The federally insured reverse mortgage known as a Home Equity Conversion Mortgage (HECM) is unique, as are the rates that impact the HECM product. For this reason, I will provide a short monthly educational focus, followed by a summary of the HECM rate market.

Keep in mind that almost all HECMs are adjustable-rate mortgages (ARMs), and so each rate update will concentrate on ARMs.

With a HECM loan, the U.S. Department of Housing and Urban Development (HUD) determines how much principal a lender can provide a borrower. This “principal limit” calculation is based on factors like home value, age, and of course, interest rates.

Why are there two HECM interest rates used with HECM loans?

- EXPECTED RATES

When calculating principal limits, HUD requires lenders to use long-term forecasted rates (tied to the 10-year Constant Maturity Treasury [CMT] rate). These are called “expected rates.”

- Purpose: Primarily used to calculate initial HECM principal limits

- Calculation: Margin + weekly average 10-year CMT

- Timing: Previous week’s average generally becomes effective Tuesday

When expected rates are higher at origination, borrowers qualify for less principal at closing. Conversely, when expected rates are lower at origination, borrowers are offered more principal.

- NOTE RATES

For calculating accrued interest and the growth of the principal limit after closing, HUD requires lenders to use short-term rates (generally tied to the 1-year CMT). These rates are called “note rates” or interest rates.

- Purpose: Primarily used to calculate interest accruals and principal limit growth

- Calculation: Margin + weekly average 1-year CMT

- Timing: Lender must use the average in effect 25 days prior to a rate change

When note rates rise after closing, borrowers have faster interest accrual and faster principal limit growth. Conversely, when note rates fall, borrowers have slower interest accrual and slower principal limit growth.

Ultimately, HUD requires us to use two rates because it is risky for the Federal Housing Administration (FHA, the insurer) to use short-term rates to calculate long-term borrowing capacity.

Imagine an extreme example where the 1-year CMT is 1% and the 10-year CMT is 6%. FHA would be nervous about providing high principal limits to borrowers with the assumption that current short-term rates will always remain at 1%.

March 2024 update

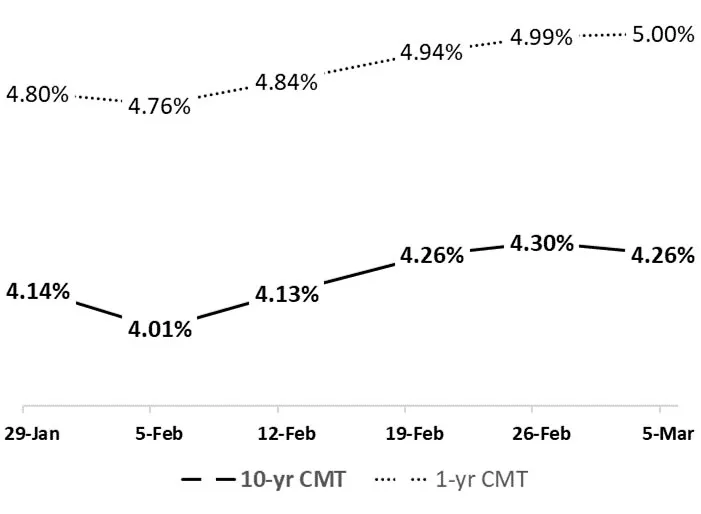

Early in February, we saw a lower weekly average 10-year CMT (4.01%). The rate in effect for March 5 is 25 basis points higher (4.26%). This has caused HECM principal limits to drop for new applications. The 1-year CMT also followed this upward trend as shown here:

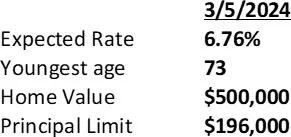

As an example, a 2.50% lender margin combined with a 4.26% 10-year CMT index would produce a HECM expected rate of 6.76%. Using this expected rate, a 73-year-old homeowner with a home that appraises for $500,000 would qualify for a principal limit of $196,000 as shown here:

For updated principal limit calculations like this, a loan originator can use a mobile app like RapidReverse or use any HECM loan origination system of their choice.

Note: 2.5% lender margins are used for education purposes only. Expected rates are rounded to the nearest 1/8% for calculating HECM principal limits. For calculating principal limits, 6.76% rounds to 6.75%.

This column does not necessarily reflect the opinion of Reverse Mortgage Daily and its owners.

To contact the author of this story: Dan Hultquist at [email protected]

To contact the editor responsible for this story: Chris Clow at [email protected]

Dan- Great explanation. You did fail to mention the ongoing MIP of .50% which is added to the note rate and affects the accrued interest by adding 1/2 point.

Thanks, Tom. Yes, we’ll discuss MIP in future monthly updates. Ongoing MIP impacts compounding and is recorded as accrued MIP (separated from accrued interest for tax reasons).