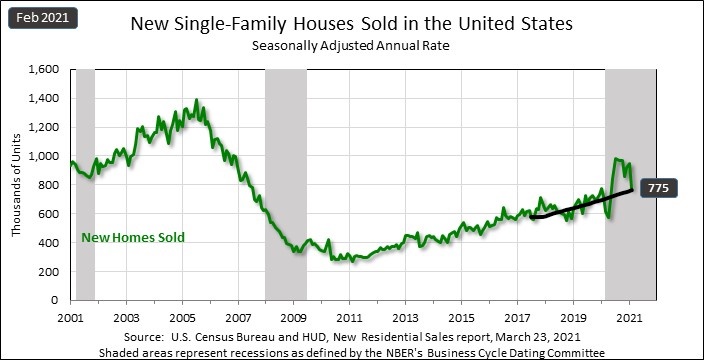

Today the Census Bureau reported that in February 2021, new single-family home sales were at a seasonally adjusted annual rate of 775,000.

This was a big miss from estimates. Although sales were up from 716,000 compared to sales in February 2020, they were 18.2% (±13.9%) below the revised sales in January 2021 of 948,000. The miss in sales immediately garnered comments about housing affordability.

New home sales are impacted more by increases in mortgage rates than an existing home. Mortgage rates, although still historically low, have risen recently. Higher mortgage rates at some point are going to quell any construction boom, despite what you may have heard from other analysts. But today’s new home sales number is largely due to sales just going back to trend after a parabolic rebound from the COVID shutdowns. Since the end of summer 2020 I have been warning that housing data would moderate and that is what we are seeing in the report today.

To illustrate, the chart below shows that new home sales had a parabolic spike in 2020 followed by the numbers going back to the trend. The data is still waffling – as it finds a stable sales range. This is a continuation of the story for the new home sales market in the previous cycle when we had slow and steady growth. Remember too that we can assume that the numbers in this new home sales report won’t stick. All significant deviations from the estimated sales, either positive or negative, revert to the trend. We are getting closer to a stable level to make a better diagnosis of each report. However, we aren’t there yet and I caution this about all economic data as well, not just housing.

New home sales are showing 8.2% year-over-year growth, which is impressive because we are comparing to strong sales in February of 2020. This is a similar story to what we are seeing in the existing home sales market. For the rest of 2021, the year-over-year data should be ignored because 2020 was such a crazy roller coaster ride. 2021 will show abnormal growth year over year due to the COVID-19 lows, followed by abnormal declines year over year due to the COVID rebound in sales in the second half of 2020.

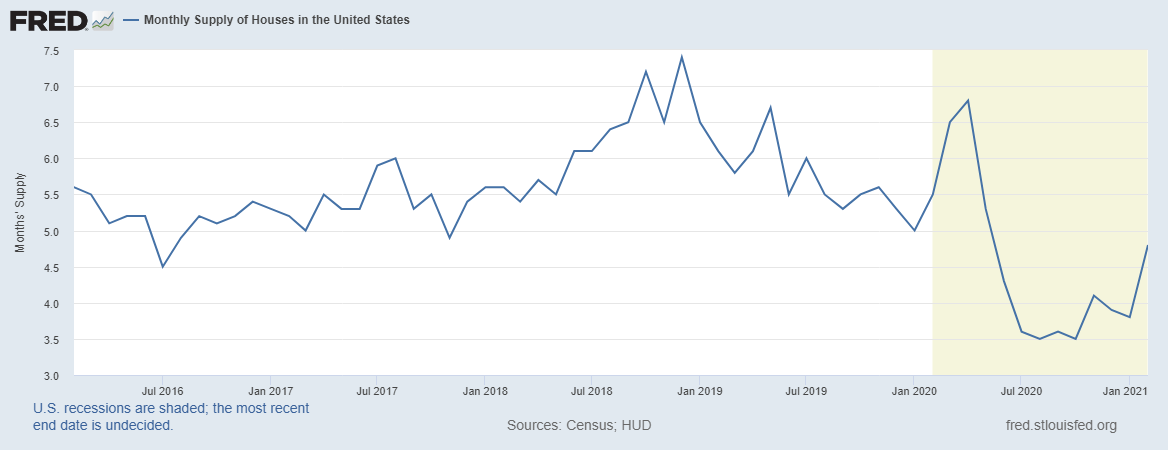

In my opinion, for 2021, the most important housing data trend to follow is the monthly supply for the new home sales market. When we are at 4.3 months and below, life is great for the builders. When supply is between 4.4 to 6.4 months it’s just meh for the builders. When supply is 6.5 months and over, builders will pull back from construction because demand no longer warrants more construction. We have seen this scenario play out twice recently when mortgage rates got to 4.75%-5% toward the end of 2018.

Last year, when COVID-19 paused everything in our economy, monthly supply went up and then quickly came back down. Inventory is rising again. Inventory in this report was at 4.8 months, whereas in the previous two months we were at 3.8 and 3.9 months. The three-month average is around 4.16 months, still low enough to be a “go-sign” for the builders. When the three-month average gets to 4.4 months and higher, then I would expect builders to become less enthusiastic about new construction. Pretty much for the previous expansion, monthly supply was always above 4.3 months and the last cycle had the weakest new home sales recovery ever recorded in history.

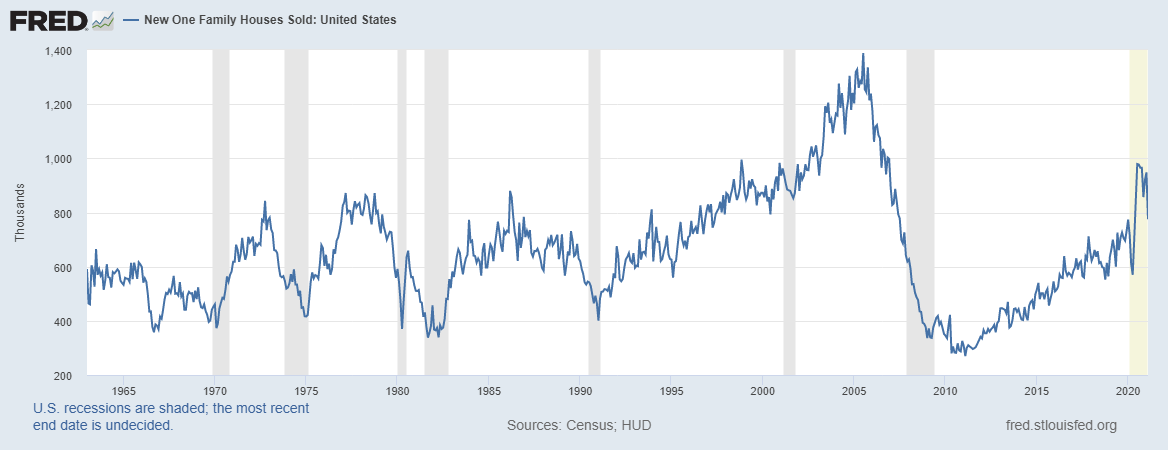

As you can see below, we were not overheating in new home sales before COVID-19 hit us. We did have an abnormal parabolic spike in new home sales last year that is still being worked out.

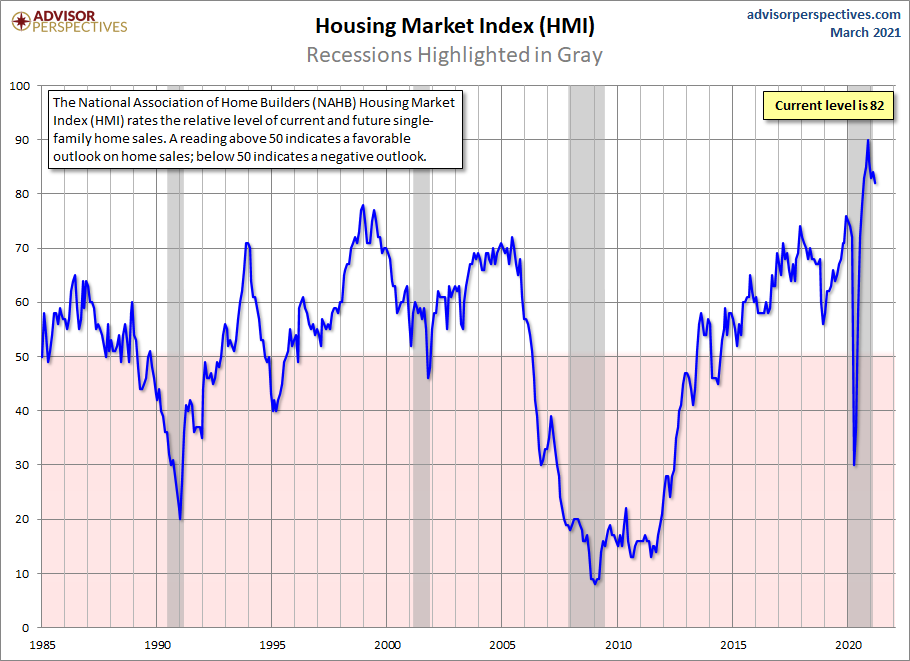

The builder’s confidence index is a good depiction of the builder’s outlook for future projects. As long as the monthly supply is trending below 4.3 months, builders will remain bullish. This data, like other housing data, is likely to continue to moderate. There is a 67% increase in year-over-year growth in new homes for sales for projects that haven’t started yet. It’s going to take a little more time to get some foundation of a normal trend. However, housing data can give you a heads up when things are actually getting weaker. Historically, year-over-year growth isn’t a good thesis for weakness.

The Census reported the median sales price of new houses sold in February 2021 was $349,400. The average sales price was $416,000.

Homebuilders have been offering smaller and smaller homes in their sales mix, which means the rate of growth of the median sales price has cooled since 2014. However, if it is true that Americans are wanting bigger homes, then this trend might have found a short-term bottom.

Right now the housing data is fluctuating, trying to find a stable trend in the sales. The parabolic spike in demand that occurred in the second half of 2020 was the most abnormal housing data line I will ever see in my life. It will take time to find a stable sales trend, so don’t read too much into the recent housing data. When mortgage rates rise high enough to impact demand, the hot price growth in the existing home sales market should cool.

However, it’s different for the new home sales market. This sector can’t really compete with the existing home sales market, so when rates rise it’s a real disadvantage. New home sales from 2018 showed us that mortgage rates of 4.75% to 5% create a supply shock and caused builders to back off construction. We are far away from those mortgage rate levels right now, but you have to know your limits with new home sales. This is why I use the term “replacement buyers.” If total housing sales (both new and existing combined) come in at 6.2 million and above in years 2020-2024, that should be considered a beat. This is something that couldn’t happen in the years 2008-2019, but now we have the demographics to back this up. We should finally have a year where housing starts will start a year at 1,500,000. We aren’t there yet, but we are getting there.