A key challenge for the reverse mortgage industry continues to be the issue of product education, as many reverse mortgage professionals remain very concerned in reforming the industry’s education efforts to reach additional audiences of eligible, prospective borrowers. Additionally, 2020 saw a noticeable “cooling” of sentiment regarding private-label reverse mortgage products, visibly realized in disclosures of proprietary origination data and the measured perspectives of reverse mortgage industry professionals.

This is according to a recent 2021 Industry Outlook survey conducted by RMD by polling our industry readership about how they’re feeling about the business, and what they plan to focus on over the course of the next year. RMD recently presented the first part of its survey results, and are concluding our look at the survey’s findings here.

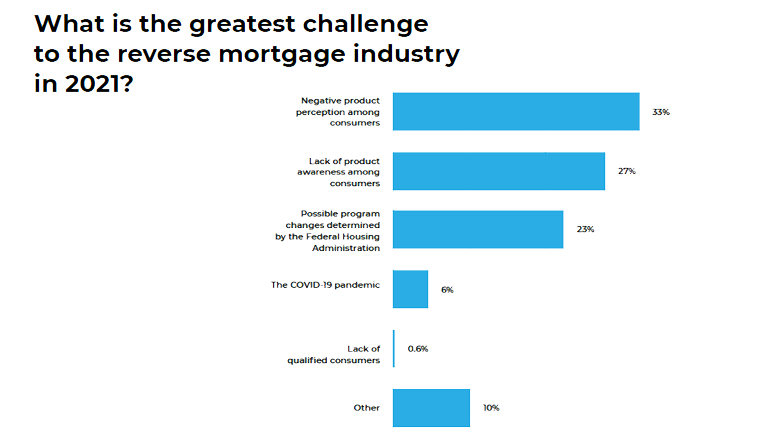

Product education as a key priority

The RMD Outlook survey was conducted online between November 11 and December 2, 2020, and asked reverse mortgage industry participants to share their insights on issues such as the anticipated impact of the COVID-19 pandemic on business operations into 2021; what the general business outlook for the upcoming year is for them; growth strategies they plan on observing in the new year; and the biggest potential opportunities and challenges are that they foresee for 2021.

Over 150 industry participants gave their insights for the survey’s results. With a concern in-line with the measured concerns of the industry in previous years, respondents for the 2021 Outlook Survey cited negative product product perception and lack of product awareness as the top two challenges they will face in 2021. When asked specifically about components that constitute the greatest challenges to the reverse mortgage industry in 2021, a combined 60% of the respondent pool named “negative product perception among consumers” (33%) and “lack of product awareness among consumers” (27%), respectively, as the top two challenges that the industry will face in 2021.

Less pressing a concern while still being relatively pronounced is “possible program changes determined by the Federal Housing Administration (FHA),” which clocked in at comprising 23% of industry respondents. The COVID-19 pandemic was also seen as a potential ongoing challenge the industry will continue to face according to 6% of respondents, while “a lack of qualified consumers” measured as the primary industry concern for just 0.6% of respondents.

Education and awareness remain key priorities for most major reverse mortgage lenders, as well. In a recent episode of The RMD Podcast, Finance of America Reverse (FAR)’s VP of Wholesale Lending Jonathan Scarpati described why education remains a key priority for FAR and the wider industry.

“Education is probably one of the most important [lessons] because regardless of what type of model you run, if you have a large forward division, a lot of that is going to be educating your forward originators about the benefits of a reverse mortgage,” he says. “To teach them when to be able to identify a potential reverse mortgage. [Asking if a client is] the right age, if they have enough equity, and just identifying that customer who could potentially get a reverse mortgage.”

Proprietary products cool down compared to 2020

2019 was a major year in terms of proprietary reverse mortgage product development and implementation, and that reflected in the Outlook Survey RMD performed as the industry headed into 2020. However, some new information the wider industry gained in mid-2020 coupled with the major interest gleaned for traditional Home Equity Conversion Mortgages (HECMs) as a result of the COVID-19 pandemic may have contributed to a slight cooling of perspectives on the potential importance of private-label products in 2021.

The perceived importance of these products is falling year-over-year, based on the results of the 2020 and 2021 surveys, respectively. Fewer than 40% of respondents indicated proprietary products are “very important” as the industry looks ahead to 2021, versus nearly 50% of respondents in 2020.

“There are about 3,400 conventional reverse mortgage originations (up from about 2,000 in the 2018 data) and 676 conventional reverse mortgage purchased loans reported, representing the niche non-HECM reverse mortgage products,” according to Home Mortgage Disclosure Act (HMDA) data released by the Consumer Financial Protection Bureau (CFPB) in August, 2020. The word “conventional” as used in the data is in reference to loans which are not sponsored, offered or secured by a government entity.

Data from the report detailing the calendar year origination of HECM loans previously placed the 2019 origination figure at 34,800, indicating that proprietary originations make up approximately 9.7% of the total figure of HECM originations in calendar 2019, based on the HMDA data. Nearly 40% of respondents indicate their company’s loan volume comprises less than 10% proprietary loans, which is in-line with the number related by the CFPB HMDA data.

Still, this is not to say that proprietary reverse mortgages are without importance. 38% of respondents still believe that proprietary reverse mortgages will be “very important” to the future of the reverse mortgage industry. More than a quarter report proprietary volume of 10% to 20%. The vast majority (85%) of respondents believe proprietary products are either “somewhat” or “very” important to the reverse mortgage industry in 2021.

Download the full results of RMD’s 2021 Outlook Survey.