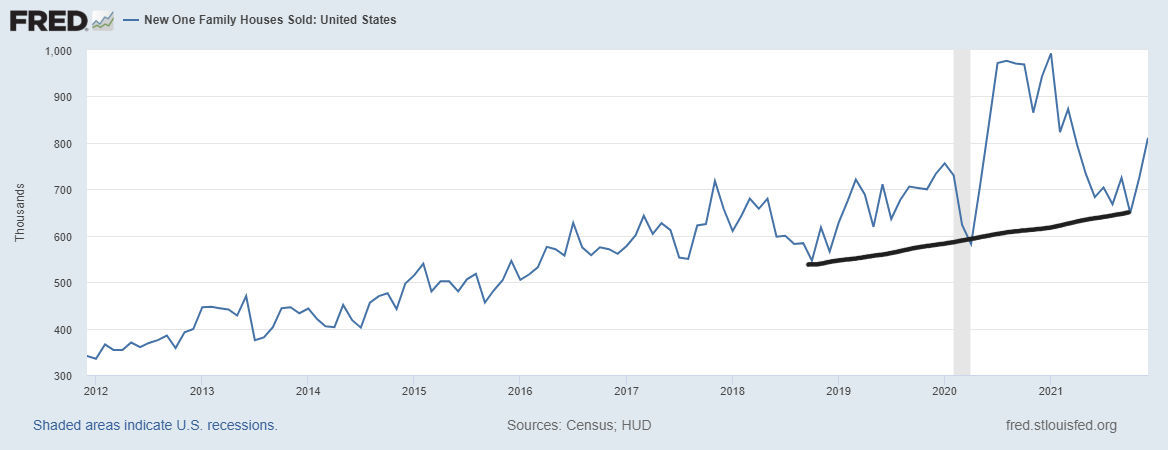

Today the Census Bureau‘s new home sales report came in as a beat of estimates at 811,000. The headline beat surprised many people, but the report’s internals show negative revisions for the previous months. The bearish take on housing for the second half of 2021 didn’t really pan out, especially in the new home sales sector.

What I believe occurred is that some housing investors took the decline in builders confidence and the increase in monthly supply to push that something bad was going to occur quickly. In reality, as we talked about many times on HousingWire, housing data was going to moderate, find a base and work from that COVID-19 surge in the data.

Now that 2021 is wrapped up, we can see this is what happened and I believe that was misread by some people. However, with that said, it’s still just an OK housing market for me based on how I view the new home sales market. Not everything in housing has to be smoking hot or an epic crash — a slow and steady dance can make the evening just right.

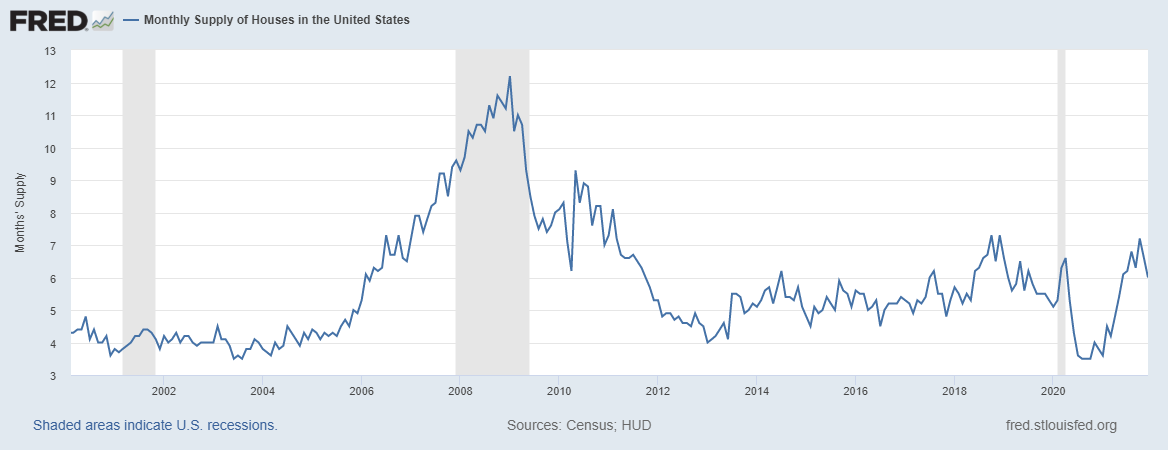

From Census: The seasonally adjusted estimate of new houses for sale at the end of December was 403,000. This represents a supply of 6.0 months at the current sales rate.

My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- When supply is 6.5 months and above, the builders will pull back on construction.

The headline supply number is six months with a three-month average number of 6.6 months. While we have seen a monthly decline in supply, we always want to keep mindful of the three-month average because the month-to-month numbers can be wild, both positive and negative.

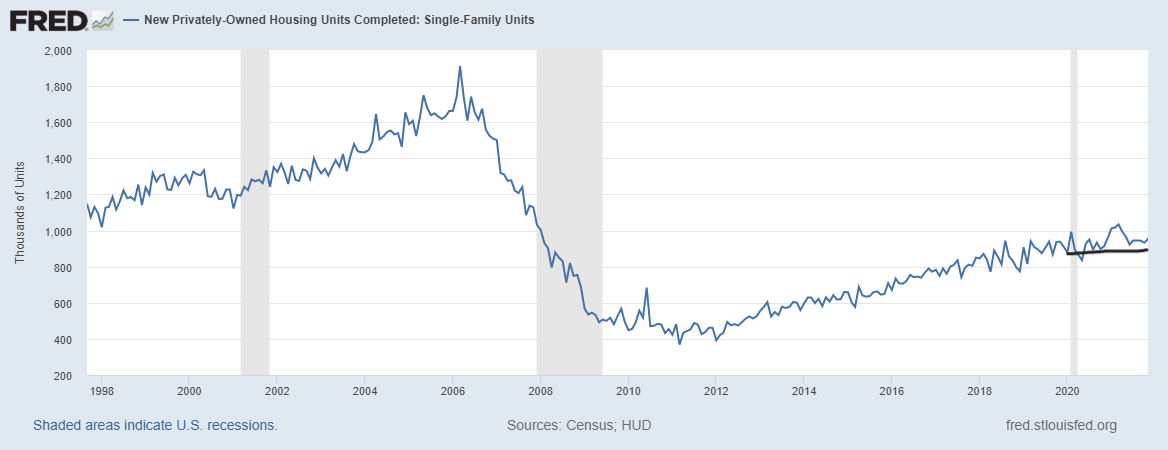

Of course, we all know what is going on in the U.S.: it’s taking forever to build and complete a home. The saddest housing chart we have in America is the total completion chart for housing starts. It is an embarrassment, but construction productivity — which has been terrible for decades — is now also dealing with shortages that delay finishing homes. Also, since robots and immigrants didn’t take all the jobs in America, we have a higher-than-normal level of job openings for construction workers.

The new home sales market is doing its slow and steady dance upward, which is typically the case as long as mortgage rates stay low. This isn’t a booming home sales market and the existing home sales have clearly been outperforming recently versus the new home sales.

From Census: New Home Sales Sales of new single‐family houses in December 2021 were at a seasonally adjusted annual rate of 811,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 11.9 percent (±20.3 percent)* above the revised November rate of 725,000, but is 14.0 percent (±16.6 percent)* below the December 2020 estimate of 943,000

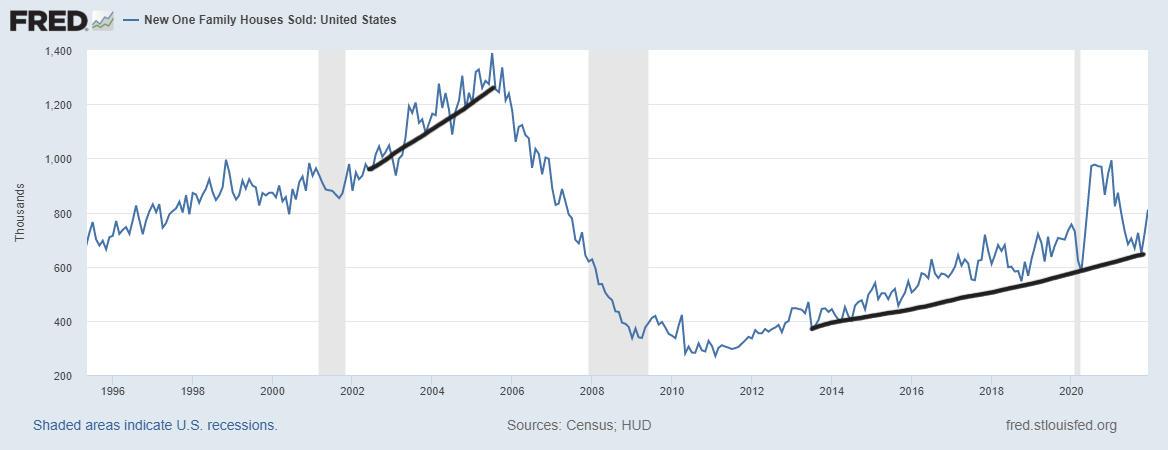

Slow and steady wins the race and the market that we had from 2002-2005 doesn’t exist today. The credit boom that facilitated new home sales then no longer exists, so while sales levels are nowhere near the peak of the housing bubble years, this should be viewed as a positive because we never want to see a credit boom as we did back then.

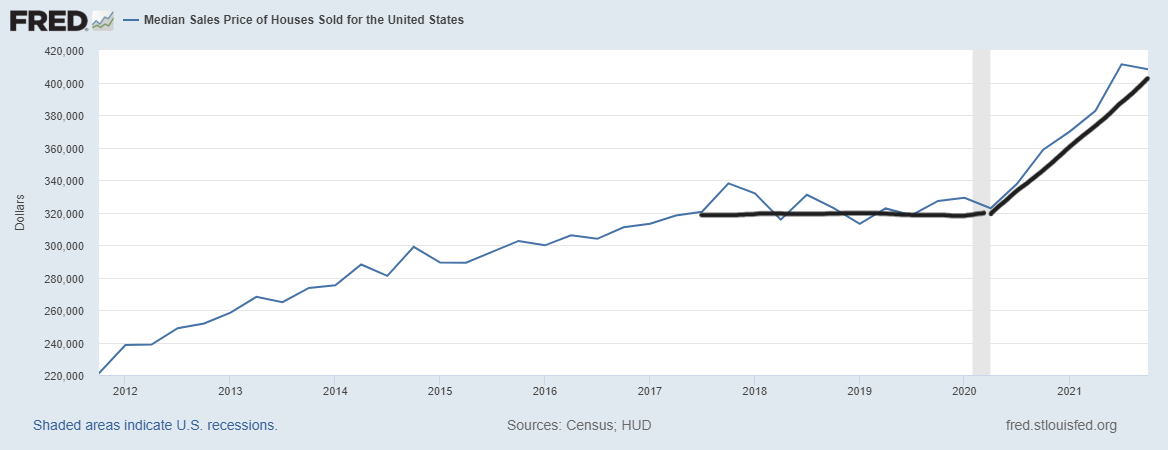

Now for some good news, growth of the median sales price has slowed down!

My biggest concern for housing in the years 2020-2024 was about home prices having the capacity to overheat in the existing home sales market. Here on the new home sales side of the equation, it’s all about pricing power and profit margins. The builders had the ability to push higher prices on the consumers as the demand was there. So for all the complaints about labor and lumber costs, the builders sold their homes at higher prices and made good money off them. This is also a factor why I don’t believe in the housing construction boom premise, because when builders and sellers have pricing power they push it to the limits.

From Census: The median sales price of new houses sold in December 2021 was $377,700. The average sales price was $457,300.

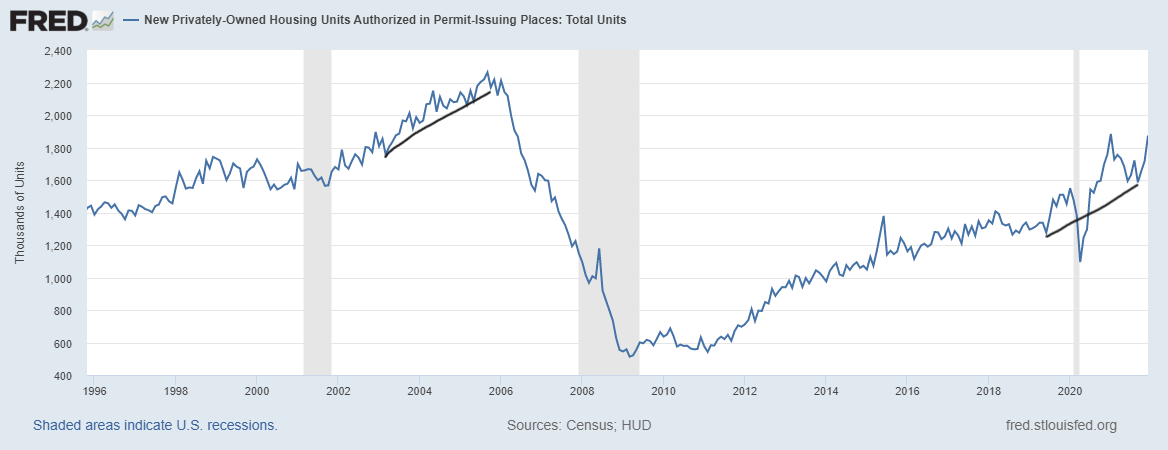

Even though the recent builder survey saw a slight drop, it picked up over the last few months of 2021, so the builders were feeling a bit perkier and sales rose, as well as permits. I believe some of the marketing that housing was going to crash in the second half of 2021 didn’t end well because simply rates are too low and demographic demand is too big.

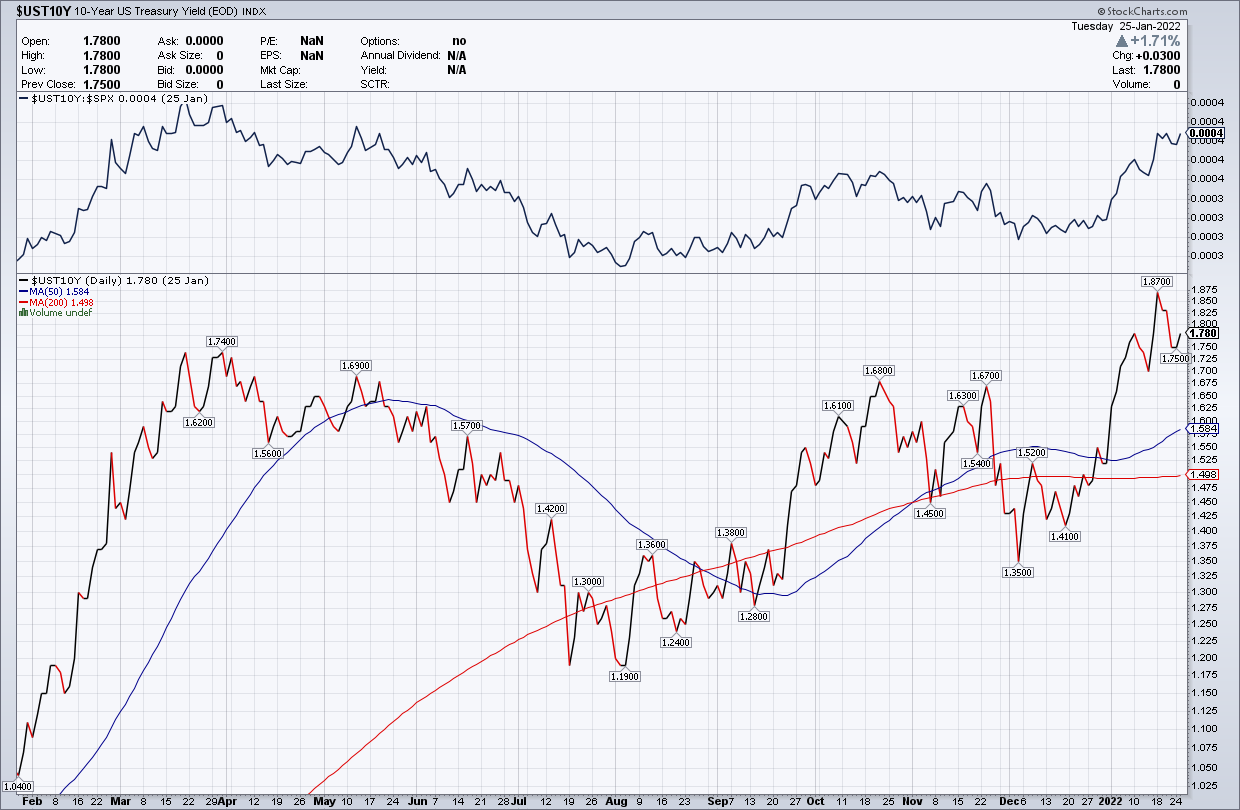

Now the pressing question is: What will the 10-year yield do? I believe, as I have since the summer of 2020, if you want housing to cool down you need the 10-year yield to break above 1.94% and head much higher with duration. Of course, this is something that hasn’t happened since the second half of 2019 after the inverted yield curve. That cooling process is to allow days on market to grow and create a balance for the existing home sales market.

Unlike last year, where I didn’t even address the possibility of that happening, for 2022 I have talked about how bond yields could rise above 1.94%, but we would need global yields to rise with it. From my article last week: “For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.”

Germany and Japan’s 10-year yields have been rising lately, but still not enough yet to get our 10-year yield to even really test the 1.94% level just yet.

Higher bond yields and higher mortgage rates really impact the new home sales market more than the existing home sales market. So, if the 10-year yield closes above 1.94% and heads toward 2.42%, creating 4% plus mortgage rates, the first sector you want to keep an eye on is the new home sales sector.

Today’s headline number beat surprised a lot of people, but the revisions to previous sales have been negative (see here for that déjà vu). On top of negative revisions, it is still taking too long to complete a new home in America. The builder has passed on a lot of costs onto the consumer, so they will be mindful of that 10-year yield as well.