We’ve all been wondering what 5% plus mortgage rates would do to the hot housing market, and now we’ve got that and a bag of chips. This topic is something very near and dear to my heart because going back to the summer of 2020, I have said that one of the only factors that could cool down the housing market was the 10-year yield getting over 1.94%, which would result in higher mortgage rates.

The home-price growth from 2020 through 2022 has been so unhealthy that I’ve labeled this a savagely unhealthy housing market as inventory has once again collapsed on a year-over-year basis in 2022. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housing market.

Have higher rates worked? It’s still early to see the full effects, but here’s what we can tell from current data.

What higher rates should accomplish

The goal of higher rates, in my view, is to cool down price growth and get more days on the market. A few key data lines can tell us if we are heading in that direction.

We are still seeing numbers in the teens for days on market, which isn’t good. We would like to get this back to 30 days, but anything in the 20s is a victory. Inventory falling again in 2022 created more forced bidding wars, which frustrates buyers, keeps potential sellers from wanting to list, and creates stress for real estate agents doing a lot of work with nothing to show for it. In addition, the Federal Reserve isn’t comfortable with home prices going up every year.

This is a first-world problem compared to a housing bubble, a credit boom, and a crash, but a problem nonetheless. Some data to consider:

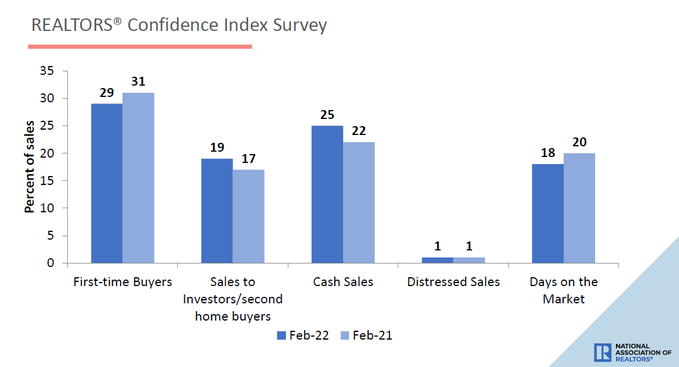

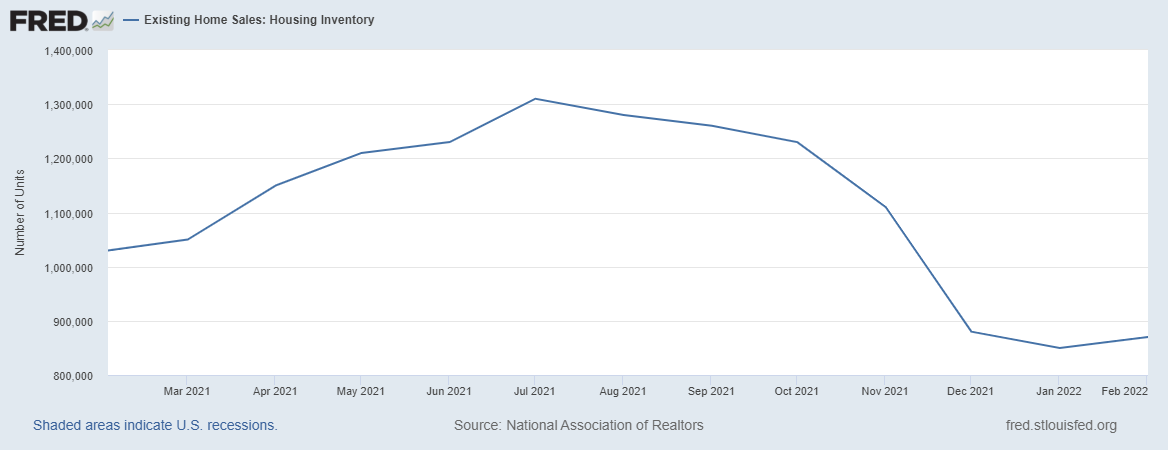

1. In NAR‘s most recent existing-home sales report, as you can see below, the days on market is still at a teenager level. We need our housing market to go to college and find a room to rent in their 20s.

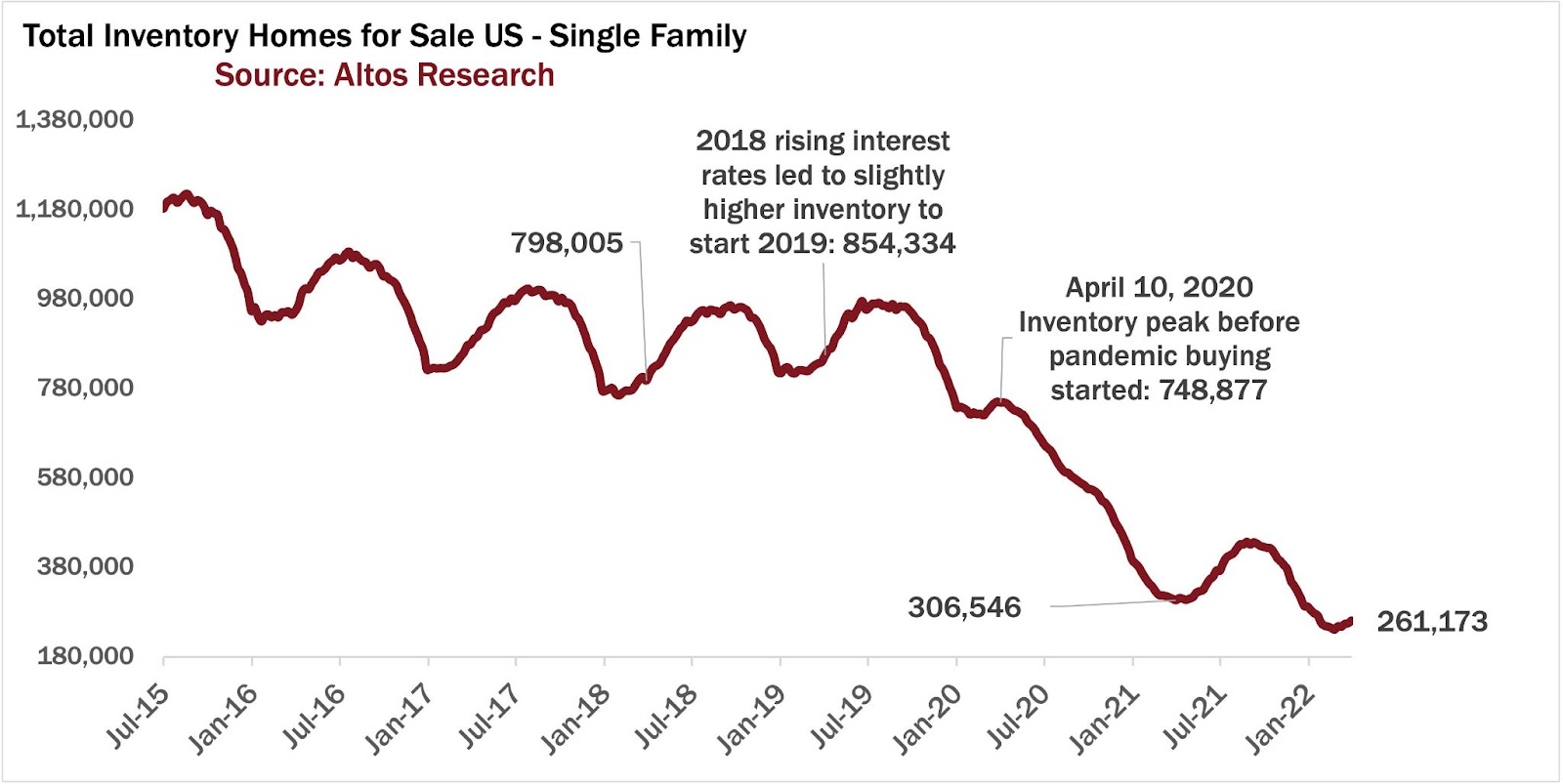

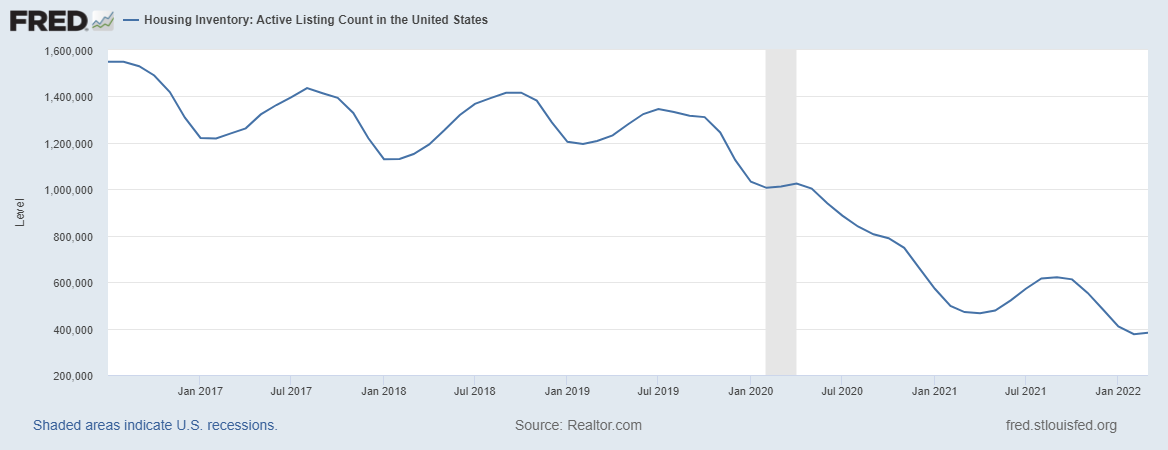

2. Inventory is still showing negative year-over-year data. Even this week, on tax day, it is still showing a decline. However, the year-over-year declines are getting less. We went from a 30% year-over-year decline at the end of 2021 to just a negative year-over-year decrease of 14.8%. I find this to be a very positive trend because the No. 1 goal for me is to see inventory have some positive prints, and we are at least heading in the right direction

From Altos Research:

Are higher rates working now?

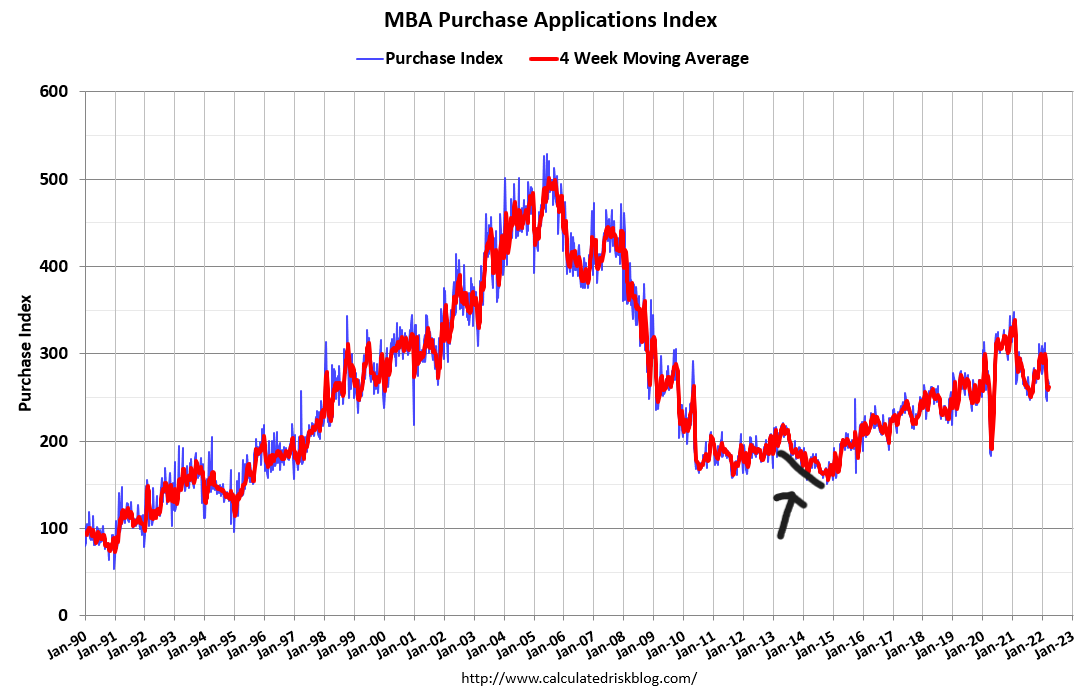

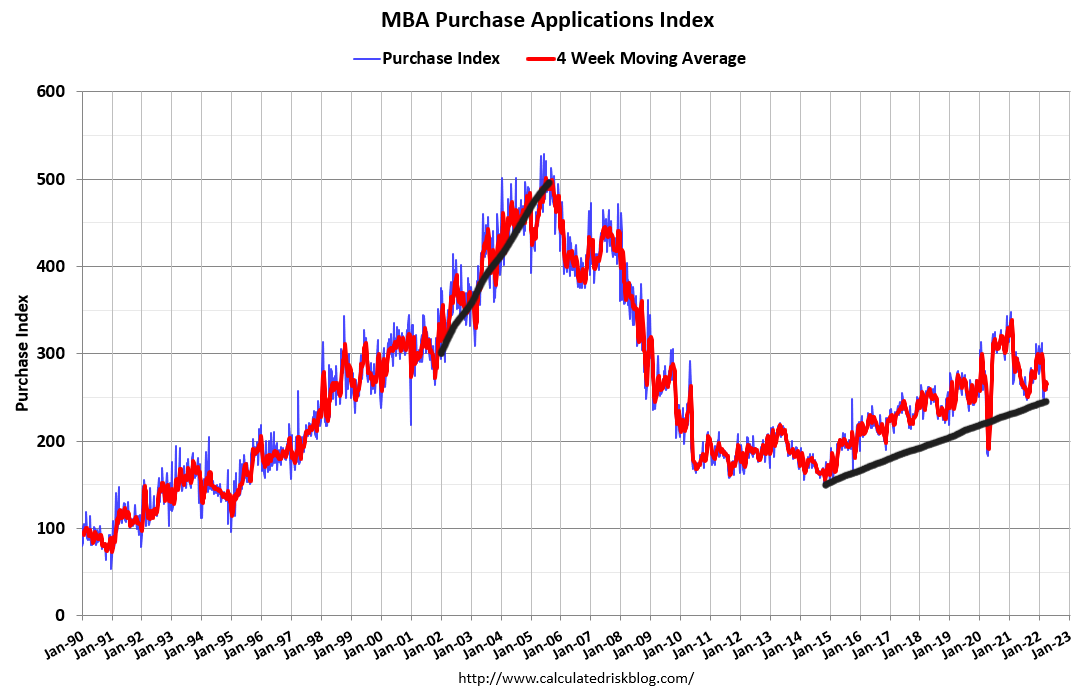

So how can we tell if higher rates are doing their job and we can achieve the goals above? Purchase application data has always been an excellent way to understand how the markets work. It’s also a bit of a funky data line if you don’t have experience reading it.

Historically, this data line is instrumental in tracking the year-over-year data from the second week of January to the first week of May. Typically after May, volumes fall! COVID-19 has wrecked the comps for many economic data lines, so COVID-19 adjustments need to be made. Considering that, what do we know so far?

I would say that we are seeing legit softness so far in 2022, but nothing too dramatic. The last time this data line was fragile was back in 2013-2014. Mortgage rates shot over 4% quickly, and it created a negative year-over-year trend in 2013-2014. The 2014 data showed a 20% year-over-year decline trend and sales fell that year.

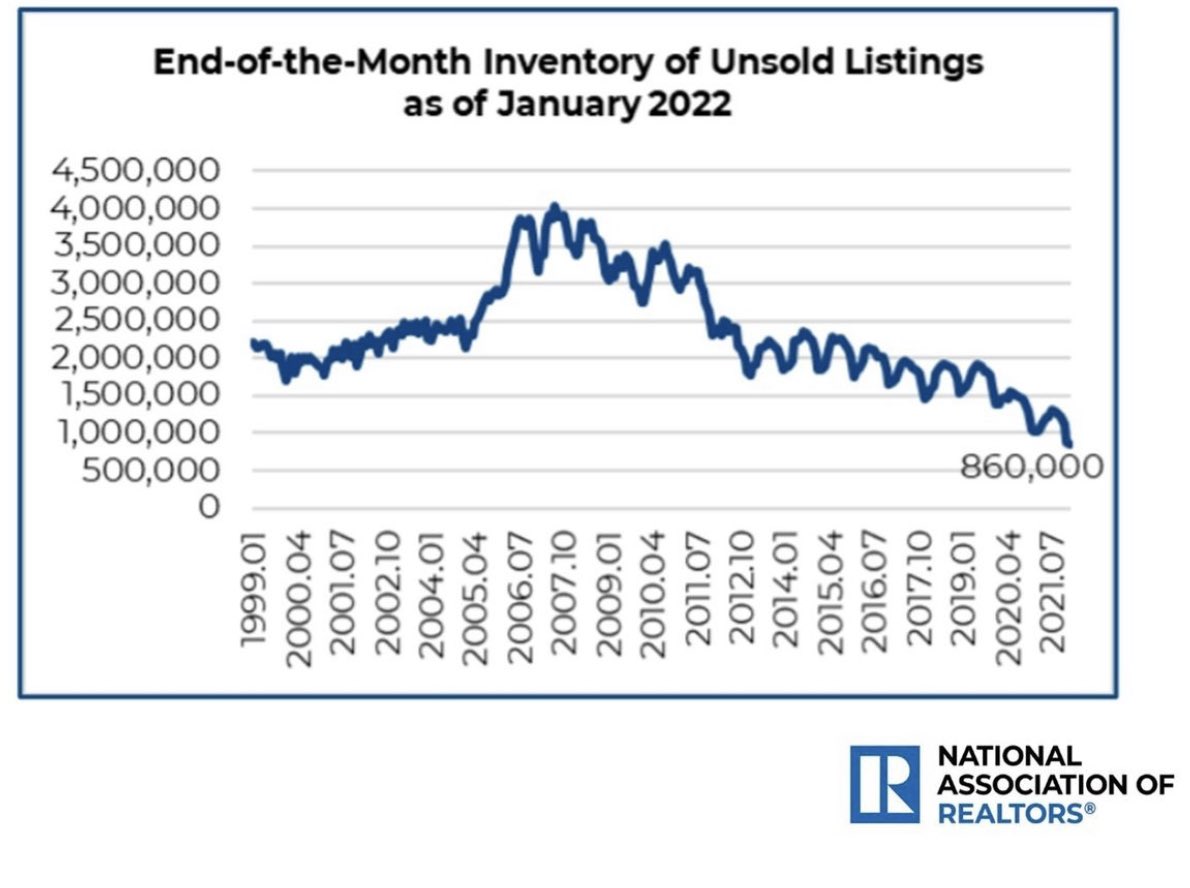

2014 was the very last year total housing inventory grew in America. It wasn’t a lot of inventory, but still, weakness in demand created more homes on the market. My ultimate goal for housing inventory is to get back into a range between 1.52 – 1.93 million. Historically, that is considered low inventory, but that is a much more sane marketplace than what we have currently.

2018 was the last time mortgage rates got to 5%, and sales trended from 5.72 million at the end of 2017 to 4.98 million in January of 2019. Inventory didn’t grow that year and purchase application data only had three negative prints year over year, and they were mild too.

That is a good reference to look at, so let’s move toward 2022 because it’s much different now. Sales are working from a higher level and price growth has been hotter, but inventory is much lower this year than any period in history, and demographics are solid in America.

Three points to focus on

1. Week-to-week data the last three weeks have had two positive prints and one negative — so that’s not much either way. Three weeks ago, we had a positive 1% print, two weeks ago a negative 3% print, and this week 1% growth. I am not a big fan of reading week-to-week data unless we are considering them within some short-term event like COVID-19 or spiking mortgage rates.

2. COVID-19 created very high comps in this data, so it’s been negative year over year since June of 2021. Unless you make COVID-19 adjustments, you’ll get confused with this data line. I believe many people did this last year because the data showed negative data for the second half of 2021, but if you made those adjustments, you could have seen that the data was getting better toward the end of the year.

Purchase application data showed meaningful increases from October to December, which was why existing home sales got to a high-level sales print of 6.5 million in January this year. I still believe that number had some December sales closed in January that made it look high.

3. Focus on the year-over-year data and remember that percent increases or decreases aren’t an exact science compared to sales. Look at this data line as a trend survey, and you need big moves to see a material change. If housing was doing great or crashing, we would need to see activities 20%-30% up or down. This can amount to just a couple of hundred thousand home sales for the existing home sales market up or down.

If you’re looking for a significant macro trend change, positive or negative, single-digit gains or losses aren’t that meaningful in the enormous macro sense for the existing home sales market.

Here are some examples. When COVID-19 created a pause in home buying, the worst four-week year-over-year declines looked like this: -24%, -33%, -35%, -31%

When we saw make-up demand after the COVID-19 paused, the data looked like this: +33%, 27%, 22%, and 22%.

We want to forget the year-over-year comps in 2021 using the crazy 2020 data, so I won’t even bother showing you those data lines.

2022 Data

Now let’s take a look at 2022! What have we learned from this year’s purchase application data? As you can see below, the housing market from 2018 to 2022 doesn’t look like anything we saw from 2002 to 2005.

If I didn’t know mortgage rates had passed 5%, I would be saying the same thing with the purchase application data all year long: not too much is happening, but some softness for sure. However, since mortgage rates got above 5%, I have been keen to see if the data has broken toward a more aggressive negative direction. So far, that hasn’t happened.

I believe I can stop using the make-up demand comps to compare the year-over-year data after mid-February. So with that adjustment, this is what I am seeing over the last four weeks, starting from 4 weeks ago: -12%, -10%, -9% and -6% year over year.

The year-over-year declines have been falling; some are due to more reasonable comps. This week -6% is the smallest year-over-year decline for the year. The four-week average is running at 9.25%.

2022 is shaping up to be the first legit year of negative year-over-year declines in purchase application data since 2014. The 2018 market, which had to deal with higher rates, was primarily positive every week except for three weeks. So, for sure, we have some softness in 2022 after making some proper adjustments, but the softness in the data is mild so far.

I had anticipated more substantial year-over-year decline numbers than this, and so far, nothing. I often mention on social media that higher rates need duration to work themselves in the housing data for the existing home sales marketplace. It can be quicker to see the results in the new home sales market because there isn’t a homeowner factor in that equation.

When we see a weakness in the housing data, it should create more days on the market. The real goal is to stop the downtrend in inventory over the past few years.

Again, I am a man who believes in balance and what we have in housing right now is savagely unhealthy. My 23% home-price growth model for 2020-2024 has already been smashed and we are heading for 35%-40% cumulative home-price growth in thee years, which is not a good thing in my book.

Purchase application data is seasonal, and total volumes typically fall after May. We will see if we get some more buyers with the seasonal rise in inventory every year. We saw this happen last year.

However, mortgage rates being at 3% is much different than mortgage rates at 5%. Hopefully, we can balance the housing market with these higher rates. In the summer of 2020, I wrote that a 10-year yield over 1.94% could cool down housing, but that was before the significant price-growth run we’ve seen in America.

However, we are here now, and hopefully, we don’t start 2023 at fresh new all-time lows because a balanced housing market is the best housing market.