Recent changes in long-term metrics could indicate that the reverse mortgage market is charting a path for borrowers toward higher loan proceeds. This is according to data compiled and provided to RMD by industry expert and VP of Organizational Development at Finance of America Reverse Dan Hultquist.

“Many in the reverse mortgage industry focus on production numbers, but very few understand all of the forces that impact industry-wide trends,” Hultquist tells RMD in an email. “I don’t claim to understand all of those factors either, but an often overlooked influencer is long-term interest rates.”

The way it works

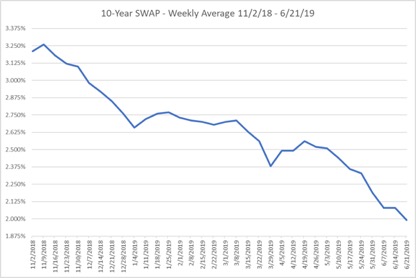

The calculation of a borrower’s expected interest rate is not calculated via short-term metrics like the one-month or one-year LIBOR index, but instead by the previous week’s average of the 10-Year LIBOR SWAP rate.

“For LIBOR-Based HECMs, the lender must use the average of the previous week’s daily 10-Year LIBOR SWAP figures,” Hultquist says. “We simply call this the 10-year SWAP average.”

When expected rates round down to the next 1/8th percent, borrowers qualify for higher principal limits, Hultquist explains.

“In addition, HUD allows a float-down at closing,” Hultquist says. “This helps borrowers get an additional bump in principal limit when SWAP rates drop. In essence, the effective SWAP rate on the day of application or closing can have a dramatic impact on the borrower’s proceeds [available].”

For those of average borrower age (currently 73 years old) and home value ($330,000), every 1/8th percent change will alter a prospect’s principal limit by approximately $2,300-$2,700 depending on the chosen lender margin, he says. While that may not seem like much, the magnitude of the change needs to be considered, Hultquist says.

Current trends

Because the 10-year SWAP rate has been declining steadily since the winter holidays, factoring in rounding has led the trend to result in higher principal limits in three of the past four weeks, Hultquist says.

“That alone is great news and should offer encouragement for dedicated loan originators looking to increase their volume,” Hultquist says. Looking at the data since November also could point to a coming increase in principal limits through the remainder of the summer.

“I don’t want loan originators to miss this opportunity,” Hultquist tells RMD. “Traditional loan originators naturally know how to take advantage of rate decreases. But reverse specialists tend to be hyper-focused on regulatory changes and often fail to recognize an economic ‘gift’ when it comes along.”

A summer opportunity

Because the weekly SWAP average peaked at 3.26 percent for the week ending November 9, 2018, comparing those with more recent figures draws a stark comparison.

“Last week’s average through Thursday, June 20th was 1.99 percent,” Hultquist explains. “That is a whopping decrease of 127 basis points (1.27 percent). Using a 2 percent lender margin, with the same borrower age (73) and home value ($330k), a prospect today qualifies for $23,100 more than they did prior to the 2018 holiday season.”

Such an increase in principal limits has the potential to result in an increase in reverse mortgage volume over the summer, Hultquist explains, but loan officers need to connect with their leads to make that possibility a reality.

“I think it can [increase summer volume],” he says. “But originators need to follow-up with prospects that were either short-to-close or less interested in their net figures when rates were high.”