It’s been an eventful fiscal year for the reverse mortgage industry.

Stemming from the Home Equity Conversion Mortgage program changes last October, the last 12 months have brought lower origination volume, proprietary product innovation, originator diversification, and — most recently — changes to the HECM appraisal process.

When last year’s HECM changes hit — with their lower principal limit factors and higher initial mortgage insurance premiums — industry experts had many predictions for the future. Now, one year later, Reverse Mortgage Daily is asking active reverse mortgage professionals if reality has met those expectations as we enter the federal government’s fiscal 2019.

“Both the industry and the consumer have been slow to adapt to the new HECM. But I believe part of the problem is the limited way the HECM product is viewed. Essentially, people see the HECM closing as a one-time exchange – the homeowner pays fees, and in return the homeowner gets to access a fraction of their home’s value. If that’s all you see, then obviously increasing the upfront fees and reducing the funds is a lose-lose proposition. What many fail to recognize is that the long-term costs for the client went down significantly. When we sell this as a long-term strategy for aging in place instead of an exchange, the changes become less significant.” — Dan Hultquist, Vice President of Education and Organizational Development, Live Well Financial

“The changes in the HECM program a year ago continue to leave the reverse mortgage industry with extreme challenges. The sales process is more important than ever to help explain to potential borrowers why the benefits of tapping home equity for a reverse mortgage more than offset the higher up-front cost for most planning-based borrowers. Needs-based borrowers suffer from the lower available principal limits, making it harder to qualify some borrowers for the product. Not all of the decreased volume is due to policy changes though — higher interest would have reduced potential borrowing limits even with no changes in the HECM program. As well, an important side effect of reduced government lending has been the growth in the proprietary reverse mortgage program. In the future, proprietary programs will offer many more options for reverse mortgage borrowers.” — Chris Mayer, CEO, Longbridge Financial, LLC

“Last year I took to calling the looming October 4 guideline changes “The dictate which will live in infamy,” as I anticipated a very difficult season ahead. Due to lower PLFs, this past year has indeed been quite tough, as I have had more turndowns than at any time in my career. The market only now seems to be righting itself.” — Laurie MacNaughton, Reverse Mortgage Consultant, Atlantic Coast Mortgage

“Mostly, reality does not differ from expectations. [In January], we stated there would be ‘market disruption and a volume drop in the short term.’ We knew margins would compress from competition and that has happened. My big disappointment is it took six extra months to confirm Brian Montgomery as FHA Commissioner — six months the industry needed to work with HUD on product enhancements and ‘back end’ servicing fixes to offset the impact of ML17-12.” — Michael McCully, Partner, New View Advisors LLC

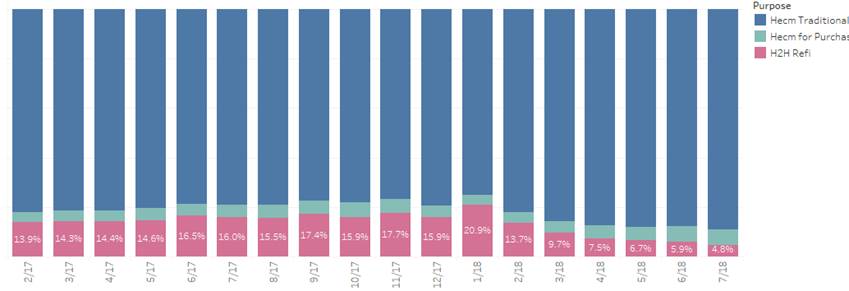

“The negative impact on volume caused by the 2017 PLF rollout is well-documented – we’re funding somewhere in the $300 million [range] in 2018 vs in the $500 million [range] in 2017. But there are a couple interesting positive takeaways when you put the data under a microscope. Positive takeaway #1: HECM to HECM refinance activity is way down. In 2017 we saw 14% to 18% of monthly production come from H2H refis. In 2018, we’ve seen H2H mix temper to around 5%. Positive takeaway #2: Prepay speeds have slowed considerably when we control for loan seasoning [how long ago the loan funded]. The vertical axis represents prepay speeds and the horizontal axis is loan seasoning. The light blue line below shows much higher prepay speeds in Q4 2017 compared to the speeds recorded in Q3 2018 [the dark blue line]. Slower speeds are a good thing for bond holders and HMBS issuers.” — Dan Ribler, Founder, Baseline Reverse

“My expectations for the HECM product this year were truly non-existent, meaning I did not know what to expect. Personally, I expected the first half of the year to most likely be slow. CHECK. I expected to have a lot of folks that would not qualify anymore. CHECK. I felt that there would be more folks that were unhappy with the amount of equity they would be receiving. CHECK. However, we have turned the corner and are getting more and more interest just like we do after every major change, and the rest of the year is looking up.” — Melinda Hipp, Branch Manager, Open Mortgage, LLC

“For my colleagues who have built professional referral patterns — advisors, builders, Realtors — the business is definitely back. After every cataclysmic change at FHA, lenders cram their pipelines with dangling loans to get them in under the wire. These bloated pipelines naturally divert attention from prospecting for new loans. Over time, though, those who build referral relationships get back on track. It amazes me how consistent the top performer list is year after year. Those who believe in their own agency in manufacturing referrals have the kinds of relationships that allow a thorough discussion of the changes and how, over time, the new HECM benefits both the consumer and the taxpayer.” — Shelley Giordano, Chair, Funding Longevity Taskforce at the American College of Financial Services

“1 — The revenue disruption from the lower floor has created a battle for being and choosing the low-cost provider – regardless of service or experience. It has also curtailed the ability to help borrowers using closing cost credits. 2 — The industry has pivoted from a mono-line product to a suite of proprietaries and a broadening definition, within companies, of serving clients with a variety of equity release options. 3 — Lower PLFs have excluded the lowest 10% [estimated] of eligible borrowers. Is that a harm [to the public] or a help to the [Mutual Mortgage Insurance] Fund?” — Brett Kirkpatrick, Partner, Harbor Mortgage Solutions, Inc.

“With the changes made last October to the lower PLFs, I expected fewer borrowers would qualify — and that is what has happened. Overcoming the costs objection has always been a hurdle; what most people don’t realize is the costs are comparable to a conventional mortgage, the difference being the IMIP. Because previously we had the flat 2% initial MIP, I had not thought that the change of raising for some but lowering for others would have the impact that it is having. But with the lower PLFs, it does make it harder to swallow the 2% MIP we had previously. At time of the changes, I had not thought about it, but am finding that people are choosing not to do the reverse mortgage because they receive so much less funds in comparison to the costs.” — Beth Paterson, Executive Vice President, Reverse Mortgages SIDAC

“1 — To say reverse mortgage volume is way down would be the understatement of the decade. 2 — For every one reverse mortgage I close, I close six to eight forward mortgages. 3 — I have developed a “blue ocean” business model and launched it in April of this year in order to keep my mortgage company profitable and growing. 4 – I started an internet television show that is NOT about mortgages to expand my brand and bring valuable information to boomers as they approach retirement. 5 – I am posting more videos on social media than I ever have and plan on expanding that form of soliciting business even more in the future.” — Michael Banner, President, Professional Mortgage Alliance, LLC

“I fully expected a personal and business loss of 40% after October 1, 2017, and this has come true, sadly. I think the industry has lost around 40% as well. This is in addition to lost business from other past HECM program changes — such as PLF cuts and financial assessment. Many loan officers have left smaller firms in search of a salary or some sort of more stable employment or switched to traditional loans. I also expected a lot of consolidation of LOs — LOs leaving this business — in 2018 and this has come true as well.” — Tim Linger, Owner, HECM Senior Home Financing

Written and Compiled by Maggie Callahan

{kind=link}

{kind=link}