Think of the markets as capitalist soothsayers. They do not abide by partisan politics, social mores or ethics. They do not care who is president. The markets react to what has the potential to make money for companies, good or bad, and what has the potential to prevent companies from making money. Also, whether they believe there will be economic and housing market growth.

This is why even though we have suffered great drama in the past week, the markets didn’t blink. Consider:

- Hospitalizations due to COVID-19 are at seven-day average record highs;

- COVID-19 deaths are at seven-day average record highs;

- The U.S. capital was under siege while congressional members were in chambers;

- And the U.S. jobs report was negative 140,000 jobs for the first time since April.

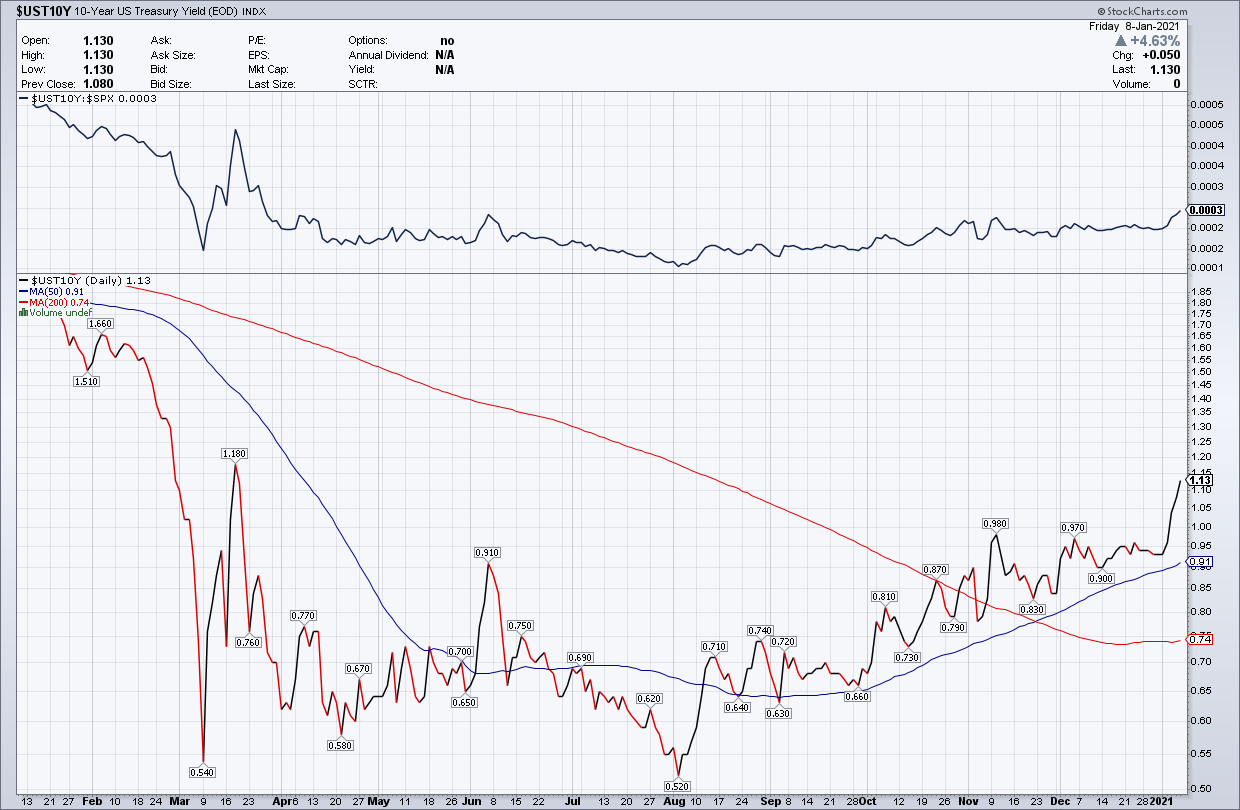

It’s been a bumpy (horrendous) start to the year, but the markets see sunny days ahead. In the same week that we experienced a real-life horror show, the 10-year not only broke over 1% for the first time since the beginning of COVID, but also ended the week with much higher yields!

My “America is Back” economic and housing market model needed the 10-year yield to get to 1% in 2020, and we got as high as 0.99% before the year ended. What happened with the 10-year yield last week was a material change in the market and one that I believe is an accurate indicator of better economic times ahead.

If we unpack the events of last week and look for correlating reaction of the markets, we can make the follow assumptions. Even though polls showed the Democrats had a chance to win both Senate seats in the Georgia runoff election, the bond market wasn’t convinced this could happen.

When the election results started to come in positive for Democrats, the bond market sold off and yields went higher, a very bullish response. Likewise the stock market ended the week at all-time highs.

The consensus assumption by the markets was that more fiscal disaster relief would be forthcoming to help the economy. However, now fiscal disaster relief will very likely be bigger than before.

Looking forward, if bond yields continue to go up then we can expect mortgage rates to increase. Bond yields have been going up since Aug. 2, however, mortgage rates have been falling. I wrote about this in my 2021 forecast article, as mortgage rates were never priced correctly in relationship with the 10-year yield in 2020.

In the previous economic cycle, when the 10-year yield got above 2.62%, we had higher mortgage rates and demand for housing got hit. In 2018, the new home sales market went into supply shock when mortgage rates got to 4.75 – 5%. There was less of an effect on the existing home sales market.

We are far from those mortgage rate levels today, but keep an eye on housing market metrics if the 10-year yield gets above 1.94%. I wrote about this in more detail here.

Achieving Touchless Mortgage Automation

Effective solutions must be purpose-built for mortgages, rather than adapted horizontal technology. In this webinar, experts at SoftWorks AI and Tavant discuss critical components of a mortgage automation solution and how to evaluate technologies that best fit your business’ needs.

Presented by: SoftWorks AI

My high-end target for the 10-year yield this year is 1.94%, which would translate to near 3.75% mortgage rates if rates are properly priced. Getting to 4% or higher mortgage rates would mean a break of my key 1.94% level, which would be extremely bullish for the U.S. economy.

Now that Democrats will have 50 votes plus the VP tiebreaker in the Senate, the fast-tracking of increased disaster relief is only one element of the story that could lead to higher yields. Add in the possibility that the vaccination rollout will accelerate and could be more efficient. With these improvements, yields should rise throughout the year. If we don’t see 10-year yields hit 1.33% in 2021, that would mean we didn’t spend enough money or that the vaccination story went very badly.

Having said that, as COVID-19 is still with us, mortgage rates should not go over 4%, which should still be bullish for the housing market. I expect mortgage rate highs to be in the range of 3.375%-3.625%, if we can get the 10-year yield between a range of 1.33% – 1.60%. These yield levels couldn’t have happened last year but for sure have a good shot in 2021.

Keep in mind, we still have a lot of headline risk that can send yields lower before we get to higher bond yields. We don’t know how well the vaccination roll-out will be, despite promises of improvements in efficiency. The political drama could get worse. Also, the stock market hasn’t had a 10% plus correction for a while. Once we get a correction in stocks, bond yields will fall.

In addition, the employment picture needs to improve a lot to get back to February 2020 jobs data. We have certain limits with our economy while COVID-19 is infecting and killing Americans daily. Until we are once again near full employment, the economy still has a lot of work to do.

The silver lining to the drama of last week is that we are about to get a bigger wave of fiscal disaster relief during a period when an effective vaccine is being rolled out. As Americans, we should cheering when we see the 10-year yield rising; our soothsayer is telling us we are winning the economic war against COVID-19 one basis point at a time.