Last week the Wall Street Journal published a story by Andrew Ackerman stating that the Biden administration wants to target nonbanks for tougher oversight and additional regulation.

The story states, “the Biden administration is laying the groundwork to target nonbank firms with stricter federal oversight as regulators grow concerned about financial threats from companies operating outside of the tightly supervised banking system.”

The article was striking to me because it was not long ago that members of a previous administration proposed defining nonbank mortgage lenders as a systemically important financial institution (SIFI) risk as a sector. The assumption was that if any were threatened with failure during a major credit event, that all would be equally susceptible to failure and thus labeling the collective entities in total as SIFI risks it would open up the ability to layer on significant regulation on all of them.

In fact, former FHFA Director Mark Calabria spoke of this in early 2020 stating, “Instead of focusing on specific entities, FSOC will shift to an activities-based approach, looking instead to the overall threats to financial stability. In other words, even if no particular nonbank is systemically important, FSOC could determine that an activity, such as nonbank servicing, is.“

The concern about nonbanks began following the Great Recession of 2008 and became exacerbated in the Obama administration as policymakers saw the rapid rise in market domination of the IMB (independent mortgage banker) and the similar de-emphasis of lending from the banking sector, especially in the Ginnie Mae programs.

The recent Wall Street Journal article only seems to reinforce the view that Calabria had in 2020 stating, “the aim would be to make it easier to label nonbank firms as systemically important financial institutions, or SIFIs, a designation that currently applies only to the nation’s largest banks and imposes extensive oversight in an effort to rein in risks to financial stability.”

This entire discussion should be extremely concerning to all in the mortgage industry, especially the IMBs. With the recent implosion of FTX, the Bitcoin exchange company, the focus on nonbanks has only increased and unfortunately the contagion of risk for increased regulation could threaten the entire nonbank sector. But we need to focus on the truths about IMBs versus all the other crypto, fintech, and new nonbanks in the market.

The fact is that the invaluable role that IMBs play is deserving of a counterattack to push back against the “throwing the baby out with the bath water” mentality that could be overtaking Washington. The Mortgage Bankers Association authored a valuable piece on IMBs that should be required reading for all policymakers as they consider trying to fix something that is simply not broken.

So here are a few key points:

- IMBs are not at all related to the FTX collapse. As a recent NPR article highlights, the FTX problem was perhaps more similar to what a run on a bank might produce stating, “FTX couldn’t meet the demand for withdrawals, and lawyers said that, in that moment of crisis, it became evident there were serious issues with FTX’s management.” Which highlights the second point.

- IMBs are not risk-taking entities. They do not have “balance sheets” that retain credit or interest rate risk in any meaningful way. IMBs generally serve as pass through entities that originate mortgages to be sold to any number of investors including Fannie and Freddie, bank portfolios, or sold into Ginnie Mae securities. Once that transaction is completed, nonbanks retain primarily two risks. Originators retain representation and warranty risk against fraud or misrepresentation, as well as processing errors that can result in a loan defect worthy of repurchase. This is a real risk but far more limited in the QM lending world of today. The other risk is only one that impacts nonbank servicers who could be stuck with making advances to Ginne Mae MBS holders if the borrower defaults until such time as the loan is pulled out of a pool. But even in this case, the risk is short-term liquidity. The servicer gets made whole by the FHA mortgage insurance once eligible to file a claim.

- Banks, on the other hand, are risk-taking institutions. They buy and hold a variety of assets representing multiple classes from residential mortgages, second mortgages, commercial loans, auto, credit card, student, lines of credit and more. In a credit event they pose far greater risk should the regulators fail in their oversight and this is why the OCC and other prudential regulators focus so much on this sector. In fact, if you think of major failures following the 2008 recession, aside from Lehman Brothers, you think of WAMU, Wachovia, Indy Mac, Bear Stearns, etc. In fact this list highlights the hundreds of bank failures post 2008. The differences in risk, particularly systemic risk (SIFI) is stark between risk-taking institutions versus pass through IMBs.

- IMBs, more importantly, are regulated. In fact some might argue that they are faced with more regulation than most other financial institutions. They have to pass the reviews and meet the capital, compliance, and safety standards of their investors, warehouse lenders, the GSEs, FHA, VA, USDA, and Ginnie Mae. They get audited by the CFPB. They are audited, generally annually, by every single state in which they operate. And on top of it all, multiple federal regulators play a role in overseeing them from the CFPB, to HUD, to FHFA.

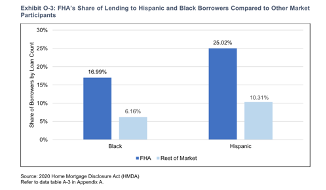

- And finally, there is this: IMBs are the entities insuring access to credit for millions of first-time homebuyers. As the Urban Institute points out in their quarterly chartbook, nonbank lending institutions are the ones offering lower credit scores to borrowers.

And with the FHA providing a significant majority of the mortgages made to African Americans and Hispanic homebuyers, the dependency on the IMB to fulfill HUD’s mission to serve these segments is simply critical.

While the banking sector generally backed away from the FHA program, IMBs not only fill that void, they have actually expanded the credit box from where it was when banks were the dominant player.

Look, it’s a shame that someone like me has to write a story to distinguish the IMB from being tainted by other nonbank players in the financial markets like the FTXs of the world.

It’s a shame that I have to clearly explain why banks should be regulated federally at a level different from the IMBs. But let’s not be so foolish as to think that the regulators know all this.

The only way to counter the views that existed in the Trump administration with Mark Calabria — and may exist today — is to fight back. This is not a time to make a passive argument. This is a time to use our voices.

The MBA wrote a great paper on this a few years ago and others like the CHLA and state associations have joined in. But we all need to get loud and get aggressive now. This is time to unite and roll up our collective sleeves and proactively engage.

David Stevens has held various positions in real estate finance, including serving as senior vice president of single family at Freddie Mac, executive vice president at Wells Fargo Home Mortgage, assistant secretary of Housing and FHA Commissioner, and CEO of the Mortgage Bankers Association.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.

To contact the author of this story:

Dave Stevens at [email protected]

To contact the editor responsible for this story:

Sarah Wheeler at [email protected]