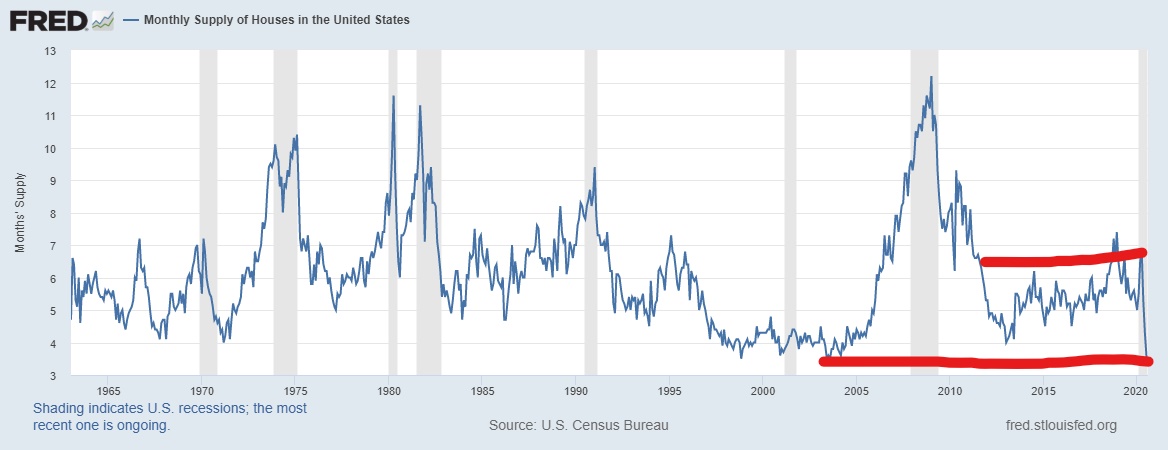

The recent new home sales data is at levels last seen in 2006, with monthly supply back down to the low levels seen the last time new home sales data was really strong.

For the first time in more than a decade we have the demand needed to prompt builders to really push housing starts. This growth in demand is consistent with what I have been saying for many years – if interest rates stayed low, good housing demographics in the years 2020 to 2024 would substantially drive up demand for housing, including new home sales. .

However, we did have a bump on the road getting here.

Compare today’s housing market with that in 2018, when mortgage rates were heading toward 5% and monthly supply went above 6.5 months. The monthly supply of new homes was mostly higher every month in the previous expansion (2008-2019) than any period from 1996-2005. At that time, the new home sales sector got so bad that I put it in the penalty box. Many assumed that this was the peak for new home sales – but I cautioned against this idea.

In December 2018, I wrote: “Despite the terrible optics for the new home sales market, I caution everyone not to assume that we have hit our peak and are heading for an epic crash in housing starts and new home sales. New home sales and starts are still very low.”

Now in 2020, we are seeing a spike in new home sales back to levels we enjoyed post 1996.

Likewise, the monthly supply for new homes is back down to the levels we saw when demand for new homes was good and builders responded with increased housing starts. Except this time around, we do not have speculation buyers and a credit bubble — just good demographics and low mortgage rates.

Some are making the erroneous assumption that the COVID-19 pandemic is the main driver of housing demand because workers are flocking to the suburbs and buying bigger homes to accommodate working from home, home schooling, home gyms and the like. But it doesn’t square with the data.

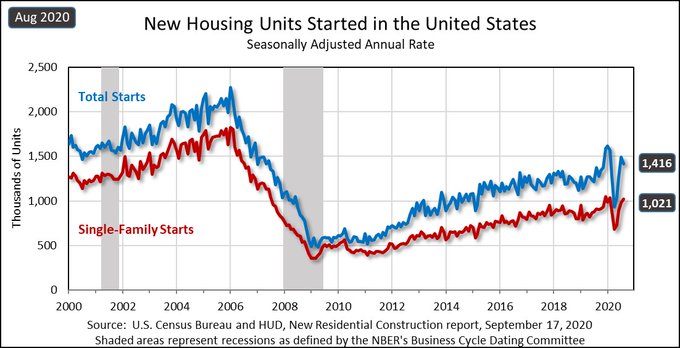

Back in February 2020, before COVID-19 hit, housing starts were showing near 40% year-over-year growth and mortgage demand for housing was good. The pandemic drove starts down temporarily, not up, but it could not kill off the organic demand due to the one-two punch of good demographics plus low interest rates.

These two factors are what will pave the way for housing starts to grow. Demand is what drives housing starts, not politics or housing pundits who say we need to build more homes. The builders are not a public service. They are in the business to make money, and were following their fiduciary duties to limit new developments from 2008-2019 because demand never warranted housing starts above 1.5 million a year.

A massive home-building plan to increase inventory in order to create better housing affordability would not be in their interest. This could only be done with significant federal deficit financing along with reversals of NIMBY zoning laws.

HousingWire Annual

Join Logan Mohtashami, Doug Duncan, Rob Dietz and other top economic analysts at HousingWire Annual 2020!

Reserve your seat today.

Don’t be surprised and lose faith if we get some negative revisions in our new home sales data as these last few prints were beyond normal hot. Instead, believe in the trend. It is legit. The U.S. housing market in 2020 is the most out-performing economic sector globally, driven by the best housing demographic patch ever with the lowest mortgage rates.

The backdrop for 2020 was a good one as housing starts were flat in 2019 after working off the excess inventory created when mortgage rates hit 5%. The new home buyer is older and makes more money than a traditional existing home buyer. We have plenty of people that can keep the new home sales data moving positive as long as mortgage rates stay low, and they should. The new home sector is especially vulnerable to increases in mortgage rates. When the economy is growing again, and the bond yields rise, keep an eye out for softening in this sector if the 10-year yield breaks over 1.94%.