In 2021, a lingering symptom of the economic sickness we suffered in 2020 is forbearance. Not the forbearance plans themselves, which allowed mortgage holders to delay their payments for many months, but the fact that 2.72 million homes remain in forbearance and can therefore be considered at risk. Forbearance will have to end at some point, and when it does, couldn’t all these homes flood the housing market at once, driving prices down and scaring would-be homeowners away from purchasing?

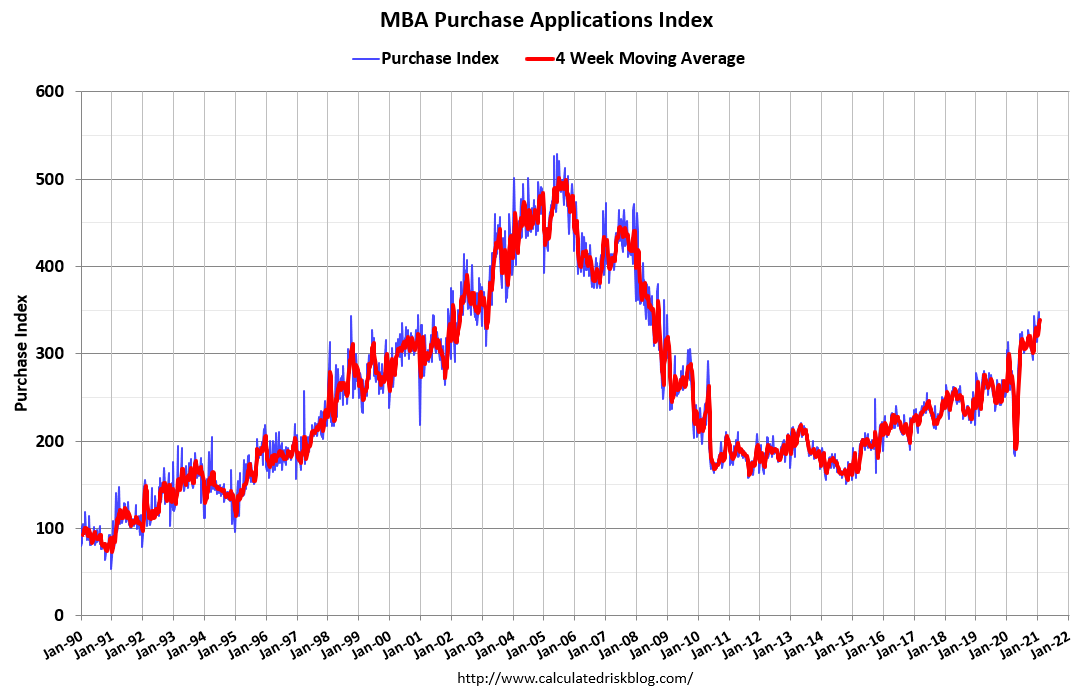

We know the current status of the housing market in America is vigorous, if not hot. The MBA purchase application data is growing at a trend of 12% year over year. This growth is 1% higher than the peak of what I forecasted for 2021, up until March 18.

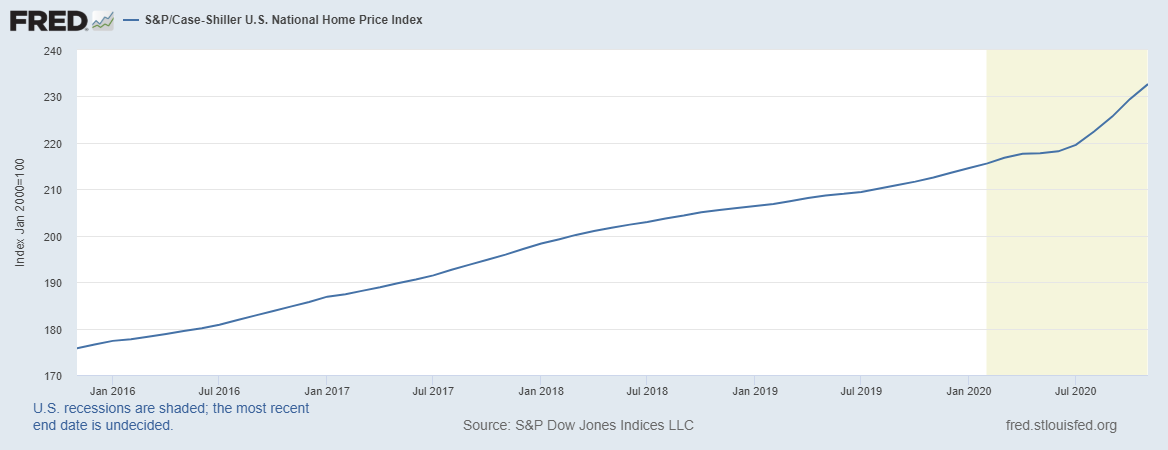

So while the housing market bubble bears predicted a crash due to the COVID crisis, the exact opposite is happening. Home price growth is accelerating above my comfort zone for nominal home price growth, which is 4.6% or lower. As I have written many times, the housing market’s current strength is not because of COVID-19, but despite it. Demographics plus low mortgage rates serve as the one-two punch that knocked out COVID-19.

In 2018/2019, when mortgage rates got to 5%, all it did was cool down price gains in the existing housing market. Real home prices went negative year over year, which I wrote back then was very healthy and what the housing market needed.

Here’s how to find property owners ready to sell

In today’s low-inventory environment, complicated by external factors such as forbearance and foreclosure moratoriums, it’s crucial for real estate agents and brokers to be proactive in order to grow their business.

Presented by: PropStream

Today, inventory levels are at all-time lows, and the purchase application data index is above 300. This means home price growth is getting too hot! Just look at the difference 2020 brought into the data lines.

The question remains: will all this strength in the housing market dampen or erase the risk of having all those homes in forbearance once forbearance ends? Here are three reasons you don’t have to worry.

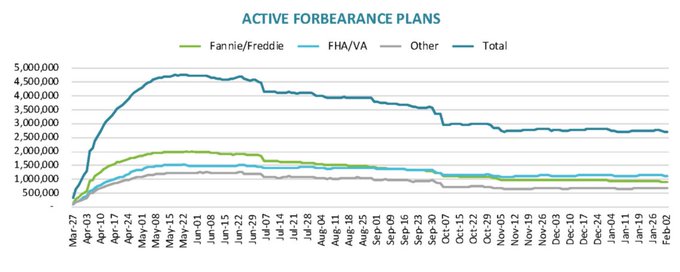

First, the latest chart from BlackKnight shows us that the number of homes in forbearance has been decreasing. We are well off the peak. I expect this number to decline as our employment picture improves; however, there will be a lag period for this data line to show more improvement.

Second, and this is critical to the story, homeowners’ credit profiles, when they originated their loans, were excellent. The previous expansion had the best loan profiles I have seen in my life. These buyers, especially those who purchased from 2010-2017, have fixed low debt costs due to low mortgage rates, with rising wages and nested equity. As home prices continue to grow beyond expectations, these homeowners have added another year of gains to their nested equity.

In this way, the current housing market backdrop is unlike the housing credit bubble years when loan profiles weren’t healthy, and we had a debt leverage speculative market. Last year, I wrote about the forbearance crash bros to outline their problems with their crash thesis. Here is a link to one of those articles.

And the third reason we don’t have to worry about a crash when forbearance ends is J.O.B.S.!

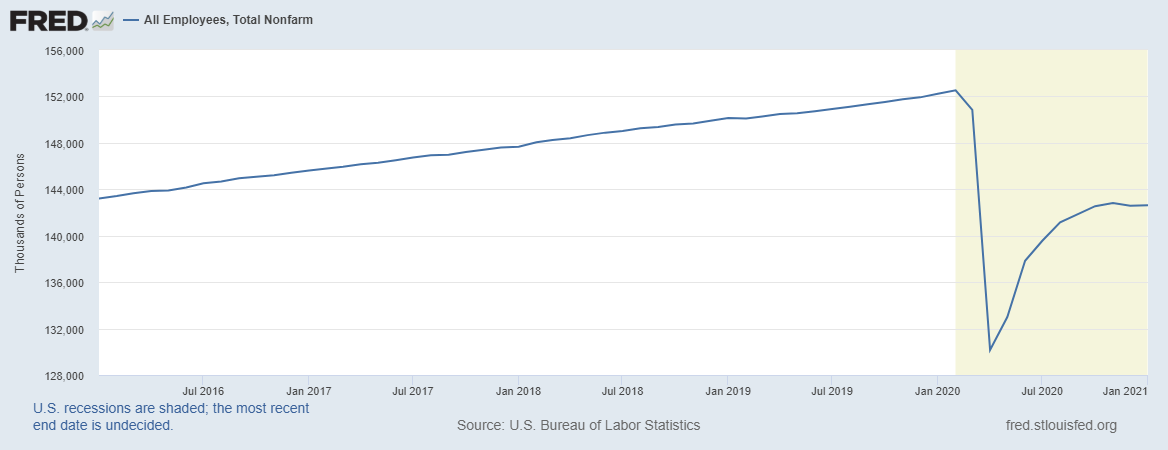

The primary reason I believe the crash thesis of the housing market bubble boys turned forbearance crash bros will fail is that jobs are coming back. The employment gains started last year and have continued. We have gained 12,470,000 jobs – and that was not in the forecast of the housing bubble boys.

The February 2020 nonfarm payroll data, which accounts for most workers, had roughly 152,523,000 employed workers. We got as low as 130,161,000 employed workers during the Covid crisis peak and are now back to 142,631,000. We are still short 9,892,000 jobs, which is more than the jobs lost during the great financial crisis.

Sadly, but to be expected, the last two jobs report combined were negative. We will not get back to the employment level we had in February 2020 while COVID-19 is with us, which prevents some sectors from operating at full capacity. So job growth remains limited until we get more Americans vaccinated.

Think of this period as the calm before the job storm.

And the job storm is coming. We are vaccinating people faster every week that goes by. We just need time, and then all the lost jobs will come back and then some. Even those 3.5 million permanent jobs lost will be replaced.

This isn’t 2008 all over again. That housing market recovery was slow, but today our demographics are better, and our household balance sheets are healthier. The fiscal and monetary assistance now is hugely improved from what we saw after 2008. We have everything we need to get America back to February 2020 jobs levels; we just need time.

I am convinced that the number of homes under forbearance will fall as more people gain employment. Expect the forbearance data to lag the jobs data, but they will eventually coincide.

Disaster relief is coming, and then when we can walk the earth freely, look for the government to do a stimulus package to push the economy along. By Aug. 31, 2021, we will have a much different conversation about the state of U.S. economics. Hopefully, by then, the 10-year yield will have hit 1.33% and higher. Wait for it!

If the jobs data continues to worsen and we decide it is too expensive to help our American citizens in this crisis, we will likely see an uptick in distress sales and forced selling, but we still would not see a bubble crash in the housing market. It may suppress home price growth, but that wouldn’t necessarily be a bad thing since my most significant concern in housing is that home prices are growing too fast. I recently talked about it on Bloomberg Financial.

If we are battling COVID-19 as war, would we leave any American behind? Imagine during wartime if we were told to build our tanks, rifles, and gear to fight the war without government assistance. The government can do certain things that the private sector can’t. Without COVID-19, we would still be enjoying the most prolonged economic and jobs expansion in history and have debates about what constitutes full employment. But it happened, and we have the power to leave no American behind once again.

Think about that next time you see someone hawking a housing market bubble crash thesis. All the jobs will come back in time, and we will all be walking in the sun again without a mask. Until then, we need to support government programs, like disaster relief and programs that help homeowners in forbearance get out of it, and help renters too. Let’s not leave any American behind in this war against COVID-19.

COVID-19 caused catastrophic unemployment that in turn triggered mortgage deferrals and forbearances.

How will this all work out when the Federal government removes foreclosure and eviction bans?

When it comes to home ownership, there is a HUGE difference in today’s scenario as compared to the Mortgage Meltdown of 2007+. The impact of the Mortgage Meltdown of 2007+ was a huge spike in foreclosures caused by homeowner NEGATIVE EQUITY….most homeowners fought the process and forced banks to foreclose. It took may years to purge the system of that mortgage delinquency. Massive volume of foreclosures hit the market de-stabilized housing prices.

TODAY, most homeowners have considerable POSITIVE EQUITY in their homes. The net result is, if they cannot afford to make their mortgage payments (i.e. still unemployed), that they simply will sell their home and pocket their positive equity.

OR- and this is key- banks (and holders of mortgages) will just MODIFY the delinquent homeowners- assuming they can now pay their mortgage (i.e. re-employed) and defer the delinquent balance to the back end of the loan. This provides the best economic result to Banks who have learned a hard lesson from the 2007+ mortgage meltdown- foreclosure is expensive and lengthy and would require a re-tooling of their work force.

There has been little new housing stock built in the last 14 years (from the beginning of the Mortgage Meltdown of 2007+), the net result being that housing is in very SHORT SUPPLY.

And- INTEREST RATES are extremely low (and look to stay that way for a considerable period) making homeownership economically advantageous.

PLUS- If Biden’s $15K first-time -homebuyer tax credit passes this will simply add fuel to the fire and push home prices higher. Remember Obama’s first time homebuyer credit of $8K in 2008? It resulted in a surge in demand and higher prices for entry level housing.

It’s a Straight Flush for housing.