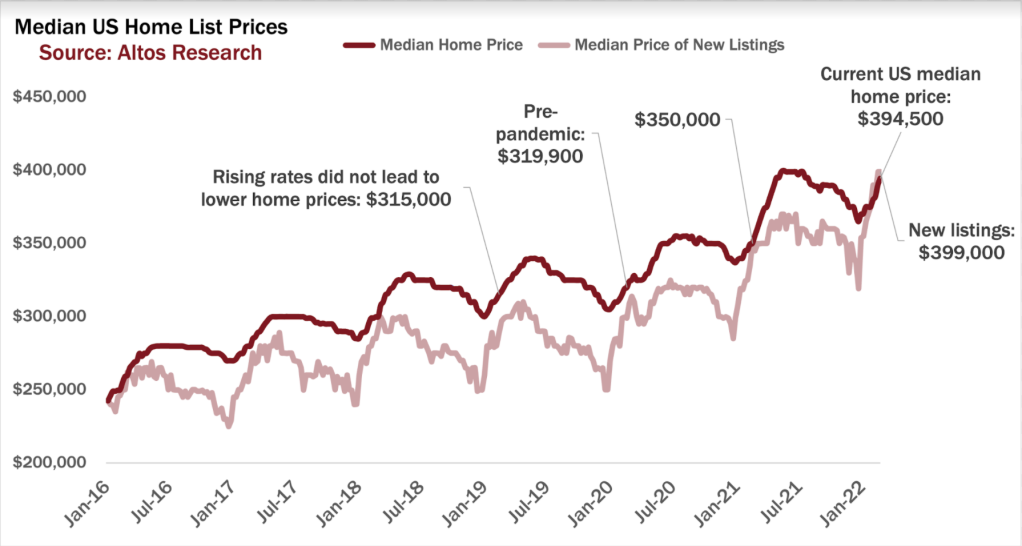

With so much demand and rapidly shrinking inventory, home prices have continued to rise in Q1, even with higher interest rates. The median home price for single family homes this week is $394,500, which is about 12% higher than last year at this time. Other leading indicators of home prices in the data are all bullish for future transaction prices.

Let’s look at what happened in 2018: even as interest rates rose and payments got more expensive, this didn’t result in any price drop. In fact, the median home price rose from $299,000 in early 2018 to $319,000 one year later. Why? Because in real terms, those mortgage payments were still a good deal.

Also, you can’t fight demographics. In 2018, demand was accelerating as Millennials moved into prime home-buying years. This is just as true today and will remain true further into the 2020s. As a mortgage lender recently told me about his first-time home buyer business, “life events don’t care about mortgage rates.”

And let’s not forget the effect of inflation. “Real” interest rates are the difference between inflation rates and mortgage rates, and in the inflationary economy of 2022, real interest rates are negative. Inflation is currently running at 7% annually. If your mortgage is at 3%, 4%, or even 6%(!) you’re still in a better financial position than you were last year.

3. Homes will take a little longer to sell.

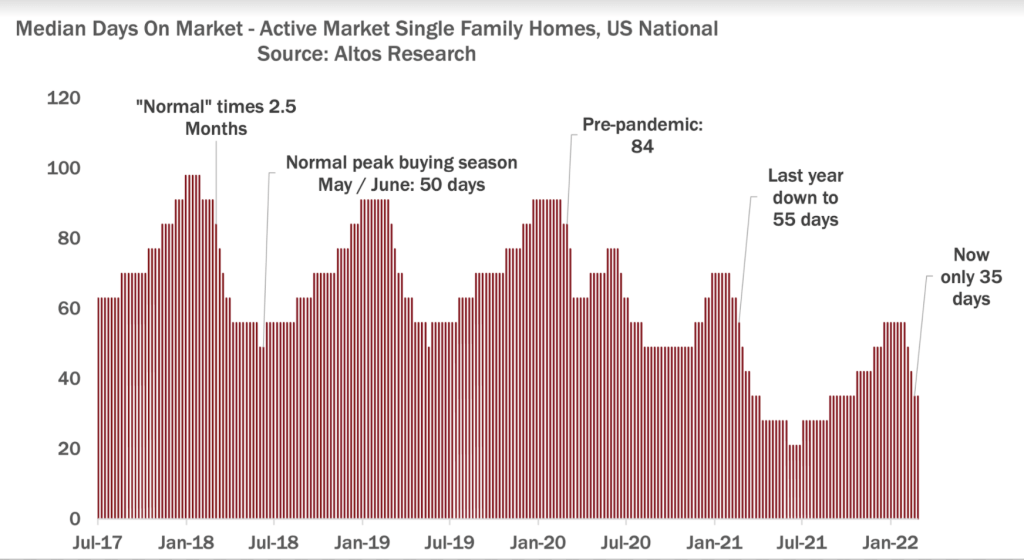

In a “normal” market, we generally expect it to take an average of 80-100 days to sell a home; over the past two years, that’s dropped to just 35 days. In fact, according to Altos Research data, one-third of homes are now sold in hours or just a few days.

If prices and mortgage rates continue to rise, we’re likely to see the breakneck pace of the market slow down a little bit. There will be a little less competition. Buyers may be able to take their time and do full diligence on a house and not have to make an offer that afternoon. We will also likely see price reductions start to tick up, because more people who overprice their home won’t be getting those immediate offers.

Of course, these numbers may look different depending on the location, and investor-heavy markets such as Phoenix will likely be more sensitive to interest rate changes. Deals get less appealing when money gets more expensive. Look for slightly more inventory, slightly longer market time in these markets.

So to sum it all up: as we enter into spring, while all the leading indicators continue to show robust demand, rising interest rates could have a small cooling effect on the market. Buyers should move quickly during this window of opportunity. If history is any indication, it won’t last for long.

Mike Simonsen is the Founder and CEO of Altos Research.

Excellent summary. Thanks Mike!

The best explanation. Thank you Mike 🙂