Last year, during the throes of COVID-19, I expended many words arguing that the U.S. economy would be OK despite the dark period we were in. We just needed patience. We aren’t in a housing bubble. Today we are enjoying the most remarkable comeback of the U.S. economy, which almost no one saw coming. The America is Back Economic Model and the 10-year yield should share the Oscar for best performance.

Favorable demographics have been a significant contributor to our rapid economic rebound, especially in the housing market. The U.S. economy was plugging along nicely before COVID-19, and the housing market was doing even better. The month before COVID-19 became a known entity in our country, demand for housing started to break out. Once COVID hit in earnest, many predicted that housing would crash.

Demand did take a pause — but that was brief. Inventory levels stayed stable, housing demand picked up after five weeks and mortgage rates went lower. Housing is a necessity — it’s not optional. Because of this, if we have the demographics for home buying, then we will have stable replacement demand. The only factor that changes this in a big way is if mortgage rates get too high. Since 1996, it’s been very rare to have existing home sales fall below 4 million in a month.

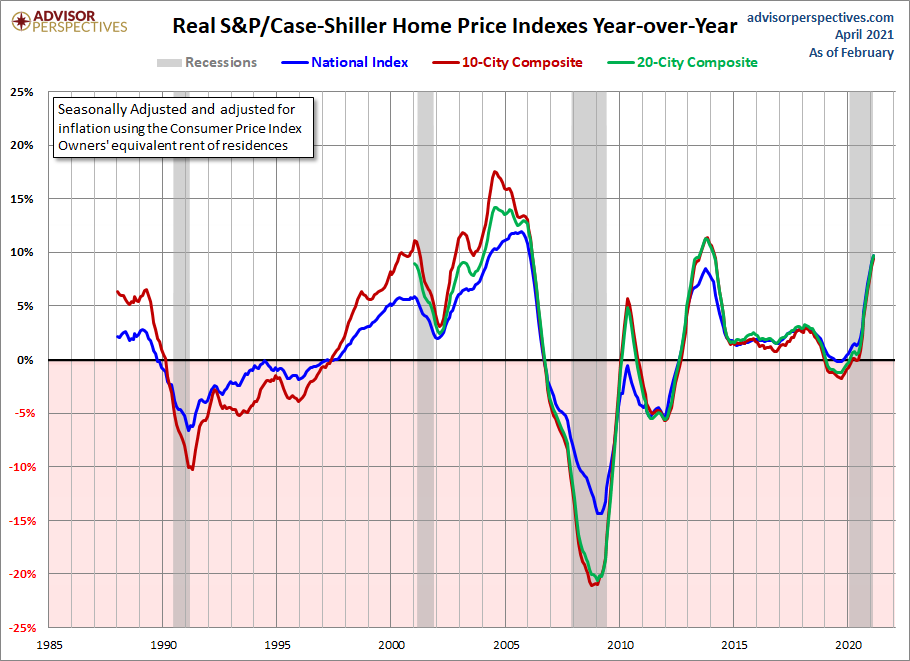

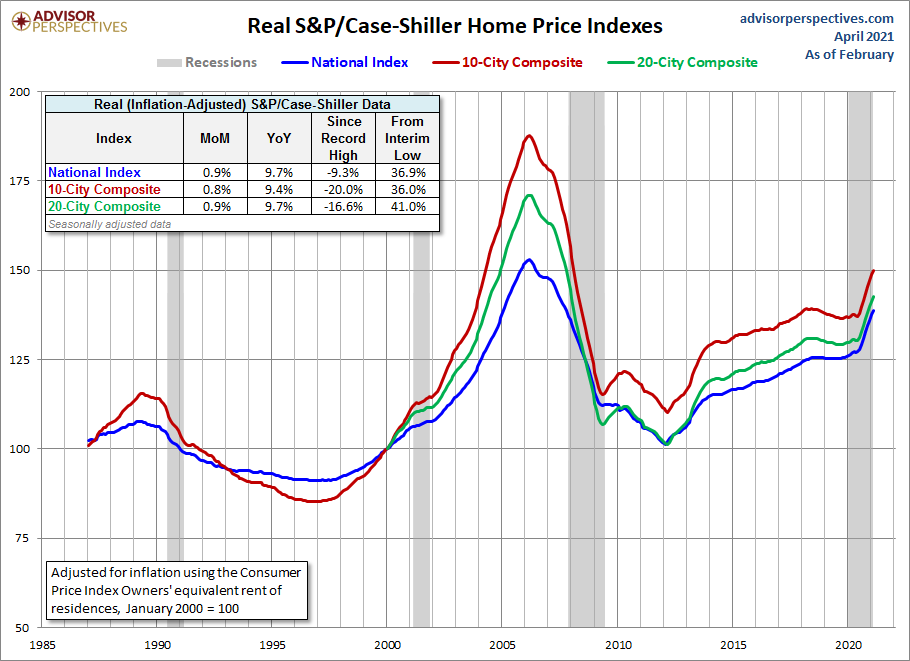

When you have the best housing demographic patch ever in history and the lowest mortgage rates in history, with housing tenure at 10 years, then we have to start worrying about home-price growth. All those factors are in play, and home prices are growing too fast. This was my main concern in the years 2020-2024, and that is being played out currently. Today the Case-Shiller index showed 12% home-price growth. For me, it’s always about real home-price growth, and this price index, as you can see, has gone parabolic now.

This is a big reason why recently on Bloomberg, I talked about how this is the most unhealthy housing market in a long time.

Granted, this is a first-world problem. Our would-be homebuyers make enough money to outbid each other on the limited number of homes available for purchase. This stressful, overheated marketplace is due to too much of a good thing. Too many qualified buyers are chasing after too little inventory. However, you have people saying homebuyers are overpaying for their homes and they will be in trouble soon. Uh, no!

This is why housing isn’t in a bubble, and that is the problem. These Americans who are outbidding others and getting the home are doing very well financially. I am not talking about cash buyers or investors. I am talking about primary resident mortgage homebuyers. They have enough home-buying power to win the house. The market is unhealthy because we shouldn’t be having this much competition for shelter, but it’s not speculation demand at all.

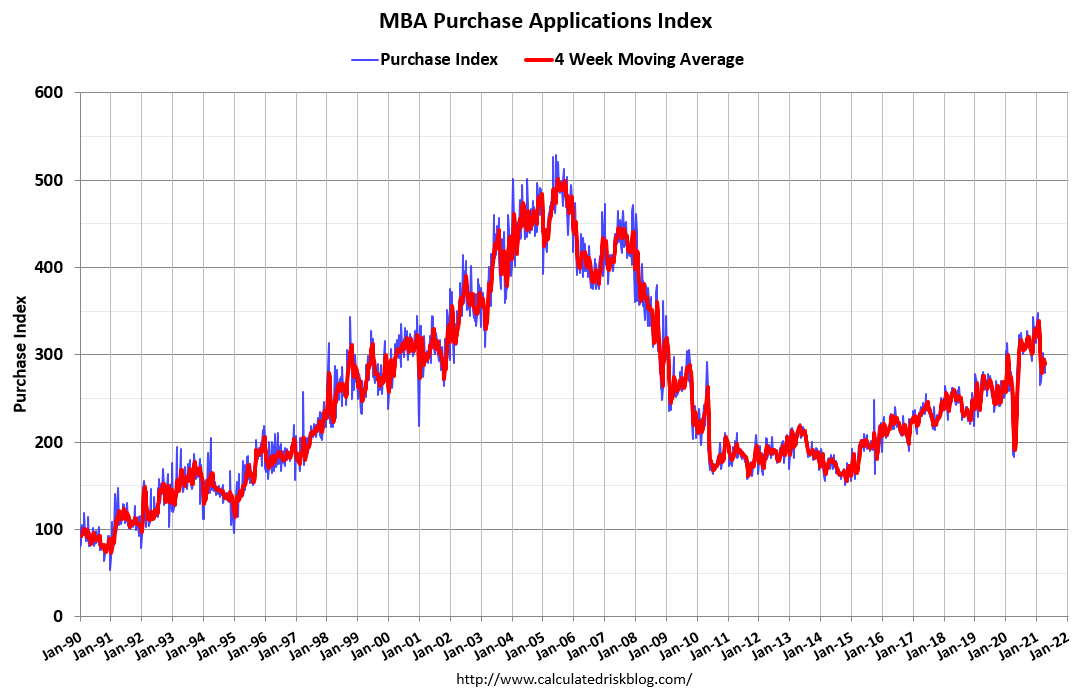

As always, I refer people to the purchase application data on this. 2018-2021 looks nothing like 2002-2005. If we make some proper COVID-19 adjustments to the data, we are up year over year, but barely.

Accelerating home prices is not a new thing. In 2013 we had a similar situation. Homes for purchase were receiving multiple bids over asking. Higher mortgage rates cooled things off. As a result, in 2014, purchase applications were trending negative 20% year over year. Higher mortgage rates were precisely what was needed to halt the unhealthy price growth. Nominal home prices didn’t go negative year over year, but the rate of growth stalled. The market did its job.

Before 2020, I thought that as long as nominal home price growth was 4.6% or less every year from 2020 to 2024 (which would mean peak 23% home price growth during these five years), we would be fortunate. The price gains we saw in 2020 and thus far in 2021 suggest that the dream of moderate home-price growth has been smashed.

What does this mean for the future? First and foremost, housing isn’t going to crash. For those wishing for a 50% “correction” to occur within a year, keep dreaming. This is especially true for 2020- 2021, when we have the best housing demographic patch in U.S. history with the lowest mortgage rates ever.

Unless we get higher mortgage rates to cool prices and allow for more days on the market, then home-price growth will continue on its upward trajectory. Home-price growth is sticky and hard to erase or backtrack with the high-velocity short term when demand is stable. I believe that housing isn’t in a sales boom, just a solid replacement buyer demographic patch in the years 2020-2024. Now I think we’re coming to an end of the deficient inventory levels, but this only cools down the price growth slightly.

We just had the quickest recession/recovery cycle ever and are on our way to a long economic expansion, barring any one-time, unexpected event. I can tell you that the silver tsunami that was supposed to occur in 2015 and every year since will (once again) not happen. The silver tsunami is the theory that a massive number of baby boomers will simultaneously decide to sell their homes and flood the market with inventory causing prices to drop. That’s not going to happen.

What could increase inventory?

Here are a few things that could happen to increase inventory:

– Higher mortgage rates

-Mom-and-pop investor landlords decide to sell their rental properties because they want out after their COVID-19 experience.

– Work-from-home model becomes more widely adopted. Since this is a new variable, this would be a reason to sell and move somewhere cheaper

We can hope that any or all of the above will facilitate an increase in inventory and a much-needed cooling of home prices from this torrid level. Home-price growth like this just eats into future affordability levels. I wasn’t too afraid of this before 2020 because the 10-year yield always stayed in a range between 1.60%-3%, and mortgage rates over 4% kept a lid on home-price growth.

That isn’t the case anymore. COVID-19 has created chaos in the bond market and rates and is not a positive for the existing home sales marketplace regarding controlling home price growth. In short, we have solid economic data without the 10-year yield breaking over 2%. 2021 should be the peak rate of growth year too.

When trying to gauge demand in the coming months, don’t be confused by the negative year-over-year prints for purchase applications for the second half of 2021. This is due to high comps from the recovery last year. When demand gets softer, we will see real natural declines or flat growth yearly.

People have already forgotten that real home prices were negative in 2019, although nominal prices did not go negative and total home sales were near 6 million. Mortgage rates were higher (4.75% to 5% back then), and we now have better demographics for home-buying. If real home prices go negative, the market will be fine, especially considering the recent rapid growth. We have lots of room for the price growth rate to fall and not worry about a home sales collapse.

The number of cash buyers and investors in the market hasn’t deviated too much from the norms in the past few years, and we have no speculation credit demand. This means demand is healthy but not booming. Last year, I talked about what would happen when the 10-year yield crossed 1.94%. This should bring mortgage rates to 3.75% or higher, which would knock some would-be homebuyers out of the market and cool prices. Slowing in the rate of growth in home prices is a positive, not a negative, for the market.

Americans buy homes to live in, and the price they are willing to pay depends on their capacity to own the debt. It does not rely on the Case-Shiller index breaking below 200 moving average so they can buy on a dip. Homebuyers don’t think like stock traders. Don’t get housing advice from stock traders looking to buy the dip. Millions of Americans purchased homes during a pandemic because they want somewhere to live, and they could do so.

More homes have been purchased in 2020 and 2021 than in any single year from 2008-2019. The reason is that mother demographics is a powerful economic force. She doesn’t care about podcast stock traders or crash cult YouTube real estate sites.

To reiterate, people buy homes to live in. Once the rate of home-price growth slows, don’t be tempted to start listening to those perpetually wrong housing bubble boys who have been predicting a crash since 2012. Some people always want to ice skate uphill, and that’s their prerogative, but you don’t have to listen to them while they do it.

Logan, I love reading your analysis. From 2016-2018 I taught a 2 hour class Denver RE Agents titled, “Is the Denver RE Market in a Bubble?” as the talk of a bubble in Denver started at end of 2015. Back then we had 2 months of inventory, now we have 9 days.

What we have is first and foremost is a SUPPLY PROBLEM! We need home builders to increase production by at least 50% nationally and probably 100% in Denver to ever solve this problem. I don’t think this will ever happen. Why? People have been fleeing the trades since 2008 and not enough new young people are choosing to work in the trades. Why?

Our country’s education policy for the last 30 years has been–send every kid to college and programs that introduced kids to blue collar work disappeared in our high schools. Thus, millions of kids went to college every year and got degrees in philosophy and other “arts” degrees that are basically worthless in the workforce.

Finally, combine our education policy with our nation’s cultural perception and value of blue-collar workers as seen in Hollywood, in which men who are blue-collar workers are ridiculed and shamed for being “losers”. I would ask in my Bubble class this question–“What was the last TV show that portrayed blue-collar workers in a positive light?” The answer everyone came to was Home Improvement.

People have been fleeing the trades since 2008, and not enough new young people are choosing to work in the trades.

I never found this to be a valid thesis. We used to build a lot more homes with a lot fewer construction workers decades ago.

In fact, I called it the Ghost theory of the lack of labor for construction a few years ago. New home sales just had their weakest recovery every from the years 2008-2019. The builders don’t oversupply a market post-1996

Charts in this article to prove my thesis.

https://loganmohtashami.com/2017/10/31/ghost-theory-the-lack-of-labor-for-construction/

Along with the indicators Mr. Mohtashami discusses, I like to watch the relationship between the monthly cost of home ownership to household income. In the new-home arena, I have seen cases in the past where price resistance trumps demand and new home sales begin to slow.