An op-ed I wrote that appeared recently in HousingWire on the nature of nonbank mortgage company risks and Ginnie Mae’s proposal to impose risk-based capital and liquidity requirements on their issuers highlighted nonbank lighter safety and soundness regulation as a concern for generally higher risk profiles of these firms relative to depositories.

In light of this important industry and policy topic, I thought it instructive to provide further insight into the arguments raised from that previous piece.

In a comprehensive study of mortgage market liquidity, Liquidity Crises in the Mortgage Market, several well-known academics provided compelling evidence for “liquidity vulnerabilities associated with nonbanks.” In their study, these researchers examined the 2008 financial crisis and its impact on nonbank liquidity. They found that: “of the 19 nonbanks and depositories that funded their originations using both warehouse lines and SIVs in the precrisis period, only two, Nationstar Mortgage and Suntrust, survived until 2017.” They further state:

“The collapse of the short-term funding structure of nonbanks and some depositories, such as Countrywide Financial, led to rapid losses in liquidity and lending activity. Many of these firms experienced bankruptcies and closures similar to that of New Century.”

Suffice it to say that not much has changed in terms of the liquidity risk potential of nonbank mortgage companies since that time. Denials that these institutions do not pose relatively greater risk to the mortgage industry at some point in the future than depositories, reminds me — having started my career off during the S&L crisis with the thrift industry’s regulator and ending it during the 2008 financial crisis at Citigroup heading up risk for their North America consumer division — that memories tend to fade regarding the details of past crises.

The CFPB has mortgage servicers in its crosshairs – Is your subservicer compliant?

If they stay true to their word, the CFPB will come knocking on the doors of many mortgage servicers this year. Compliance always matters, but in the age of COVID-19, it matters tenfold. This white paper will cover strategies for compliant subservicing.

Presented by: Equifax

Another major risk of nonbank originators and servicers is operational risk in terms of loan manufacturing quality. In a study I conducted for the MBA’s Research Institute for Housing America I analyzed the impact of loan manufacturing quality on credit loss and its implications for the industry. It is critical to understand how operational risks can be closely tied to other risks such as credit.

In my earlier op-ed, I referred to a statistical analysis finding that the risk of nonbanks was significantly higher than that of depositories, controlling for other risk factors. I applied a multivariate statistical analysis consistent with the one I used to develop the industry’s first FHA automated underwriting scorecard (known now as TOTAL), and the industry’s first VA scorecard during my tenure at Freddie Mac.

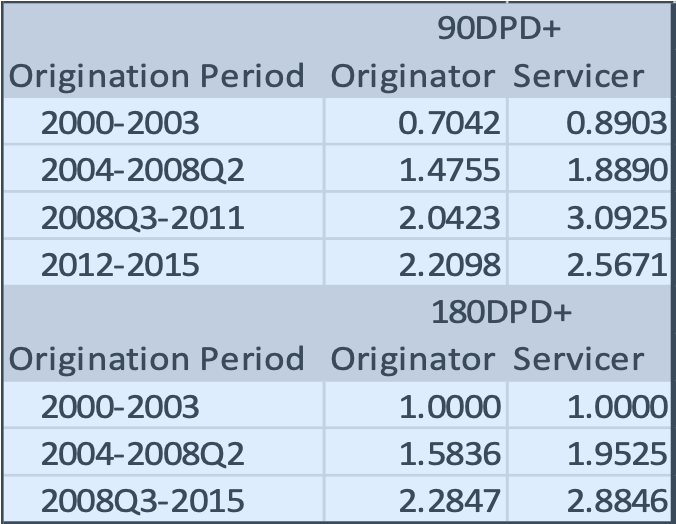

Far from being a back-of-the-napkin estimate of nonbank risk, it analytically controls for a host of factors such as borrower credit score, LTV, DTI and a dozen other factors to understand the credit risk profile of borrowers. The origination period of the analysis was 2000-2015 to allow for loan seasoning and two models were estimated: one with a definition of default as a loan becoming 90 days past due or worse, and the second a loan becoming 180 days past due or worse.

I segmented the time periods into four underwriting regimes based on a machine learning technique clustering loan performance based on origination year and quarter. These were 2000-2003, 2004-2008Q2, 2008Q3-2011, and 2012-2015. I created separate indicator variables for whether the loan was originated by a depository or nonbank and included them in the models along with the other variables of interest.

The overall models had a high level of discriminatory power on an out-of-sample basis (KS of 66 and 69 for the 90DPD+ and 180DPD+ models, respectively). A table of results from those models is found below showing the odds ratios (risk multipliers) from those indicator variables.

NonBank Risk Multipliers Compared to Depositories

The baseline or reference level (odds ratio =1) for each odds ratio is the default risk of mortgages originated by depositories between 2000-2003. Any odds ratio above 1 in the table indicates higher risk of nonbanks relative to the baseline. All estimated coefficients underlying the odds ratios were statistically significant at the 99% level with the exception of the 180DPD+ model results for the nonbank 2000-2003 period which were no different than the baseline. Note that for the 180DPD+ model the 2012-2015 period was collapsed with the 2008Q3-2011 period based on the machine learning results.

The results indicate that other than the 2000-2003 period, loans originated or serviced by nonbank institutions were riskier than depositories originating or servicing loans from 2000-2003. Specifically, the 1.9 risk multiplier I cited in the earlier piece was from a simpler version of this model.

The results are consistent with this analysis where for 2012-2015, loans originated by nonbanks were 2.2 times more likely to become 90DPD+ than depositories from a more normal underwriting period (2000-2003). Similar results (2.57 odds ratio) hold for nonbank servicers over the 2012-2015 period, which analytically corroborates a GAO’s study of nonbank mortgage servicers and their recommendation for greater regulatory oversight.

Specifically, they stated: “Banks and nonbank servicers are subject to different safety and soundness regulation and different capital rules. As a result, mortgage market participants and others have questioned the extent to which nonbank servicers may pose additional risk to consumers and the market and whether the existing oversight framework can ensure the safety and soundness of nonbank servicers.”

The primary takeaways are this: nonbanks by virtue of their business model and regulatory oversight pose greater liquidity and operational/credit risks than depository institutions all things considered.

Clifford Rossi is Professor-of-the Practice and Executive-in-Residence at the Robert H. Smith School of Business at the University of Maryland. He has 23 years of industry experience having held several C-level executive risk management roles at some of the largest financial institutions.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.

To contact the author of this story:

Clifford Rossi at [email protected]

To contact the editor responsible for this story:

Sarah Wheeler at [email protected]